Structured settlement documents and annuity contract next to a judge gavel on divorce papers representing settlement division during divorce

How Courts Divide Structured Settlement Payments in a Divorce

Content

When you're getting divorced and one of you has been receiving structured settlement payments, you're facing a puzzle most divorce attorneys only see a few times in their careers. Your monthly annuity checks can't be split down the middle like a 401(k). Banks won't just redirect half to your ex's account. The insurance company that sends your payments? They're bound by federal rules that make dividing these funds genuinely complicated—not just expensive-lawyer complicated, but legally-impossible-without-creative-workarounds complicated.

Here's what makes these cases so tricky: the very protections that keep creditors from seizing your settlement also prevent your spouse from claiming half. Courts can't override these restrictions by simply issuing an order. They need strategies that work within tight legal boundaries while still achieving a fair split of marital assets.

Are Structured Settlements Considered Marital Property?

The date you signed your settlement paperwork—not when you got injured or filed your lawsuit—typically determines whether courts treat your annuity as joint marital property or your separate asset. Got your settlement in 2021 but didn't marry until 2022? That's likely your separate property in most states. Finalized that same settlement in 2023 after marrying in 2022? Now you're probably looking at marital property subject to division.

Around thirty states carve out special treatment for personal injury settlements. These jurisdictions recognize something fundamental: money compensating you for a broken back, traumatic brain injury, or permanent disability represents something deeply personal. It's not like the vacation home you bought together or the stock portfolio you built during marriage. Courts in these states often classify such settlements as separate property belonging exclusively to the injured spouse.

But there's a catch—actually, several catches. Let's say you settled a workplace injury case for $500,000, structured to pay you $2,500 monthly for twenty years. The portion compensating you for medical bills and physical suffering? Separate property in many states. The portion replacing the wages you can't earn anymore? That's almost always considered marital property because those lost wages would have supported your household during the marriage.

