Person’s hand hesitating between a single large settlement check and a structured payment schedule document on a law office conference table

Personal Injury Structured Settlement Guide to Payments, Taxes, Benefits

Content

You've just settled your injury case for $800,000. The defense attorney slides two documents across the table. One shows a single check for the full amount, minus your lawyer's fee. The other outlines monthly payments of $3,200 stretching across the next 25 years.

Which do you choose?

Most people grab the lump sum without thinking twice. That's often the wrong move.

Personal injury structured settlements transform your one-time payout into a series of scheduled payments. Instead of depositing everything into your checking account on Tuesday, you receive predictable income on specific dates—monthly, quarterly, annually, or following whatever custom schedule you negotiate.

The insurance company that's paying you doesn't just promise to send checks. They purchase an annuity from a life insurance carrier, which then becomes legally obligated to make your payments. This isn't like your cousin promising to pay you back "eventually." It's a binding contract backed by state guaranty associations.

Here's what makes injury settlements different from other structured payment deals: the tax treatment. Win the lottery and structure those payments? You'll pay income tax on the earnings portion. Settle an employment discrimination case with periodic payments? Same problem—taxable income. But compensation for bodily harm comes with special IRS treatment that eliminates taxes on both the principal and the growth inside the annuity.

That tax advantage alone can mean $100,000+ more in your pocket over a 20-year period compared to taking a lump sum and investing it yourself.

The catch? You're locked in. Change your mind next year? Too bad. Need extra cash for an emergency? You'll pay dearly to access it. Pick the wrong payment schedule now, and you'll regret it for decades.

I've watched injury victims make catastrophic decisions in this moment—structuring 100% of their settlement when they needed immediate cash for medical bills, or taking everything as a lump sum and blowing through $500,000 in eighteen months. Your attorney has probably seen it too, which is why the good ones insist you understand exactly what you're agreeing to.

What Is a Structured Settlement in Personal Injury Cases?

When the insurance company offers you a structured settlement, they're proposing to replace your single payment with an income stream spread across time. You might receive $2,000 every month for fifteen years. Or $50,000 annually for a decade. Or nothing for five years, then $4,500 monthly for life after that.

The mechanics work like this: the defendant's insurer transfers their obligation to pay you to what's called an "assignment company." This assignment company then purchases an annuity contract from a life insurance carrier—usually one with an A+ or better rating from AM Best. That annuity contract specifies exactly when you get paid, how much, and for how long.

You become the "payee" and "measuring life" on the annuity, but you don't own it. The assignment company owns it. This legal separation matters enormously for the tax benefits we'll discuss later.

Author: Andrew Halvorsen;

Source: avayabcm.com

Contrast this with taking a lump sum. The insurance company cuts you one check. Done. Finished. No ongoing relationship. No future obligations. You deposit that money in your bank account, and from that moment forward, everything that happens to those funds is your responsibility. If you invest wisely and earn 8% annually, great. If your brother-in-law talks you into funding his cryptocurrency venture and you lose everything, that's on you.

Structured settlements emerged in the 1970s after courts and legislators noticed a disturbing pattern. Injury victims—particularly those with severe, permanent disabilities—were receiving substantial settlements, then showing up in bankruptcy court or on public assistance rolls within a few years. A catastrophically injured worker might get $2 million, spend it on a new house and some bad investments, and find himself broke with 40 years of medical expenses still ahead.

The legal framework that enables these arrangements is called "qualified assignment." The defendant assigns their obligation to pay you to a third party, which triggers specific tax code provisions. This assignment must be irrevocable and cannot be accelerated, deferred, increased, or decreased by you. The rigidity is what creates the tax benefits.

Most personal injury cases can be structured: car wrecks, medical malpractice, slip-and-fall accidents, defective product injuries, workplace accidents, and assault cases. The fundamental requirement is that your settlement compensates you for physical injuries or physical sickness. Purely emotional distress claims don't qualify unless the emotional distress stems from a physical injury. Property damage settlements don't qualify either.

