Parent sitting at kitchen table reviewing legal settlement documents with a check, children’s room visible in background

Structured Settlement for Minors Guide for Parents

Content

Your eight-year-old daughter just won a $400,000 settlement after a car accident left her with permanent nerve damage. The defense attorney's check sits on your kitchen table. You're ready to deposit it and start planning her future. Then your lawyer delivers unexpected news: a judge must approve exactly how this money gets distributed, and you won't simply walk away with a lump sum.

Personal injury compensation for children works nothing like adult settlements. Courts won't hand over large sums to parents without detailed safeguards. The legal system learned hard lessons from cases where settlement money vanished within months—spent on family vacations, bad investments, or simply absorbed into general household expenses while the injured child's future needs went unmet.

That's where structured settlements enter the picture, converting one-time payouts into payment streams designed around your child's anticipated needs over their lifetime.

What Makes Structured Settlements Different for Minors

Think of a structured settlement as transforming a single check into scheduled payments—sometimes dozens of them—spread across years or decades. Your daughter's $400,000 might become $1,800 monthly until she turns 18, then $60,000 when she starts college, another $75,000 at 25, with monthly payments resuming afterward.

Here's how it works mechanically: settlement dollars purchase an annuity contract from a highly-rated insurance company. That insurer commits to making payments following the court-approved timeline. No stock market involvement. No investment decisions. Just guaranteed payments arriving on schedule.

What separates minor settlements from adult cases? Mandatory judicial review. California, Texas, New York, Florida—every state demands that a judge personally approve any settlement involving a child, whether it's $25,000 or $2.5 million. Adults can do whatever they want with their money. Kids can't, which means parents can't either.

The reason traces back to basic contract law. Minors lack legal capacity to enter binding agreements. They can't manage substantial assets. Courts step in as protectors because too many families discovered that sudden wealth disappears faster than anyone expects.

Parents come to me thinking they'll invest the money wisely for their child. Six months later, half of it's gone—not through malice, just life happening. Medical bills pile up. The family car dies. Someone gets laid off. Without court-enforced structure, settlement money becomes the family emergency fund instead of the child's protected compensation

— Sarah Mitchell

Structured settlements create barriers that feel restrictive but serve critical purposes. Parents can't borrow against future payments. The child can't sell their payment rights impulsively at 19. Creditors can't touch the funds, even if the family faces bankruptcy. These limitations exist specifically because settlements without them so often ended badly.

Judges don't just rubber-stamp proposed structures. They examine whether the payment schedule matches the injury's severity and the child's projected needs. A settlement that pays everything by age 21 might get rejected if medical evidence shows ongoing treatment needs extending into middle age. Courts ask tough questions: Will this structure actually protect this specific child? Have alternatives been seriously evaluated? Are there conflicts between the parents' immediate financial pressures and the child's long-term welfare?

How Minor Settlement Structured Payments Work

The annuity backing a child's settlement bears little resemblance to retirement annuities your parents might own. These instruments guarantee specific payment amounts on specific dates, period. Market crashes don't affect them. Interest rate swings don't change them. The insurance company's investment performance doesn't touch them. Once the judge signs off, those payment amounts and dates become contractual obligations that persist for decades.

Most payment designs blend several components. Monthly or quarterly payments handle ongoing expenses—therapy appointments, specialized tutoring, adaptive equipment that needs regular replacement. Lump sums timed to education milestones cover tuition and housing. Larger payments at ages 25, 30, or 35 provide capital for home purchases, business starts, or retirement account funding.

Author: Andrew Halvorsen;

Source: avayabcm.com

Before court approval, customization options are nearly unlimited. After approval? Changes require another court petition, which means the initial design carries enormous weight.