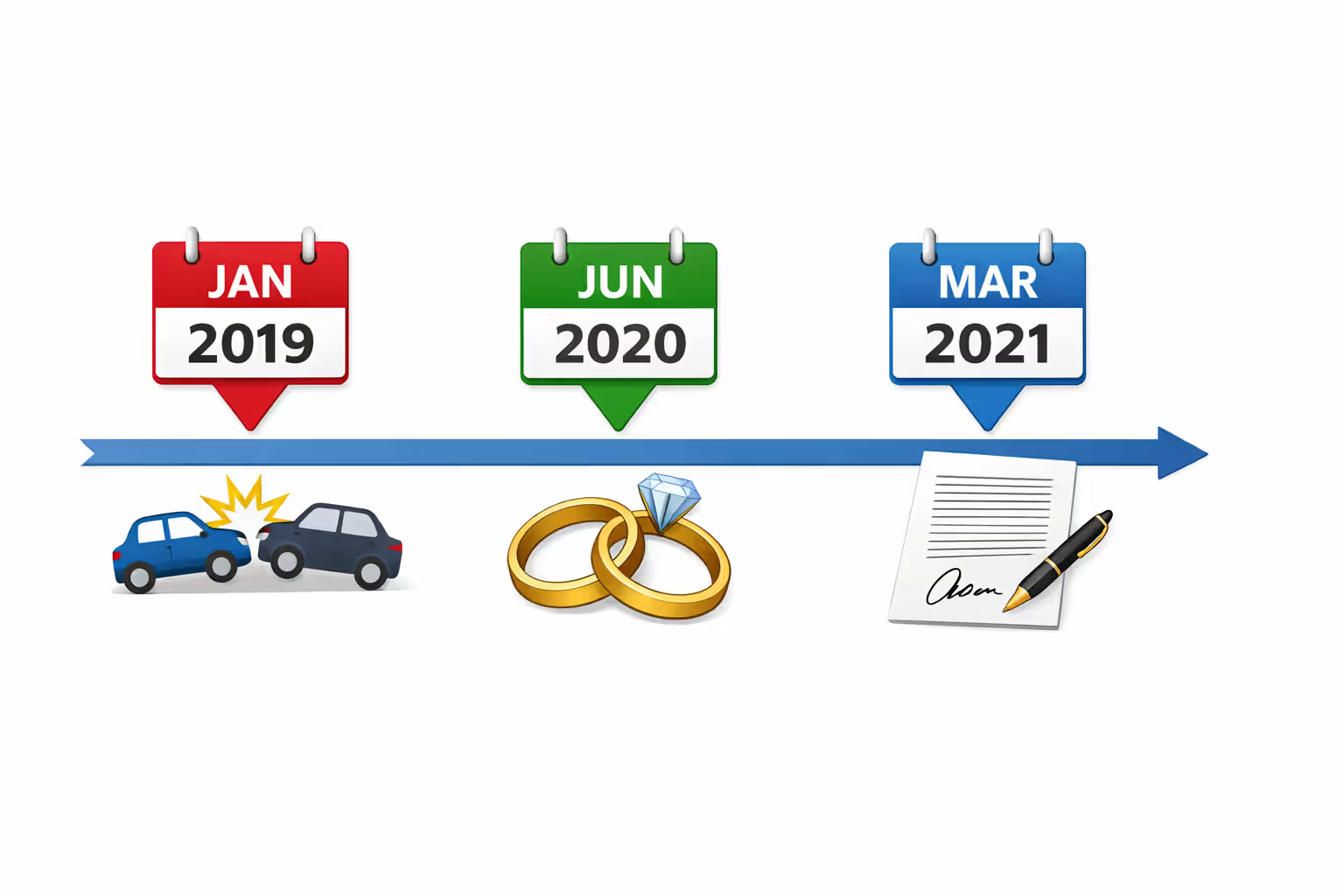

Take this real-world example: Maria was rear-ended by a commercial truck in January 2019. She married Robert in June 2020. Her structured settlement finalized in March 2021. Even though her injury happened while she was single, she received the settlement after marriage. Unless she lives in a state with broad personal injury exceptions, that settlement gets classified as marital property—meaning Robert has potential claims to its value in a divorce.

Author: Olivia Carmichael;

Source: avayabcm.com

Employment-related settlements get even messier. When you settle an age discrimination or wrongful termination case, courts view those payments as wage replacements. You sued because you lost your job and the income it provided. That income would've paid the mortgage, funded family vacations, filled the retirement accounts. Courts treat these settlements like pension benefits or deferred compensation packages—definitely marital property.

State lines matter enormously. Texas law treats virtually all personal injury settlements as separate property, period. Massachusetts judges take a more granular approach, examining whether specific damages compensate for losses during or after the marriage. California courts sometimes split a single settlement into marital and separate components based on when different types of harm occurred.

Your documentation practices can make or break your separate property claim. If you received a structured settlement three years before getting married, you absolutely need the original settlement agreement, the annuity contract showing the purchase date, and bank statements proving you kept those payments separate from joint marital accounts. Deposited your $3,000 monthly settlement checks into the joint checking account you shared with your spouse? You've just given their attorney ammunition to argue you treated it as marital property all along.

How Courts Divide Structured Settlements During Divorce

Federal law and the contracts governing your settlement contain what lawyers call "anti-assignment clauses"—legal language that essentially says "these payment rights cannot be transferred to anyone else, period." This isn't just a contractual preference. It's baked into the federal tax code and state consumer protection laws. When a judge realizes they can't simply order the insurance company to send half your monthly payment to your ex-spouse, they need to get creative.

Most commonly, courts use what's called an offset approach. They calculate what your entire structured settlement is worth today (we'll dig into that thorny calculation shortly), then assign that whole value to you. Your spouse gets other marital assets—the house, retirement accounts, investment portfolios—adding up to roughly the same amount. You received a settlement worth $350,000 in present value? Your spouse might walk away with the $150,000 in home equity, your $120,000 Fidelity rollover IRA, and the $80,000 in joint savings.

