Injured worker reviewing workers compensation structured settlement documents at a desk with legal papers and calculator

Workers Compensation Structured Settlement Guide

Content

Settling a workers compensation claim marks the end of one journey and the beginning of another. The check you receive—or the payment stream you agree to—must cover medical bills, replace lost wages, and sustain you through recovery or permanent disability. Yet many injured workers sign settlement agreements without fully understanding the difference between a lump sum and a structured payment plan, or how that choice will affect their finances for years to come.

A workers compensation structured settlement replaces a single large payment with a series of smaller, predictable disbursements over time. Insurance carriers often prefer this approach because it reduces their immediate cash outlay and limits exposure to claims that payments were mismanaged. For claimants, the appeal lies in guaranteed income, tax advantages, and protection from the temptation to spend a windfall too quickly. But structured settlements also lock you into a rigid payment schedule that can be expensive or impossible to change if your circumstances shift.

Understanding how these arrangements work, what state laws require, and which mistakes drain value from your settlement gives you leverage during negotiations and helps you avoid regret after signing.

What Makes a Workers Comp Settlement "Structured" vs. Lump Sum

When you settle a workers compensation claim, you typically choose between two payment models: a one-time lump sum or a structured settlement that pays out over months, years, or even your lifetime. The lump sum is straightforward—you receive the entire agreed amount at once, minus attorney fees and any liens. A structured settlement, by contrast, converts part or all of your award into an annuity that delivers periodic payments according to a fixed schedule.

Defining the Annuity Payment Model

A structured settlement annuity is a financial product issued by a life insurance company. Your workers comp insurer purchases the annuity on your behalf, funding it with a single premium equal to the present value of your future payments. Once the annuity is in place, the life insurer assumes responsibility for making payments to you on the agreed schedule—monthly, quarterly, annually, or in customized intervals that match your needs.

Because the annuity is irrevocable, you cannot accelerate payments, pause them, or withdraw the principal. The insurance company calculates the premium using actuarial tables that factor in your age, life expectancy, and prevailing interest rates. If rates are low when you settle, the carrier must invest more upfront to generate the same stream of future payments, which can reduce the total benefit you receive compared to a lump sum.

Author: Christopher Vaughn;

Source: avayabcm.com

When State Laws Require or Restrict Structured Payments

Most states allow injured workers to choose between lump sum and structured settlements, but a handful impose restrictions when awards exceed certain thresholds. California, for example, requires court approval for any settlement involving a self-represented claimant or a minor, and judges often mandate structured payments if they believe a lump sum poses a risk of dissipation. New York law requires structured settlements for certain permanent partial disability awards unless the worker can demonstrate financial hardship.

In states with "commutation" bans, workers compensation pensions for permanent total disability must be paid periodically and cannot be converted to a lump sum without a showing of extraordinary circumstances. Florida and Pennsylvania both restrict commutation, though the rules differ in detail. These laws exist to prevent injured workers from accepting discounted lump sums and then exhausting the funds before their medical needs end.

Even in states that permit full lump-sum settlements, insurers may insist on structuring large awards to manage their own cash flow and reduce the risk of future litigation over mismanagement. A workers comp structured settlement planning guide provided by your attorney should explain your state's rules and the leverage you have during negotiations.

