Judge desk with gavel legal documents calculator and financial reports for structured settlement guardianship

Structured Settlement Rules for Court Appointed Guardians

Content

Picture this: a seventh-grader walks away from a catastrophic accident with $800,000 in compensation—money that needs to last her entire lifetime. Hand that kid the full check today? Any judge will laugh you out of court. They've seen what happens when teenagers or incapacitated adults suddenly control life-changing money. Bad financial decisions, predatory relatives, inexperience—courts understand these risks intimately.

Here's what trips up most guardians, though. Mess up these responsibilities and you're facing removal, personal financial liability, contempt of court. In serious cases? Fraud charges. Nobody gets excused for “meaning well.”

Every state enforces structured settlement guardianship rules with different thresholds, paperwork, timelines. But here's the constant: you're stepping into a fiduciary role with intensive court oversight. Detailed documentation requirements come with the territory. Cut corners? Prepare for serious consequences.

What Is a Structured Settlement Guardian and When Are They Required?

A structured settlement guardian manages periodic annuity payments for someone who can't legally handle money themselves. You'll receive scheduled payments from a life insurance company and make financial decisions on your ward's behalf. The court watches everything you do.

Guardian versus conservator—states throw these terms around inconsistently, which confuses everyone. California draws a clear line: conservators handle only financial matters while guardians manage both personal care and finances. Texas splits things differently: "guardian of the estate" covers financial management, "guardian of the person" handles healthcare decisions. Your court order defines your actual authority. The title matters less than what the paperwork says you can do.

Courts step in under two circumstances.

Minor beneficiaries can't legally accept significant settlement funds until hitting majority age—18 in most states, though Alabama and Nebraska make kids wait until 19. Each state sets different dollar triggers for mandatory court involvement. California's bar sits ridiculously low at $5,000. Florida's at $15,000. Texas draws the line at $10,000.

Incapacitated adults create the second scenario. Someone who suffered traumatic brain injury, lives with severe intellectual disabilities, battles advanced Alzheimer's disease—they can't manage complex financial decisions. Courts won't strip away an adult's autonomy without substantial medical proof, though. Neurological assessments, psychiatric evaluations, physician testimony about functional limitations—the evidentiary bar sits intentionally high because you're eliminating fundamental rights.

Dollar thresholds determine whether full guardianship becomes necessary or simpler alternatives work instead. Smaller settlements might qualify for "restricted account" options—money sits in a bank account needing court authorization for withdrawals, which avoids the paperwork burden of formal guardianship. A Georgia judge might approve this streamlined approach for a $30,000 settlement rather than establishing comprehensive oversight.

Parents walk in thinking they can treat their kid's injury settlement like household money. That's the mistake that gets them removed. This settlement might represent the only substantial income that child sees for decades. I'll hold you personally accountable for mismanagement. Don't expect me to accept ignorance as your excuse

— Cook County probate lawyer

Legal Duties and Fiduciary Responsibilities of Settlement Guardians

Courts evaluate your decisions through the "prudent person" lens. What's that mean? Manage these funds more carefully than you'd handle your own money. One person's entire financial future depends on you getting it right.

Three fundamental duties control everything you do. The loyalty duty means every decision must benefit your ward exclusively—your interests literally don't matter. The care duty requires thorough research and informed choices. The impartiality duty forces you to balance immediate needs against decades of future expenses—you can't drain accounts on current costs while ignoring what your ward needs twenty years down the road.

Self-dealing violates the loyalty duty automatically. Can you "borrow" guardianship money temporarily? Nope. Can you pay your ward's medical bill with your credit card, then reimburse yourself weeks later? Still no. Can you invest settlement funds in your brother's restaurant? Absolutely not. Courts void self-dealing transactions whether your ward ultimately profited or not.

Most states require surety bonds—basically insurance protecting the estate when guardians mismanage money. Bond amounts typically equal total estate value plus one year's expected receipts. Managing a structured settlement worth $500,000 that pays $30,000 annually? You're posting a $530,000 bond. Annual premiums run 0.5% to 1% of the bond amount, paid from estate funds. Judges sometimes waive bonds for institutional fiduciaries or when payment structures prevent lump-sum access anyway.

Author: Christopher Vaughn;

Source: avayabcm.com

Court Reporting and Accounting Requirements

Your judge monitors performance through annual accountings—exhaustive financial reports documenting every single dollar received and spent. You'll file these reports 60 to 90 days after each anniversary of your appointment. Don't treat this like some casual summary. You'll attach bank statements, spending receipts, explanations for anything questionable, complete inventories of remaining assets.