When couples don't have enough other assets to balance things out, judges sometimes order direct payment arrangements. You keep receiving your $2,800 monthly settlement check, but the divorce decree requires you to pay your ex-spouse $1,200 every month from those proceeds. Critically, this doesn't change your structured settlement contract—the insurance company still sends the full amount to you. The court has simply imposed a personal obligation on you to share what you receive. This works when payment amounts are sufficient and, frankly, when your ex believes you'll actually send those monthly checks instead of forcing them back to court for enforcement.

A small percentage of cases involve actually selling structured settlement rights under state transfer statutes. This requires jumping through serious legal hoops: court hearings, detailed financial disclosures, mandatory waiting periods, and judicial findings that the transfer serves your best interest. Even when approved, you'll typically receive only 50-70 cents per dollar of present value—a terrible deal financially, but sometimes necessary when no other assets exist to offset the settlement's value.

Community Property vs. Equitable Distribution States

Where you file for divorce matters as much as the settlement itself. Nine states—Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin—follow community property rules requiring roughly equal splits of marital assets. When your structured settlement counts as community property, your spouse walks in presumptively entitled to half its value.

The remaining forty-one states give judges much broader discretion. Courts in these "equitable distribution" jurisdictions consider how long you've been married, each person's income and earning potential, who contributed what to acquiring marital property, and each spouse's financial needs going forward. A judge might award you seventy or eighty percent of the settlement's value if you're the injured party with permanent disabilities and limited work capacity, while your spouse has a six-figure income and full health.

| Community Property Approach | Equitable Distribution Approach |

| Starts with assumption each spouse gets 50% of marital asset values | Judge weighs multiple factors to determine what division seems "fair" |

| Limited wiggle room for judges to deviate from equal splits | Courts can award 60/40, 70/30, or other unequal divisions |

| When you got the settlement determines everything—marital or separate | Circumstances surrounding your injury may influence the final division |

| Separate property stays 100% with whoever owned it originally | Courts might consider separate property when determining overall fairness |

| Fights typically center on getting the present value calculation right | Battles involve both valuation disputes and fairness arguments |

| Offset arrangements dominate because equal division is expected | More flexible approaches including graduated payment schedules |

| Personal injury rules vary significantly despite community property framework | Broader ability to account for injury's impact on family finances |

Calculating Present Value for Settlement Division

Your structured settlement might pay out $750,000 over twenty-five years, but that doesn't mean it's worth $750,000 today. Courts hire financial experts—forensic accountants or structured settlement consultants—to calculate what's called "present value." This represents the lump sum you'd need to invest today, at current market rates, to replicate your future payment stream.

Here's why this matters: $3,000 received buys more than $3,000 you'll receive in 2044. Inflation erodes purchasing power. Money you have now can be invested to generate returns. There's also the risk (however small) that the insurance company could fail before making all payments. Financial experts account for all these factors using "discount rates"—typically ranging from three to seven percent.

Let's work through a real example. You receive $2,500 monthly for fifteen years—$450,000 total. Using a 5% discount rate and standard present value formulas, that payment stream is worth approximately $315,000 today. Use a 4% discount rate instead? The present value jumps to around $335,000. That's a $20,000 difference based solely on the discount rate assumption—which explains why valuation battles get heated during divorce negotiations.

Author: Olivia Carmichael;

Source: avayabcm.com

Life-contingent payments add another layer of complexity. Many structured settlements pay "for life" or "for life with ten years guaranteed." If your payments stop when you die, actuaries must estimate how long you'll likely live based on your current age, gender, health status, and lifestyle factors. A healthy 40-year-old woman receiving lifetime payments has substantially higher present value than a 68-year-old man with heart disease receiving identical monthly amounts—the woman will likely collect payments for decades longer.

Your spouse's attorney will push for the lowest discount rate possible because that maximizes present value and increases what you must offset with other marital assets. Your attorney will argue for higher discount rates to reduce the present value calculation. A two-percentage-point difference in a $500,000 settlement can shift valuations by $50,000 or more. That's why hiring your own financial expert rather than relying on your spouse's numbers is worth every penny.