How Structured Settlement Payments Are Calculated and Distributed

Let's say you're settling your case for $600,000. The insurance company doesn't just divide that by 240 months and send you $2,500 monthly for twenty years. The math involves interest rates, life expectancy tables, annuity costs, and time value of money calculations.

The assignment company shops your case to several life insurance carriers who underwrite annuities. Each carrier looks at current interest rates, their investment portfolio yields, administrative costs, and profit margins. They then quote what payment stream they can provide for the $600,000 premium.

In today's interest rate environment (early 2025), that $600,000 might purchase $2,800 monthly for 20 years. Or $45,000 annually for 18 years. Or $5,200 monthly for 12 years. The insurance company provides multiple options showing different combinations of payment amounts and durations.

Interest rates dramatically affect these calculations. Back in 1985, when Treasury bonds yielded 10%+, your $600,000 could purchase much larger payment streams than today. This creates strategic timing considerations—if you're settling during a low-rate period, you might push for a larger overall settlement amount to compensate for reduced annuity purchasing power.

The Role of Annuities in Injury Settlements

The annuity isn't some variable investment product tied to the stock market. We're talking about single-premium immediate annuities (SPIAs) specifically designed for injury settlements. The assignment company pays one lump sum to the life insurance carrier, which then guarantees specific payments on specific dates, regardless of what happens in financial markets.

Think of it as the insurance company making a bet. They're betting they can take your $600,000, invest it conservatively in government bonds and investment-grade corporate debt, generate enough returns to make all your scheduled payments, and still have a bit left over as profit. They're sophisticated investors with huge portfolios, so they're comfortable making that bet at the quoted payment levels.

Your payments come from a combination of principal and investment earnings, structured so the annuity exhausts itself exactly when the last payment is due (or continues indefinitely if you've chosen a lifetime payment option).

The insurance carrier matters. You want a company that'll still exist in 30 years to make your final payments. That's why structured settlement annuities typically come from the largest, highest-rated life insurance companies—MetLife, New York Life, Pacific Life, MassMutual, and similar carriers with fortress balance sheets and century-long operating histories.

When rates are higher, your settlement dollars buy bigger payment streams because the insurance company can earn more on their investments. When rates drop—like they did between 2008-2021—the same settlement amount generates smaller payments. Your attorney should be monitoring rate environments and timing settlement finalization strategically when possible.

Author: Andrew Halvorsen;

Source: avayabcm.com

Payment Schedule Options: Periodic vs. Deferred Payments

You're not stuck with simple monthly checks. The payment structure can be customized to match your actual anticipated needs, which is one of the strongest arguments for choosing structured payments over lump sums.

Want nothing for three years while you recover and get back to work, then monthly income starting in year four? Done. Need $3,000 monthly for living expenses plus a $75,000 lump sum in year seven when your daughter starts college and another $50,000 in year twelve when you'll need spinal surgery? No problem. Prefer payments that increase 3% annually to keep pace with inflation? That's an option too.

Some claimants choose immediate periodic payments starting within 60 days of settlement. This works well if you've lost income and need to replace your paycheck right away. The payments continue at regular intervals—monthly is most common, but quarterly and annual payments are also available.

Deferred payments delay the start date, sometimes by decades. A 30-year-old plaintiff might defer payments until age 65, effectively creating a pension. The annuity grows during the deferral period, which means the same premium purchases larger payments than if they started immediately. A $400,000 premium deferred for 35 years might generate $6,000 monthly for life starting at 65, whereas immediate payments might only provide $2,200 monthly.