Local court rules dictate formatting. You'll typically provide:

- Last year's closing balance as your starting point

- Every receipt (structured payments, interest income, tax refunds, whatever came in)

- Every expenditure broken into specific categories (medical costs, educational expenses, living needs, etc.)

- Current balance with documentation showing where money sits

- Your spending plan for the upcoming year

Judges scrutinize expenditures for reasonableness. Buying your 10-year-old ward a $200 winter coat? Perfectly appropriate. Purchasing a $2,000 designer jacket? Better explain why that serves the ward's interests. Document unusual purchases completely: "Custom orthopedic footwear prescribed by Dr. Martinez following reconstructive surgery on left foot—$850" tells the full story. A receipt without context? That raises red flags immediately.

When estate values exceed $250,000 to $500,000, many states mandate CPA-prepared accountings. Costs more, but it adds credibility when expenditure decisions might otherwise face questions.

Investment Restrictions and Prohibited Actions

Settlement guardians face dramatically tighter investment limits than trustees managing other property types. Many court orders flatly prohibit investing structured settlement receipts, requiring you to deposit funds in FDIC-insured accounts earning virtually nothing. Why such conservatism? The structured settlement itself already provides investment growth through guaranteed future payments. Courts prioritize capital preservation over return maximization every single time.

When investment gets permitted, most jurisdictions limit you to ultra-conservative choices: Treasury bonds, investment-grade corporate debt, established mutual funds, bank certificates of deposit. You absolutely cannot touch:

- Individual corporate stocks (volatility risks the ward's only resources)

- Cryptocurrency (pure speculation masquerading as investment)

- Real property purchases (illiquid and uncertain)

- Loans to family members (obvious self-dealing)

- Business investments (inappropriate risk for irreplaceable settlement funds)

You can't modify structured payment schedules without court permission. You can't sell future payment rights to factoring companies—businesses that purchase payment streams at steep discounts—unless you satisfy stringent statutory criteria specifically designed to prevent exploitation.

State-by-state guardianship requirements comparison:

| State | Majority Age | Court Approval Threshold | Accounting Window | Bonding Requirements | Key Limitations |

| California | 18 | Yearly spending over $2,500 | 90 days after appointment anniversary | Required unless judge issues specific waiver | Mandatory Judicial Council forms; commingling strictly prohibited |

| Florida | 18 | Annual expenditures above $5,000 | 60-day window after appointment date | $10,000 minimum bond | Education expenses need detailed supporting documentation |

| Texas | 18 | Non-routine expenditures | 60 days once fiscal year ends | Corporate fiduciaries get exempted | Investment prohibited without explicit authorization |

| New York | 18 | Spending beyond routine maintenance | Judge determines filing schedule | Varies with total estate value | Office of Court Administration receives all filings |

| Illinois | 18 | Yearly spending above $5,000 | 60 days after appointment anniversary | Required absent specific waiver | Dedicated checking account mandatory; commingling strictly forbidden |

How to Set Up and Manage Guardianship Annuity Payments

Establishing guardianship over settlement funds typically happens simultaneously with settlement negotiations or immediately after parties reach agreement. Personal injury attorneys usually coordinate with guardianship counsel to draft court petitions while finalizing settlement terms.

Your guardianship petition packages several documents: the negotiated settlement agreement, medical records establishing minority or incapacity, background information about you as proposed guardian, comprehensive details about the structured annuity. Courts examine whether compensation fairly addresses injuries sustained, whether the payment schedule genuinely serves the beneficiary's needs, whether you're qualified to serve.

After the judge approves settlement terms and officially appoints you, the life insurance company funding the annuity demands specific documentation before issuing payments: certified copies of the guardianship order, your sworn fiduciary oath, letters of guardianship (official court credentials), W-9 tax forms establishing the correct taxpayer identification number.

Working with Structured Settlement Brokers and Life Insurance Companies

Structured settlement brokers connect defendants, their insurers, and the annuity companies actually funding payments. During initial setup, they design payment schedules matching your ward's anticipated needs. Maybe immediate payments covering ongoing medical treatment. Larger payments scheduled for college expenses in eight years. Final lump sums when guardianship terminates.

Here's a crucial distinction: you hold zero contractual relationship with the life insurance company issuing the annuity. The defendant or their insurance carrier purchases the annuity as settlement consideration. The annuity company's legal obligation runs directly to your ward—not to you personally. This contractual structure protects payments even if the defendant subsequently files bankruptcy.