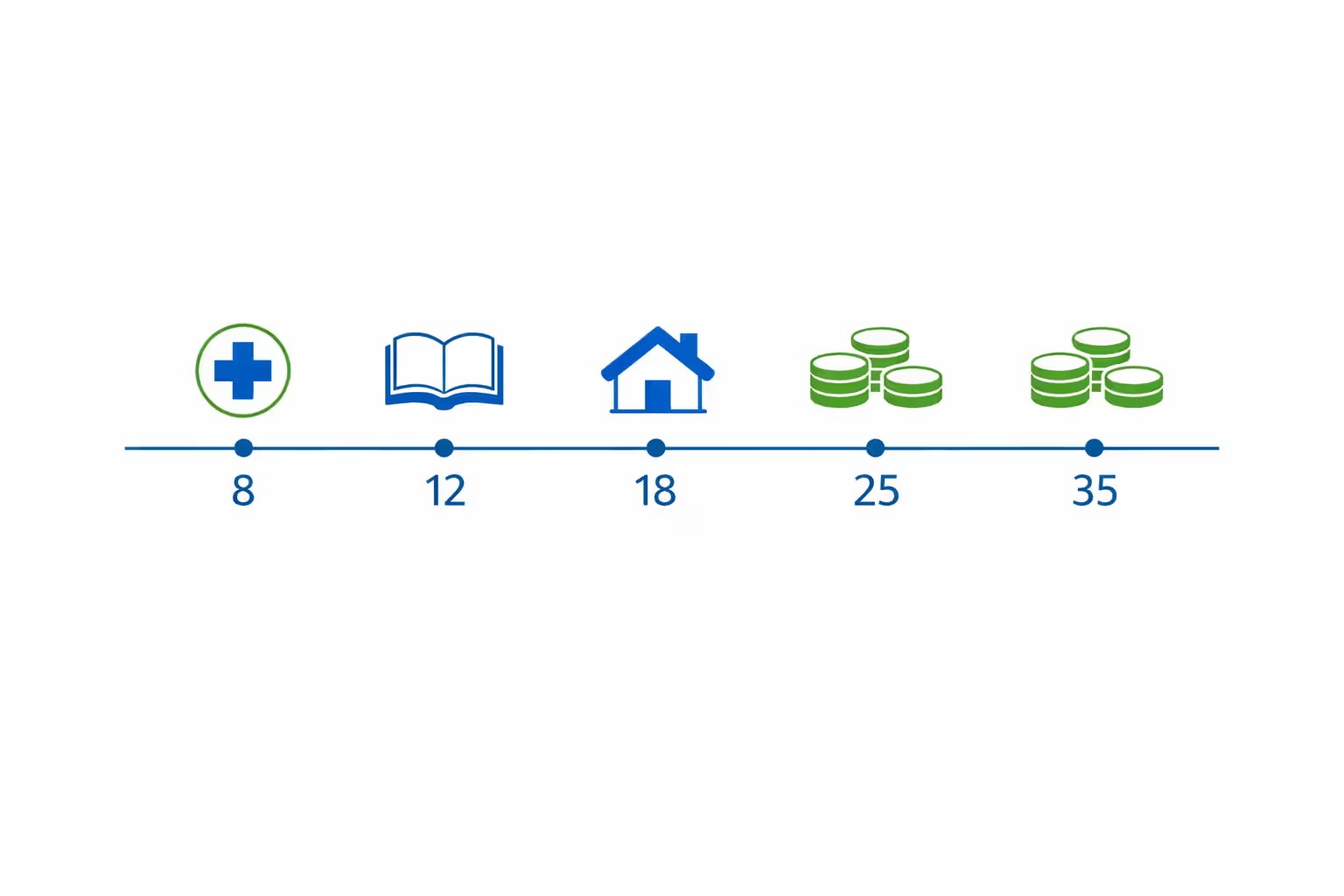

Consider a moderate $180,000 settlement for a 12-year-old boy whose arm fracture healed poorly, limiting future job prospects. His parents might structure it as: - $800 monthly from age 12 to 18 ($57,600 total) for physical therapy and equipment - $45,000 at age 18 for vocational training or community college - $2,200 monthly from age 23 to 33 ($290,400 total) supplementing reduced earning capacity - $60,000 at age 35 for a home down payment

That $180,000 settlement delivers roughly $453,000 through tax-free annuity growth over 23 years—more than 2.5 times the original amount.

Common Payment Schedule Examples

Settlements under $200,000 where the child recovered fully often emphasize education and young adult transition. Take $140,000 for a broken leg with no permanent damage: $600 monthly until age 18 covers any residual therapy ($43,200 total), $50,000 arrives for college expenses, and $65,000 comes at age 25 when the young adult establishes career and housing.

Severe injury settlements exceeding $750,000 typically create lifetime income frameworks. A child facing permanent mobility limitations might receive $3,200 monthly for life, with payment increases at 18 (to $4,500), 30 (to $5,800), and 50 (to $7,200) acknowledging inflation and changing care costs. Add $85,000 at age 19 for an adapted vehicle and $110,000 at age 28 for home accessibility modifications.

Wrongful death settlements where children survive a parent usually defer most payments until young adulthood. The surviving parent often handles immediate needs. The settlement replaces what the deceased parent would have provided later—educational funding, wedding contributions, first home assistance. Payments might not start until age 18, then deliver substantial sums at 18, 22, and 26.

When Payments Can Begin

Immediate-need scenarios justify starting payments within 30-45 days of court approval. If your child needs ongoing occupational therapy three times weekly at $180 per session, that's $28,080 annually. Monthly payments covering that expense plus adaptive equipment makes sense when those costs are real and current.

Deferring payments makes sense when immediate needs are manageable through insurance or family resources. Waiting lets the annuity grow longer before making payments. A $250,000 settlement starting payments immediately might deliver $420,000 over 25 years. That same $250,000 deferred for seven years could deliver $560,000 because of the additional growth period.