How Structured Settlement Payments Are Calculated and Distributed

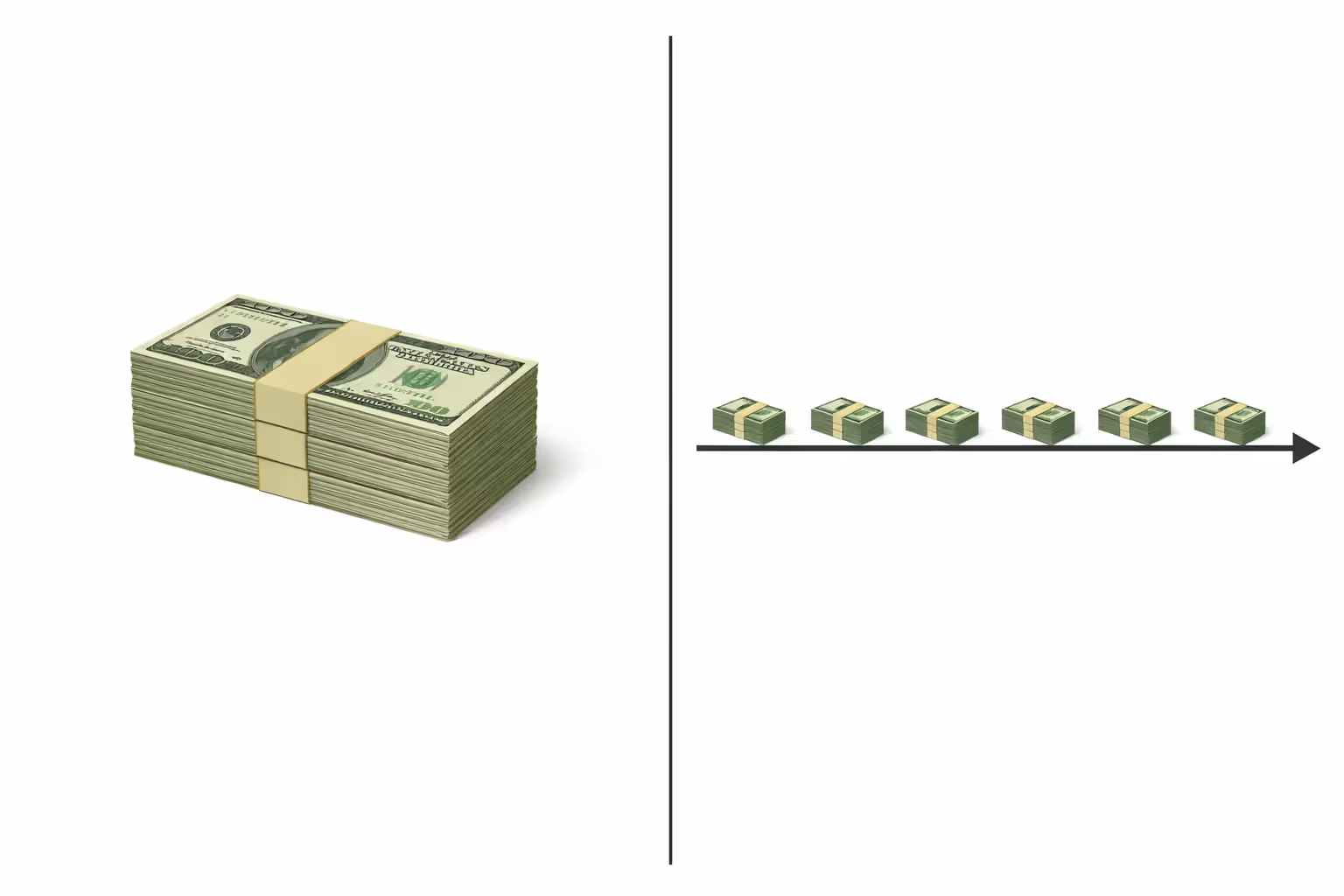

The dollar amount you see in your settlement agreement is not the same as the premium the insurer pays to the annuity company. That premium is the present value—the lump sum needed today to generate your future payments, assuming a certain rate of return. If your settlement calls for $2,000 per month for twenty years, the annuity premium might be $350,000, depending on interest rates and your age. The difference between the total payments you will receive ($480,000 in this example) and the premium reflects the time value of money and the insurer's investment earnings.

Factors That Determine Your Payment Schedule

Your payment schedule should align with your actual expenses. If you have ongoing medical costs, a monthly payment may cover prescriptions, therapy, and out-of-pocket copays. If your biggest concern is property tax or annual insurance premiums, a single annual payment could be more efficient. Many workers comp settlement annuity guide documents recommend front-loading payments in the first few years after settlement to cover immediate rehabilitation costs, then tapering to a lower monthly amount once you reach maximum medical improvement.

Cost-of-living adjustments (COLAs) are another critical variable. A fixed $1,500 monthly payment may feel adequate today, but inflation will erode its purchasing power over two decades. Some annuities offer annual increases tied to the Consumer Price Index, though adding a COLA reduces the initial payment amount because the insurer must reserve more capital to fund future increases.

Role of Life Insurance Companies and Annuity Providers

Once your settlement is approved, the workers comp carrier selects a life insurance company with a strong credit rating to issue the annuity. You typically have limited say in which carrier is chosen, though your attorney can object if the proposed insurer has a history of financial instability. The annuity is owned by you, and payments are guaranteed by the issuing company's reserves and, in many states, by state guaranty associations up to statutory limits (often $250,000 in present value).