Common Legal Issues When Dividing Settlement Annuities

Those anti-assignment clauses we mentioned earlier create the biggest headaches in these cases. Federal structured settlement legislation and the Internal Revenue Code both rely on these provisions to provide tax benefits and creditor protections. Courts cannot simply wave a magic wand and override federal law because you're getting divorced. Even a judge's explicit order transferring payment rights to your spouse won't force the insurance company to comply—they're contractually prohibited from making payments to anyone except the named annuitant.

These anti-assignment rules aren't merely contract terms you might negotiate around or legal technicalities a good lawyer can sidestep. They form the foundation of the entire structured settlement framework. Try to violate them, and you risk triggering payment terminations, tax penalties, or both. I've seen divorcing couples lose everything trying to force square pegs into round holes

— Family law attorney

Attempting unauthorized transfers can blow up in your face spectacularly. Some annuity contracts contain forfeiture provisions automatically terminating all future payments if you try transferring rights to anyone else. Imagine explaining to a judge that your settlement—worth perhaps hundreds of thousands in present value—vanished entirely because you violated anti-assignment terms. The IRS might also reassess your tax situation, determining that improper assignment destroyed your settlement's tax-exempt status and demanding back taxes plus penalties on payments you've already received.

Tax complications extend beyond assignment problems. While your structured settlement payments for physical injuries typically arrive tax-free under Section 104 of the Internal Revenue Code, the monthly checks you send your ex-spouse might be taxable income to them. Current federal tax law (post-2018 Tax Cuts and Jobs Act) eliminates alimony deductions, meaning you cannot deduct these payments on your tax return even if they're characterized as spousal support. You're paying taxes on money you're required to give away without getting any deduction—a harsh result.

Payee designation becomes an enforcement nightmare when courts order you to pay your spouse directly from settlement proceeds. Your ex-spouse cannot garnish payments from the insurance company because the anti-assignment clause prevents third-party payment rights. If you stop sending those monthly checks, your ex must take you back to court for contempt, obtain a judgment, then attempt to collect from other income or assets you might have. They're essentially an unsecured creditor hoping you'll voluntarily comply rather than force expensive enforcement litigation.

Creditor protection issues cut both ways. Structured settlements enjoy robust protection from creditors under both federal and state laws—creditors generally cannot seize your annuity to satisfy judgments against you. Once you've offset your settlement against other marital assets, though, those protections don't transfer. Your ex-spouse receives the marital home, retirement accounts, and investment portfolio in exchange for your settlement? All those assets they received remain vulnerable to their creditors in ways your original structured settlement never was.

Protecting Your Structured Settlement Rights Before and During Divorce

Start building your paper trail long before you ever consider divorce. Keep the original settlement agreement showing exactly when you received the settlement and what it compensates. Maintain the annuity contract establishing payment terms. Save every payment statement or direct deposit confirmation. If you're claiming any portion as separate property—injury before marriage, inheritance that funded the settlement, or pre-marital acquisition—assemble medical records, legal complaint filings from the underlying lawsuit, and any other documents establishing the timeline.

Strategic timing can significantly affect property classification, though courts scrutinize suspiciously-timed settlements carefully. Imagine you've been negotiating a major personal injury settlement while your marriage deteriorates. You could potentially delay finalizing until after filing for divorce, which might preserve separate property status in some jurisdictions. However, judges see through transparent attempts to manipulate property characterization—especially when settlement delays coincide precisely with marital breakdown. Courts can "relate back" the settlement's classification to when negotiations substantially concluded.

Author: Olivia Carmichael;

Source: avayabcm.com

Negotiation leverage often comes from educating the other side about structured settlement limitations. Many divorce attorneys have never handled these cases. Your spouse may not understand that attempting to force a transfer is legally impossible or that selling settlement rights means accepting massive discounts. Propose win-win solutions: you keep the structured settlement with its restrictions and ongoing tax benefits, while your spouse takes more liquid assets—cash, real estate, retirement accounts—that are easier to access and manage. In many divorces, spouses prefer receiving the house over fighting about complex annuity valuations.