Life insurance companies require current contact information and immediate notification about any guardianship status changes. When you resign or the court removes you, your successor guardian must provide updated credentials before the insurer redirects payments.

Payment delivery methods vary. Most companies provide direct deposit to your guardianship account, mail physical checks to your address of record, or—less frequently—direct payments into a structured settlement trust providing additional protection. Direct deposit eliminates lost-check risks and automatically creates documentation for your court accountings.

Payment Schedule Options and Distribution Methods

Structured settlements provide payment flexibility impossible with lump-sum settlements. You'll encounter several arrangements.

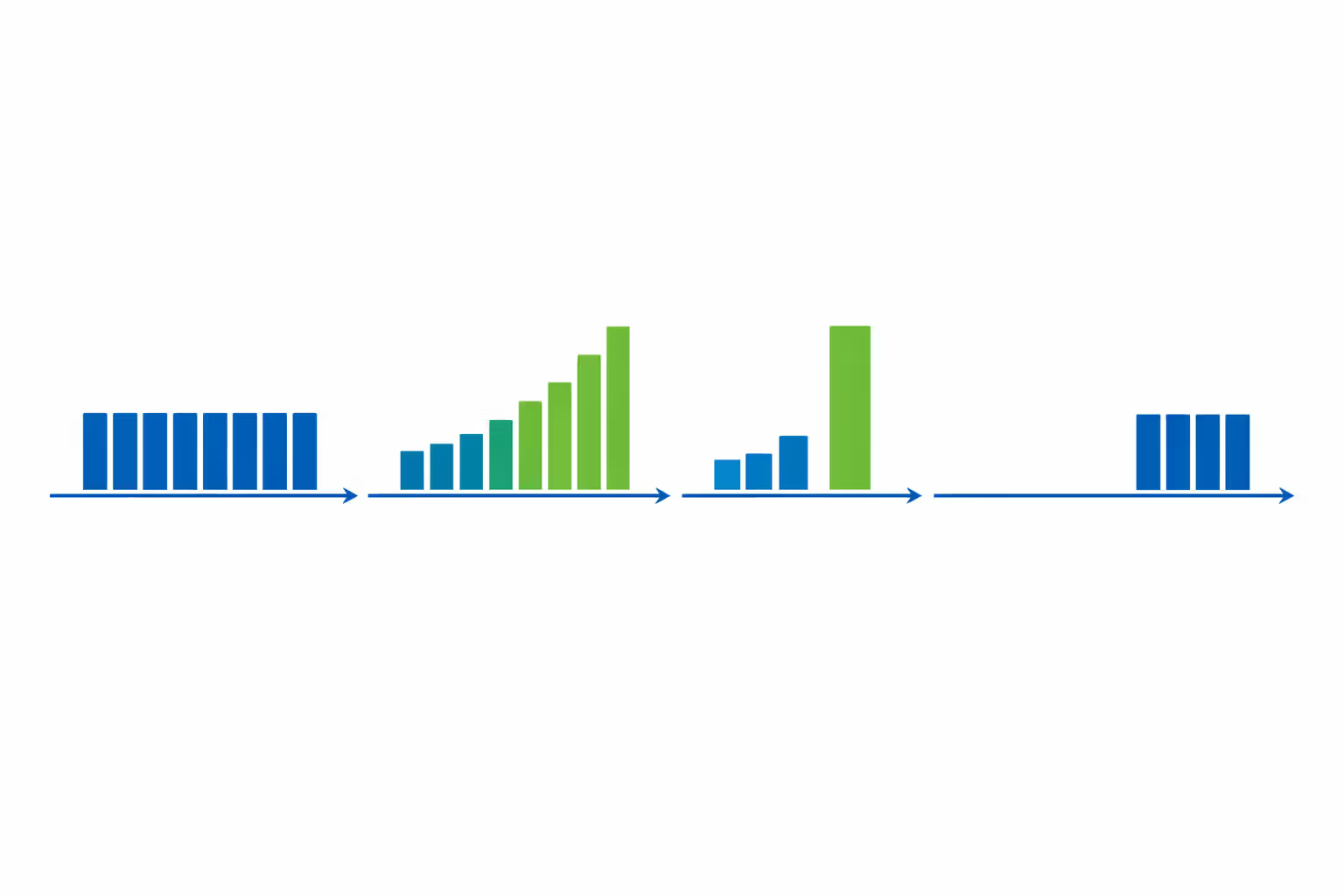

Level payments deliver identical amounts on a regular schedule throughout the payment period. Take a $500,000 settlement: it might distribute $2,000 monthly for 20 consecutive years, creating predictable income covering routine expenses.