Some families blend approaches—modest payments during childhood for genuine current needs, with the bulk deferred until the child reaches adulthood and can better understand the settlement's significance.

Court Approval Process for Child Injury Settlement Payments

The approval process kicks off after your attorney finalizes settlement terms with the defendant but before any money moves. Your lawyer files a formal petition with the court detailing the proposed settlement amount, explaining the payment structure, and arguing why this arrangement serves your child's best interests. Attached documents include medical records establishing injury severity, expert opinions projecting future care needs, and financial analyses showing how the structure meets anticipated expenses.

Judges scrutinize multiple factors: Does the total amount fairly compensate the injury? Does the payment timing align with when needs will arise? Are the insurance companies financially solid enough to make payments 30 years from now? Have reasonable alternatives been explored and rejected for good reasons?

Author: Andrew Halvorsen;

Source: avayabcm.com

Many jurisdictions—especially for settlements topping $100,000 or involving catastrophic injuries—appoint a guardian ad litem. This court-appointed attorney works exclusively for your child's interests, not yours or your lawyer's. They interview doctors, review financials independently, and ensure no conflicts exist where parents' immediate financial stress might compromise the child's long-term security. Their report to the judge matters enormously. A negative recommendation can torpedo a settlement structure even if both sides agreed to it.

Timing varies wildly. Straightforward cases—clear liability, documented injury, reasonable settlement, well-designed structure—might win approval in 30-60 days. Complex situations involving disputed facts, uncertain future medical needs, or family disagreements stretch to four or six months. Courts prioritize getting it right over getting it done quickly, recognizing that approval mistakes can't easily be fixed later.

State rules vary significantly. California mandates public hearings where anyone can object. Texas allows streamlined procedures for certain settlements under $100,000. New York requires specific contractual language and restricts which financial institutions can hold blocked accounts. Florida has different procedures for medical malpractice versus other injury types. Working with local counsel who handles these cases regularly prevents procedural mistakes that delay approval.

Tax Advantages and Financial Protection Benefits

Here's where structured settlements shine brightest: complete tax exemption. Internal Revenue Code Section 104(a)(2) excludes personal physical injury compensation from taxable income—not just the initial settlement, but all future growth too. A $350,000 settlement growing to $710,000 over 22 years generates zero tax liability. Your child receives every dollar.

Compare that to investing a lump sum. Even the most tax-efficient portfolio spins off taxable income annually through dividends, interest, and capital gains. A $350,000 investment earning 5.5% annually produces $19,250 in Year One alone. Depending on your family's tax bracket and your child's other income, 20-35% might disappear to taxes. Compounded over two decades, tax drag can consume $200,000 or more—money that structured settlements preserve completely.

| Feature | Structured Settlement | Lump Sum Investment |

| Tax Treatment | Growth and payments both completely tax-free under IRC §104(a)(2) | Earnings taxed annually as ordinary income, capital gains, or dividends |

| Court Oversight | Ongoing protection requiring court permission for any changes | Initial approval only; no supervision once funds are released |

| Access/Liquidity | Fixed schedule; accessing funds early requires court petition | Parents or guardians control spending; money easily accessed |

| Protection from Misuse | Payments can't be sold, borrowed against, or transferred | Vulnerable to impulsive decisions, family pressure, or fraud |

| Growth Potential | Guaranteed returns with zero market risk | Potentially higher returns but with substantial loss risk |

| Flexibility | Very limited; schedule largely fixed when created | Complete flexibility to adjust investment strategy anytime |

| Creditor Protection | Payments fully shielded from creditors and bankruptcy claims | Often seizable by creditors depending on state law |

Creditor protection works differently than standard bankruptcy exemptions. Traditional asset protection has limits and exceptions. Structured settlements enjoy broader protections—even if your child later faces lawsuits, business failures, or divorce proceedings, their settlement payments remain untouchable in most jurisdictions. This shield lasts throughout the entire payment period, offering security that invested money simply cannot match.

Spendthrift clauses prevent your child from selling, assigning, pledging, or borrowing against future payments. While companies do buy structured settlement payment rights, transactions involving minors face additional legal hurdles specifically designed to prevent defeating the settlement's protective purpose. These restrictions might frustrate an 18-year-old who wants $50,000 immediately to start a business, but they prevent the impulsive decisions that have left countless young adults with empty bank accounts and decades of lost compensation.

Choosing the Right Annuity Provider and Payment Structure

Financial strength ratings matter more for children's settlements than any other annuity category because payments might continue 40, 50, even 60 years into the future. Only insurance companies carrying A ratings or higher from A.M. Best, or AA or better from Standard & Poor's, deserve consideration. The company's financial stability determines whether your child actually receives payments in 2055 or 2070.