If the life insurer becomes insolvent, state guaranty associations step in to continue payments, but coverage caps mean that very large structured settlements carry some risk. Diversifying a large award across multiple annuities from different carriers can mitigate this exposure.

| Payment Frequency | Pros | Cons | Best For |

| Monthly | Steady cash flow; easier budgeting; matches recurring bills | Higher administrative overhead; small payment amounts may feel insufficient | Claimants with ongoing medical expenses, rent, or living costs |

| Quarterly | Larger individual payments; fewer transactions to track | Less frequent income can strain budgets between payments | Workers with seasonal expenses or moderate savings discipline |

| Annual | Simplifies tax reporting; maximizes compound growth between payments | Long gaps require strong cash reserves; risk of overspending lump receipt | Claimants with other income sources or low monthly expenses |

State-by-State Rules Governing Workers Comp Settlement Structures

Workers compensation is a state-regulated system, and settlement rules vary widely. Some jurisdictions impose strict oversight to protect injured workers from predatory settlement practices, while others grant broad discretion to the parties. A workers comp structured settlement rules guide tailored to your state is essential before signing any agreement.

States That Mandate Structured Settlements for Large Awards

California requires judicial approval for any compromise-and-release settlement, and judges routinely order structured payments when the claimant is unrepresented, has a history of financial instability, or is receiving public benefits. The Workers' Compensation Appeals Board will reject settlements that appear to leave the worker without adequate future income.

New York mandates structured settlements for permanent partial disability awards classified as "schedule loss of use" above certain thresholds, unless the claimant demonstrates an immediate financial need that justifies a lump sum. The state's goal is to prevent workers from spending down awards and then seeking public assistance.

Florida prohibits commutation of permanent total disability benefits except in cases of extreme hardship, such as terminal illness or imminent foreclosure. Even then, the worker must petition the court and accept a discounted present value.

Approval Requirements and Court Oversight

In most states, structured settlements require approval by a workers compensation judge or administrative law judge. The hearing examines whether the proposed payment schedule is reasonable given your age, medical prognosis, and financial obligations. Judges pay particular attention to Medicare set-asides—funds earmarked to cover future medical costs related to your injury—and will reject settlements that fail to protect Medicare's interests.

If you are represented by an attorney, the approval process is usually straightforward, provided the settlement falls within the range of reasonable outcomes for your injury. Self-represented claimants face more scrutiny, and judges may appoint a guardian ad litem or require financial counseling before approving a structured settlement.

| State | Minimum Threshold for Mandatory Structuring | Court Approval Required? | COLA Standard? |

| California | No fixed threshold; judge discretion | Yes, for all C&R settlements | Not required, but common |

| Texas | No mandate; parties negotiate freely | Only if dispute exists | Rarely included |

| Florida | Permanent total disability awards | Yes, for commutation petitions | Not standard |

| New York | Schedule loss above $50,000 (varies by injury) | Yes, for structured PPD | Negotiable |

| Pennsylvania | No mandate; commutation restricted | Yes, for commutation only | Not standard |

| Illinois | No mandate | Yes, for all settlements | Rarely included |

| Ohio | No mandate; structured options available | Yes, for settlements over $25,000 | Not required |