Escalating payments start smaller and increase over time, addressing inflation and expanding costs as children mature. Payments might begin at $1,000 monthly, then climb 3% yearly.

Strategic lump sums blend regular smaller payments with periodic larger amounts targeting predictable major expenses. The structure might deliver $2,000 monthly for living costs plus $25,000 every four years earmarked specifically for college.

Deferred structures provide nothing initially, then commence regular payments years later. Works when immediate needs get covered through other means, with the settlement funding long-term care requirements decades down the road.

Lifetime payments continue for your ward's entire life span, regardless of longevity. This feature provides essential security for beneficiaries facing permanent disabilities.

Author: Christopher Vaughn;

Source: avayabcm.com

You can't unilaterally alter payment schedules once established. The annuity contract locks payment terms permanently. Modifying schedules requires either a court petition (addressed in the next section) or selling payment rights to a factoring company—something courts almost never approve when minors or incapacitated adults are involved.

Common Mistakes Guardians Make With Settlement Payments (And How to Avoid Them)

Commingling funds tops the violation list. Guardians deposit structured payments into personal checking accounts "temporarily" or because they don't understand the absolute prohibition. Courts treat commingling as automatic evidence of mismanagement, even when you meticulously tracked which money belongs to your ward. Solution: open a separate account titled "Jane Doe, a minor, by John Doe, Guardian" immediately upon appointment. Mix funds at your peril—not even briefly.

Unauthorized spending happens when guardians exceed statutory spending caps without obtaining court approval first. Your ward needs emergency surgery costing $10,000, so you withdraw funds from the guardianship account intending to seek court approval afterward. Terrible mistake. Courts can surcharge you personally for unauthorized expenditures, forcing you to reimburse the estate from your personal assets even when the spending obviously helped your ward. Better approach: file an emergency petition immediately. Most judges grant legitimate emergency requests within one to three days.

Missing court deadlines triggers sanctions ranging from removal to contempt citations. You're juggling employment, family obligations, guardianship responsibilities—the annual accounting deadline slips your mind, or you figure a three-week delay doesn't matter. Wrong assumption. Courts manage hundreds of guardianship matters and depend on timely information to fulfill oversight obligations. Calendar all deadlines the day you're appointed. Create reminders one month and two months beforehand. If you'll miss a deadline despite genuine effort, file an extension motion before the deadline expires.

Inadequate documentation leaves you unable to prove expenditures when accounting season arrives. Receipts disappear, credit card statements get discarded, you're reconstructing six months of spending from memory. Courts reject unsupported expenditures, potentially surcharging you for amounts you actually spent appropriately but can't prove. Maintain a dedicated file—physical or digital—for every single receipt, bank statement, correspondence. Photograph receipts immediately because thermal paper fades. Annotate each receipt: "Physical therapy copay per Dr. Smith's referral 3/15/24" provides context.

Skipping accountings entirely represents the gravest error. Some guardians skip filings completely, sometimes for years, then face removal and potential criminal charges when investigation reveals misappropriation. Other guardians mistakenly believe that if they haven't spent money, they don't need to file. Wrong again. Courts require accountings showing current balances and confirming no unauthorized activity occurred. Even a simple accounting showing "opening balance: $50,000; received: $12,000 in structured payments; spent: $0; closing balance: $62,000" satisfies the requirement.

Modifying or Terminating Settlement Payment Agreements Under Guardianship

Once structured settlement payment schedules get established, changing them becomes incredibly difficult. The annuity contract locks payment amounts and timing contractually. However, you've got two potential paths forward if circumstances change dramatically: petition the court for approval to sell payment rights, or petition to restructure the settlement itself (rarely successful).

The Structured Settlement Protection Act—adopted in various forms by most states—governs sales of future payment rights to factoring companies. These companies purchase the right to receive future payments at substantial discounts, providing immediate cash. Example: a factoring company might pay $80,000 today for the right to receive $120,000 in payments over five years.