Ask these questions before finalizing anything: What happens if the insurance company fails? (State guaranty associations provide backup coverage, but limits vary—often $250,000 to $500,000 per person depending on the state.) Can we modify the payment schedule if life takes unexpected turns? (Usually no, making initial planning absolutely critical.) Do any fees or administrative charges reduce the payment amounts? (Quality structures have zero ongoing fees—if someone mentions charges, that's a red flag.) What happens if my child dies before receiving all scheduled payments? (Beneficiary provisions need explicit documentation.)

Watch for these warning signs: Anyone pressuring you to accept a structure without adequate review time. Providers projecting unusually high payments that significantly exceed competitors' offers for the same premium. Reluctance to provide detailed information about the insurance company's financial history and current ratings. Suggestions to structure only partial amounts without clearly explaining why a hybrid approach benefits your child specifically.

Build a professional team. Your personal injury attorney negotiates the settlement and shepherds the court approval process. A financial planner experienced specifically with structured settlements—not just general financial planning—helps design payment schedules matching your child's anticipated needs across their lifetime. A tax advisor confirms the structure qualifies for tax-free treatment and coordinates with any special needs trusts or government benefits considerations. Cutting corners to save advisory fees often produces suboptimal structures that can't be corrected later.

Common Mistakes Parents Make When Planning Child Structured Settlements

Author: Andrew Halvorsen;

Source: avayabcm.com

The biggest planning error? Underestimating future needs by focusing too narrowly on current expenses. Your child is 11 years old today, facing 60-plus years of life ahead. Current therapy costs and immediate equipment needs are obvious. Less obvious: adaptive technology requiring replacement every 5-7 years, transportation costs that increase dramatically when your child can't use public transit easily, housing modifications that won't be necessary until independent living begins, and employment limitations that reduce lifetime earnings by hundreds of thousands of dollars.

Inflexible payment schedules create problems when life doesn't follow predicted paths. A structure assuming college attendance at 18 fails if your child needs gap years for additional recovery, pursues vocational certification instead of university, or takes longer to complete degrees due to disability accommodations. Building in flexibility—perhaps educational funding available between ages 18-24 rather than only at 18, or monthly living expense payments usable for various purposes rather than designated narrowly—provides adaptation room.

Inflation destroys purchasing power silently but devastatingly over time. A $2,400 monthly payment feels substantial today. At just 2.5% annual inflation, it feels like $1,440 in 20 years. Better structures include periodic payment increases or cost-of-living adjustments tied to CPI. Even modest 2% annual increases preserve purchasing power far better than flat payments.

Special needs trusts get overlooked regularly, sometimes disqualifying children from benefits worth more than the settlement itself. Children with significant disabilities often qualify for Supplemental Security Income and Medicaid—means-tested programs with strict asset and income limits. A structured settlement paid directly to your child might exceed those limits, causing benefit loss. SSI might "only" provide $900 monthly, but Medicaid coverage can be worth $3,000-$5,000 monthly in medical expenses. Properly drafted special needs trusts receive settlement funds without triggering disqualification, preserving both the settlement and government benefits.

Rushing the approval process to access funds faster occasionally produces poorly designed structures that don't genuinely serve your child's long-term interests. Medical bills are piling up. Therapy costs are mounting. The pressure to finalize everything quickly feels overwhelming. But a few extra weeks refining the payment schedule can mean the difference between a settlement supporting your child through retirement versus one exhausted before they turn 30. Take the time to get it right.

Frequently Asked Questions About Minor Structured Settlements

A structured settlement transforms one-time legal compensation into financial security spanning your child's lifetime. The mandatory court oversight, complete tax exemption, and creditor protections create safeguards impossible to replicate with lump-sum settlements. Children whose compensation might otherwise vanish before they finish college instead receive income precisely when the injury's impact hits hardest—starting higher education despite disabilities, establishing independent living, funding ongoing medical needs into middle age and beyond.

The best settlements result from careful planning balancing immediate necessities against long-term security. Parents who invest time understanding payment options, vetting annuity providers' financial strength, and building teams of experienced advisors create frameworks supporting their children for decades. Avoiding common pitfalls—underestimating future needs, accepting inflexible schedules, ignoring inflation, overlooking special needs trusts—demands patience during an already exhausting period, but the decades-long benefits justify the extra weeks spent refining the structure.

Courts protect children's interests when parents face conflicting pressures or lack expertise in long-term financial planning. Rather than viewing judicial oversight as bureaucratic frustration, families who embrace the process as an additional safeguard often discover that court involvement improves their final settlement structure. Judges and guardians ad litem contribute objective perspectives identifying potential problems families might miss while dealing with medical crises and emotional trauma.

Your child's settlement compensates harm that can never be undone. Structuring those funds to deliver maximum benefit throughout their lifetime honors the settlement's purpose and ensures the compensation genuinely improves your child's future opportunities, independence, and quality of life well into their retirement years.