| North Carolina | No mandate | Yes, for all settlements | Negotiable |

| Georgia | No mandate | Yes, for settlements over $50,000 | Rarely included |

| Michigan | No mandate | Yes, for redemption settlements | Not standard |

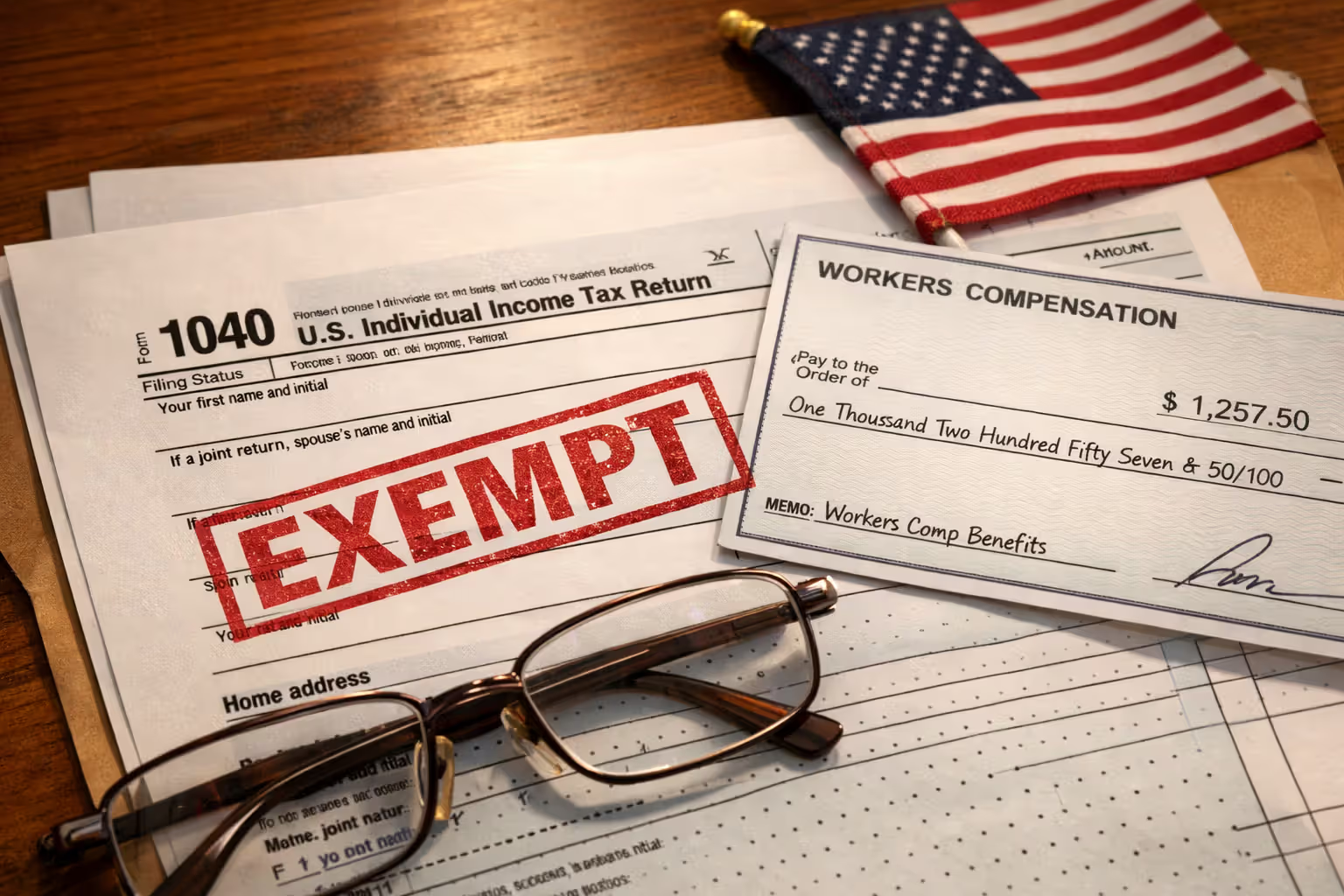

Tax Treatment and Long-Term Financial Implications

One of the most compelling reasons to choose a structured settlement is the favorable tax treatment. Workers compensation benefits—whether paid as weekly indemnity, lump sum, or structured settlement—are excluded from federal and state income tax under Section 104(a)(1) of the Internal Revenue Code. This exclusion applies to both the principal and any investment earnings generated by the annuity.

Why Workers Comp Structured Settlements Are Tax-Free

Unlike a personal injury settlement for non-physical injuries, workers compensation awards compensate for physical harm suffered on the job. Congress has long recognized that taxing these benefits would undermine their purpose: to replace lost wages and cover medical costs without leaving the injured worker worse off financially.

The tax exemption extends to the annuity's internal growth. If the life insurer credits your annuity with a 3% annual return, you receive the full benefit of that growth without owing tax on the gain. By contrast, if you take a lump sum and invest it in a taxable account, you will owe tax on dividends, interest, and capital gains, reducing your net return.

Author: Christopher Vaughn;

Source: avayabcm.com

Protecting Eligibility for Medicare and Medicaid

Structured settlements offer a strategic advantage for claimants who rely on means-tested public benefits. A large lump-sum payment can disqualify you from Medicaid, Supplemental Security Income, or subsidized housing because these programs count assets above certain thresholds. Structured settlement payments, however, are treated as income in the month received and do not accumulate as countable assets if spent down.

Careful planning can preserve eligibility. For example, you might structure payments to stay below the monthly income limit for your benefit program, or you might direct a portion of the settlement into a Medicare Set-Aside account that does not count against asset limits. A workers compensation settlement payment structure guide prepared by an elder law attorney or benefits specialist can map out these strategies.

Common Mistakes That Reduce Your Settlement Value

Negotiating a structured settlement is more art than science, and small missteps can cost you tens of thousands of dollars over the life of the annuity. Insurance adjusters are skilled at presenting structured proposals that look generous on paper but deliver less value than a well-negotiated lump sum.

Accepting the First Payment Structure Offered

Insurers often propose a payment schedule designed to minimize their upfront cost rather than maximize your financial security. A common tactic is to offer a long deferral period before payments begin, which reduces the annuity premium the carrier must pay today. If you agree to wait five years before your first payment, the present value of your settlement drops significantly, even if the total nominal payments remain the same.