Author: Christopher Vaughn;

Source: avayabcm.com

Courts scrutinize these transactions intensely when guardians get involved. You must prove:

- The transfer genuinely serves your ward's best interest

- Your ward received independent professional advice

- The discount rate isn't predatory

- The transfer won't leave your ward without adequate future resources

- Your ward consents (if they possess capacity to do so)

Judges deny most petitions involving minors unless extraordinary circumstances exist: experimental medical treatment insurance won't cover, a special needs trust urgently requires funding, the family faces homelessness without immediate funds. Courts reason that structured settlements exist precisely to prevent premature fund depletion—approving sales defeats that fundamental purpose.

Petitions to restructure settlements—changing payment amounts or timing within the existing annuity—require consent from both the life insurance company and the court. Insurance companies rarely agree because restructuring creates administrative headaches and potential adverse selection problems (beneficiaries in poor health might seek accelerated payments, leaving the company with unfavorable longevity risk).

When guardianship terminates—typically when a minor reaches 18 or an incapacitated adult regains capacity—structured settlement payments continue directly to the former ward. You file a final accounting, obtain court approval, transfer any accumulated funds to the beneficiary. The annuity company updates its records to send payments to your former ward's personal account.

Some settlement agreements include provisions for payments continuing in trust if the beneficiary lacks financial maturity at majority age. These trusts extend professional management beyond guardianship termination, protecting beneficiaries from impulse spending while preserving eventual access to funds.

Tax Implications and Reporting Requirements for Guardian-Managed Settlements

Structured settlement payments from personal injury cases arrive tax-free under Internal Revenue Code Section 104(a)(2), which excludes damages received for physical injuries or physical sickness. This favorable tax treatment extends to periodic payments from structured settlements—your ward doesn't pay federal income tax on the payments themselves.

However, you must distinguish between the tax-free settlement payments and taxable investment income those payments generate. If you deposit a $5,000 monthly payment into a savings account earning interest, the $5,000 stays tax-free but the interest is taxable. Guardianship estates must file Form 1041 (U.S. Income Tax Return for Estates and Trusts) when gross income exceeds $600 annually.

Author: Christopher Vaughn;

Source: avayabcm.com

Your guardianship estate needs its own Employer Identification Number (EIN) obtained from the IRS. You can't use your personal Social Security number or your ward's SSN for guardianship accounts. Banks require the EIN to open guardianship accounts and report interest income properly.

Each state handles taxation differently. While most states follow federal treatment by exempting personal injury settlement payments from state income tax, they vary on how they tax investment income from guardianship estates. California, for example, taxes guardianship estate income at trust tax rates, which hit the highest marginal rate at much lower income levels than individual rates do.

Maintain separate records distinguishing tax-free settlement receipts from taxable income. Your annual accounting should clearly show: "Structured settlement payments received (tax-free): $60,000; Interest earned on guardianship account (taxable): $1,200; Capital gains from court-approved investments (taxable): $3,500."

Punitive damages receive different tax treatment when included in settlements. These amounts are taxable as ordinary income even when paid as part of a personal injury settlement. Settlement agreements should clearly allocate amounts between compensatory damages (tax-free) and punitive damages (taxable) to prevent confusion.

Skip required tax return filings and you expose the guardianship estate to penalties and interest. The IRS assesses penalties of $205 per month (adjusted annually for inflation) for failure to file Form 1041 when required. State taxing authorities impose their own separate penalties. More significantly, courts view tax compliance failures as evidence of mismanagement, potentially leading to your removal.

Frequently Asked Questions About Settlement Guardianship

Managing structured settlement funds as a guardian carries massive responsibility—but that's exactly why these protections exist. Courts don't expect perfection from you. They expect honesty, diligence, genuine commitment to your ward's welfare. Keep detailed records, seek court approval before taking questionable actions, prioritize your ward's long-term security over short-term convenience. Follow these principles and you'll avoid serious problems.

The guardianship settlement payments guide principles outlined here apply broadly across states, but state-specific rules govern your particular situation. Consult with a guardianship attorney in your jurisdiction before making significant decisions. The relatively modest cost of professional advice pales compared to potential consequences of errors.

When doubt arises about whether particular expenditures require court approval or whether proposed actions fall within your authority, err on the side of transparency. File a petition asking the court's guidance. Judges appreciate guardians who seek direction rather than acting unilaterally and requesting forgiveness later.

Structured settlement guardianship rules exist to serve one purpose: ensuring that funds meant to provide for an injured or incapacitated person's lifetime needs actually accomplish that goal. Keep that purpose front of mind and you'll navigate the technical requirements successfully while fulfilling your most important duty—protecting someone who can't protect themselves.