Creative compensation methods can bypass anti-assignment problems entirely. Rather than calculating a controversial present value figure, agree that you'll pay your spouse twenty-five percent of each payment as you actually receive it. This shares the settlement's benefit without violating anti-assignment rules or requiring present value fights. You might agree to maintain life insurance naming your ex as beneficiary—if you die before the settlement pays out, life insurance proceeds compensate them for lost settlement value they would've received through other means.

Prenuptial agreements or postnuptial agreements provide the strongest protection available, though you need one drafted before marital trouble starts. These agreements can explicitly classify any structured settlement as separate property, establish specific valuation methodologies if divorce occurs, or have your future spouse waive all claims to settlement proceeds. Courts generally enforce properly-drafted marital agreements unless they're unconscionably unfair or were signed under duress. Getting your fiancé to sign away rights to a structured settlement worth hundreds of thousands might require offsetting concessions—perhaps waiving claims to their business or inheritance—but it's doable with skilled attorneys on both sides.

Don't wait until divorce papers are filed to consult structured settlement specialists. These experts understand technical restrictions your general practice divorce attorney may not grasp. They can provide accurate valuations that won't be demolished by opposing experts at trial. Some settlement recipients work with consultants during initial settlement negotiations to structure payment terms anticipating potential future divorce—perhaps requesting guaranteed payment periods rather than life-contingent terms, or structuring multiple smaller annuities that might be easier to divide than one large contract.

Tax Implications of Structured Settlement Division in Divorce

Section 104(a)(2) of the Internal Revenue Code excludes damages for physical injuries or sickness from taxable income. When you receive $3,000 monthly from a structured settlement compensating you for injuries sustained in a car accident, you don't report that as income or pay taxes on it. This valuable tax treatment continues throughout the payment period—but divorce can create unexpected tax complications that erode this benefit.

The IRS views your structured settlement as property rather than an income stream when dividing assets during divorce. Offsetting your settlement against your spouse's share of other marital assets doesn't trigger immediate taxation—you're just dividing existing property between divorcing spouses. Section 1041 generally allows spouses to transfer property between themselves without tax consequences during divorce. However, you remain the taxpayer for all future payments under your settlement. Your ex-spouse cannot claim tax-free treatment for money you pay them from settlement proceeds, even though your original payments arrive tax-free.

Let's examine how this plays out practically. Your monthly $4,000 structured settlement payment arrives tax-free under Section 104. The divorce decree orders you to pay $1,800 monthly to your ex-spouse from these proceeds. You're not paying taxes on the $4,000—that remains excluded from income. But your ex-spouse might owe taxes on the $1,800 they receive, depending on how the divorce decree characterizes these payments. If structured as property division, they arguably shouldn't be taxable. If characterized as support, they're likely taxable income to your ex.

Here's where the 2017 Tax Cuts and Jobs Act makes everything worse: alimony and spousal support payments are no longer tax-deductible for the paying spouse in divorces finalized after December 31, 2018. Previously, you could deduct alimony payments on your tax return while your ex reported them as income. Now? You get no deduction even if payments are taxable to your ex. This creates potential double taxation—you're paying taxes (or losing tax-free benefits) on money you're giving to your ex, who might also owe taxes on receiving it, with nobody getting a deduction.

Income attribution disputes arise because the IRS may not care what your divorce decree says. You remain the named annuitant on the structured settlement. Payments flow to you. From the IRS perspective, you're receiving the income—and if it's taxable, you owe the taxes. When you turn around and pay your ex from these proceeds, the IRS might view that as a gift, property transfer, or support payment rather than your ex receiving settlement income directly. Without careful tax planning and proper divorce decree language, you could face IRS challenges during audits.

Documentation becomes absolutely critical. Continue reporting your structured settlement payments exactly as you did before divorce—excluded from income if they qualify under Section 104, reported as ordinary income if they don't. Payments you make to your ex should be carefully documented as property division rather than support, using specific language in your divorce decree that preserves intended tax treatment. Your ex-spouse should not report these amounts as income when they're properly structured as tax-free property transfers.