Always ask your attorney to calculate the present value of any structured proposal using a reasonable discount rate—typically the current yield on U.S. Treasury securities with a similar duration. Compare that present value to the lump sum offer. If the structured settlement's present value is more than 10% lower, you are giving up substantial value for the convenience of periodic payments.

Ignoring Future Medical Cost Inflation

Healthcare costs have historically risen faster than general inflation. A structured settlement that pays $1,000 per month for medical expenses may cover your needs today, but in fifteen years that same $1,000 could buy half as much care. Failing to include a cost-of-living adjustment or an escalating payment schedule is one of the most common planning errors.

If your injury requires ongoing treatment—physical therapy, pain management, prescription drugs—negotiate for annual increases of at least 3% to keep pace with medical inflation. Yes, this reduces your initial payment, but it prevents a future crisis when your fixed income no longer covers your care.

Author: Christopher Vaughn;

Source: avayabcm.com

Failing to Include Cost-of-Living Adjustments

Even if your medical costs are fully covered by a Medicare Set-Aside, your living expenses will rise over time. Rent, utilities, groceries, and transportation all cost more each year. A structured settlement with no COLA effectively cuts your purchasing power by 2% to 3% annually, compounding over decades.

Some annuity providers offer fixed percentage increases (e.g., 2% per year) or adjustments tied to the CPI. The trade-off is a lower starting payment, but the long-term protection is worth it if you expect to receive payments for more than ten years.

The biggest mistake I see is workers accepting a structured settlement without understanding that the payment amount is fixed in nominal dollars. A client who settles at age forty-five and agrees to $2,000 per month until age sixty-five will find that $2,000 buys far less in year twenty than it did in year one. By failing to negotiate a COLA, they've locked in a declining standard of living. I always recommend at least a 2% annual increase for settlements expected to last more than a decade

— Michael Ramirez

When Selling or Modifying Your Structured Settlement Makes Sense

Life changes, and the payment schedule that seemed perfect at settlement may no longer fit your circumstances. You might face a medical emergency, need capital to start a business, or want to buy a home. Selling some or all of your future payments is possible, but it comes at a steep cost.

The Factoring Industry and Discount Rates

Companies that purchase structured settlement payments—often called factoring companies—offer you a lump sum today in exchange for the rights to your future payments. They calculate the lump sum by discounting your payments at a rate that reflects their cost of capital, administrative expenses, and profit margin. Discount rates in the factoring industry typically range from 9% to 18%, far higher than the rates used to price the original annuity.

If you are receiving $1,000 per month for ten years (a total of $120,000) and a factoring company offers you $70,000 today, you are giving up $50,000 in value. The company will collect the full $120,000 from the annuity issuer over time, pocketing the difference. In some cases, selling makes sense—if the lump sum prevents foreclosure or funds a medical procedure not covered by insurance—but you should exhaust other options first.

Author: Christopher Vaughn;

Source: avayabcm.com

Court Approval Process for Selling Future Payments

Federal law and most state statutes require court approval before you can sell structured settlement payments. The court must find that the sale is in your best interest, taking into account your financial situation, the discount rate, and whether you received independent legal advice. Judges are skeptical of sales driven by high-pressure tactics or unrealistic promises from factoring companies.

If you are considering selling, consult your original workers compensation attorney or a lawyer experienced in structured settlement transfers. They can help you evaluate competing offers, negotiate a lower discount rate, and present a compelling case to the court. Selling a small portion of your payments—say, two years' worth—may be a better option than liquidating the entire stream.

Planning Your Settlement Structure: Questions to Ask Before You Sign

A well-structured settlement aligns with your medical needs, financial goals, and family obligations. Before you finalize the agreement, work through these questions with your attorney and, if possible, a financial planner who understands workers comp settlement payments.

A workers compensation structured settlement can provide financial stability and peace of mind, but only if the payment schedule matches your real-world needs and the terms protect you from inflation and unforeseen expenses. The choice between a lump sum and a structured annuity is not binary; hybrid settlements that combine immediate liquidity with long-term income often deliver the best of both worlds.

State laws, tax rules, and insurance company practices all shape the final agreement, so working with an experienced attorney and, when appropriate, a financial planner is essential. Before you sign, verify the annuity issuer's credit rating, confirm that the payment schedule includes cost-of-living adjustments if you need them, and understand the consequences of selling payments in the future.

Your settlement must sustain you through recovery, replace lost earning capacity, and cover medical costs that may persist for decades. Taking the time to structure it correctly—rather than accepting the first offer—can mean the difference between financial security and hardship down the road.