Selling structured settlement rights to fund property division creates definite tax consequences you'll want to avoid if possible. The IRS has ruled that while sale proceeds from a Section 104 settlement aren't taxable income, you're still receiving perhaps 50-60% of your settlement's actual present value. That 40-50% haircut represents a massive economic loss—one that's essentially permanent and irreversible. Add state transfer approval costs, attorney fees for the sale hearing, and potential state premium taxes, and selling becomes the most expensive way to handle settlement division.

Mistakes to Avoid When Your Structured Settlement Is Part of Divorce Proceedings

Panic-selling your structured settlement to raise quick cash for the divorce ranks as the single most costly error. You're stressed about legal bills piling up, maybe needing money for a new apartment and furniture. Settlement purchasing companies make selling sound easy—quick approval, money within weeks. What they don't emphasize: you'll receive somewhere between 50 and 65 cents per dollar of present value. That settlement worth $400,000? You might net only $220,000 after the sale. State transfer laws require courts to approve sales and mandate disclosure of effective discount rates, but even approved sales represent financial disasters compared to working out offset arrangements.

Agreeing to undervalued offsets happens when neither spouse brings in proper financial experts. Your divorce attorney, however skilled at custody negotiations and property division generally, might lack specific structured settlement valuation expertise. They agree to offset your settlement—which careful analysis shows is worth $380,000—against only $260,000 in other marital assets. You've just given away $120,000 in value because neither side ran the numbers correctly. Always hire qualified forensic accountants or structured settlement consultants to perform present value calculations using appropriate discount rates, mortality tables, and payment analysis.

Author: Olivia Carmichael;

Source: avayabcm.com

Short-term thinking leads people to fight for immediate assets while surrendering long-term financial security. You might battle to keep the house, agreeing to let your spouse have greater claims against your structured settlement because you're emotionally attached to staying in the family home. Run the numbers twenty years out—will the house still be worth the massive settlement value you surrendered? Or conversely, you might fight to keep every penny of settlement value without recognizing that accepting the house, retirement accounts, and investment portfolio gives you better liquidity and financial flexibility.

Failing to gather separate property documentation before your spouse files for divorce leaves you scrambling to prove what should be straightforward. Once divorce litigation begins, you're suddenly trying to track down settlement paperwork from eight years ago, medical records from before the marriage, and bank statements showing you kept settlement payments in separate accounts. You bear the burden of proving separate property status—courts presume property acquired during marriage is marital property unless you demonstrate otherwise. Without documentation, you're sunk.

Sloppy valuation shortcuts produce wildly inaccurate numbers that lead to unfair divisions. Some divorcing couples simply add up all future payments ($2,000/month × 300 months = $600,000) and divide by two, agreeing to offset $300,000. This completely ignores present value principles—that $600,000 in future payments is worth perhaps $375,000 today. You've just agreed to an offset that overvalues your settlement by $225,000, meaning you receive far less than fair value in other marital assets. Similarly, ignoring life-contingent payment terms or guaranteed payment periods can skew valuations by tens of thousands of dollars.

Setting up direct payment arrangements without security mechanisms creates enforcement headaches. The divorce decree orders you to pay your ex-spouse $1,500 monthly from your $3,500 settlement checks. Sounds simple. But what happens if you lose your job and can't afford to pay? What if you move across the country and stop sending checks? Your ex cannot garnish payments directly from the insurance company—anti-assignment clauses prevent that. They're stuck pursuing contempt motions, getting judgments against you personally, then attempting collection through wage garnishment or bank account levies. They might eventually collect, but only after months or years of expensive litigation. Build security into these arrangements: life insurance, wage assignment from your other employment, or restrictions on your ability to relocate without notice.

Working With Specialists: Who You Need on Your Divorce Team

Structured settlement consultants bring technical knowledge that general practice divorce attorneys simply don't have unless they've handled dozens of these cases. These specialists live and breathe annuity contracts, anti-assignment provisions, state transfer statutes, and settlement valuation methodologies. They review your specific annuity contract, identify restrictions your divorce attorney needs to understand, and suggest division strategies that work within legal constraints rather than wishing those constraints didn't exist. A consultant who charges $2,500 for case analysis can easily save you $50,000 in improved settlement terms.

Forensic accountants perform the detailed present value calculations judges rely on when dividing structured settlements. These aren't back-of-the-envelope estimates—they're sophisticated financial models incorporating discount rates based on current treasury yields and corporate bond rates, mortality calculations using actuarial tables from the Social Security Administration or insurance industry, and complex formulas accounting for payment timing, guaranteed periods, and life contingencies. Their expert reports, presented in sworn affidavits or trial testimony, often resolve valuation disputes because both sides recognize the analysis is mathematically sound and defensible.

Family law attorneys with actual structured settlement experience understand nuances that attorneys handling their first settlement case will miss. Not every divorce lawyer has dealt with these situations—they're relatively uncommon compared to typical property and custody disputes. When interviewing potential attorneys, ask directly: "How many divorce cases involving structured settlements have you handled?" Press for specifics: "What strategies did you use for division? Can you explain anti-assignment provisions and how they affected the outcome?" An attorney who's navigated these waters before knows which expert witnesses to hire, how to draft proposed orders that comply with technical restrictions, and which arguments resonate with judges in your jurisdiction.

Tax advisors—certified public accountants or tax attorneys focusing on divorce taxation—help structure division arrangements that minimize tax hits to both spouses. Someone fluent in Section 104 exclusions, Section 1041 divorce transfers, and current alimony taxation rules (or lack thereof) can draft divorce decree language that preserves intended tax treatment. They ensure you're not inadvertently destroying tax-exempt status, advise on reporting requirements post-divorce, and model tax consequences of different division scenarios. That $300/hour tax attorney could save you $15,000 annually in unnecessary taxes—every year for the rest of the settlement payment period.

Certified Divorce Financial Analysts (CDFAs) specialize in the financial rather than legal aspects of divorce. These professionals hold specific credentials in divorce financial planning, understanding how property division plays out over decades. They build financial models showing long-term impacts: "If you keep the structured settlement, here's your projected income and net worth at age 65. If you take the house and retirement accounts instead, here's how those assets grow over time." This forward-looking analysis helps you make smart decisions rather than emotional ones.

Be cautious with settlement purchasing company representatives who offer to "help" with your divorce. These companies profit by buying your payment rights at significant discounts, then collecting the full payment amounts over time. Their quotes might be competitive within the settlement purchasing industry—but even the "best" offers represent terrible deals compared to keeping your settlement and working out offset arrangements. They're not advisors working in your interest; they're buyers negotiating to pay you as little as possible. If you're seriously considering selling, consult independent advisors first who aren't making money from the transaction.

Build your team early—ideally before filing divorce papers, or immediately after being served. Once you've signed a settlement agreement with unfavorable terms, unwinding those mistakes becomes extremely difficult or impossible. Colorado's rule against modifying property division after 48 hours means you're likely stuck with whatever you agreed to, even if you later discover it was dramatically unfair. The cost of assembling this expert team—perhaps $10,000 to $25,000 total—pales compared to potential losses from mishandling settlement division worth hundreds of thousands of dollars.

Frequently Asked Questions

Dividing structured settlements during divorce requires navigating restrictions most divorce attorneys encounter rarely, if ever. The anti-assignment clauses protecting your settlement from creditors and preserving tax benefits simultaneously prevent straightforward division between divorcing spouses. Courts cannot override federal law or contractual provisions simply because you're ending your marriage—they must work within tight constraints while still achieving reasonably fair outcomes.

Success in these cases depends heavily on preparation, expertise, and realistic expectations. Document everything about your settlement's origin, timing, and separate versus marital property status. Bring in specialists who actually understand structured settlement valuation, tax implications, and division strategies that comply with technical restrictions. Work with divorce attorneys who've handled these cases before, not lawyers learning on your dime.

Whether you ultimately retain your structured settlement through offset arrangements, agree to share payments with your ex-spouse from proceeds as received, or pursue some other creative solution, informed decisions beat rushed agreements every time. The difference between understanding your options and signing whatever agreement your spouse's attorney proposes could mean $100,000 or more in present value—money that determines your financial security for decades to come.