Hybrid structures give you both immediate cash and long-term security. Take $150,000 as a lump sum to pay off medical bills, buy an accessible vehicle, and create an emergency fund. Structure the remaining $450,000 for monthly income. This approach addresses the valid criticism that structuring everything leaves you with no liquidity.

| Payment Type | How It Works | Best For | Example Scenario |

| Immediate periodic | Regular payments start within 60 days, continue at set intervals throughout the payment period | Replacing lost wages, covering ongoing medical costs, paying daily living expenses when you have no other income | $2,800 monthly for 20 years beginning two months after settlement, total payout $672,000 from $550,000 premium |

| Deferred periodic | No payments for months or years, then regular payments begin and continue for specified period or lifetime | Younger injury victims who have current income but need future retirement security | Zero payments for 8 years, then $4,500 monthly for life beginning at age 62, funded by $350,000 premium |

| Lump sum + periodic hybrid | Immediate lump sum payment followed by regular scheduled payments on whatever intervals you choose | Pressing immediate bills combined with long-term income needs, or maintaining some liquid reserves while securing future payments | $125,000 upfront, then $2,100 monthly for 15 years, total payout $502,000 from $425,000 settlement |

| Increasing payments | Payments rise each year by fixed percentage or dollar amount to offset inflation's erosion of purchasing power | Long-term payment schedules where maintaining buying power matters, especially for younger claimants | $2,200 monthly in year one, increasing 2.5% annually for 25 years, ending at $4,000+ monthly in final years |

Once you finalize the payment schedule, it's set in stone. You can't call the insurance company next year and say "instead of monthly payments, I'd like everything right now." You can't skip a few payments to take a larger amount later. You can't accelerate the schedule if you need money sooner.

This inflexibility is the price of the tax benefits and guaranteed income. It's also why choosing the right structure from the beginning matters so much.

Tax Advantages and Financial Rules Governing Structured Settlements

The federal tax code treats money you receive for bodily injuries differently from virtually every other type of income. Section 104(a)(2) of the Internal Revenue Code says that if you receive damages because of personal physical injuries or physical sickness, you don't pay income tax on that money.

This applies whether you take a lump sum or structured payments. Either way, it's tax-free.

So what's the tax advantage of structuring?

Author: Andrew Halvorsen;

Source: avayabcm.com

With a lump sum, you receive tax-free dollars, but then you're responsible for investing them. Those investments generate interest, dividends, and capital gains—all taxable. Even in tax-advantaged accounts like IRAs, you'll eventually pay taxes (except for Roth accounts, which have income limits and contribution caps).

With structured payments, the annuity's internal growth escapes taxation entirely. The insurance company invests your premium, earns returns on those investments, and pays you from principal plus earnings. You owe zero tax on any of it.

Here's a concrete example. You settle for $500,000. Take it as a lump sum, invest it reasonably well at 6% average annual returns, and withdraw $2,500 monthly. The investment earnings get taxed each year—let's say you're in the 24% federal bracket plus 5% state. Over 20 years, you'll pay roughly $140,000 in taxes on the investment earnings.

Structure that same $500,000 for $2,850 monthly for 20 years (the larger monthly amount reflects tax-free growth inside the annuity), and you pay zero taxes. None. Ever. That's $140,000 in your pocket instead of the government's.

The tax-free compounding grows more valuable over longer time periods. A 25-year-old structuring payments until age 75 benefits far more from tax-free growth than a 55-year-old structuring payments for ten years.

But restrictions apply. The tax benefits only work when your settlement compensates for physical injuries or physical sickness. If you're settling an employment discrimination case, a sexual harassment claim that didn't involve physical touching, or a defamation lawsuit, structuring provides no tax advantages. The payments count as ordinary income.

Even in physical injury cases, punitive damages don't qualify. Compensatory damages for your medical bills, pain and suffering, and lost wages? Tax-free. Punitive damages awarded to punish the defendant? Fully taxable as ordinary income, and structuring them doesn't help.

The qualified assignment structure I mentioned earlier is mandatory for preserving these tax benefits. If you try to control the annuity directly, or retain any right to modify the payments, the IRS treats it as a taxable installment sale and you lose the tax-free treatment. The assignment company must own the annuity. You're just the payee.

The Periodic Payment Settlement Act of 1982 established the federal legal framework for these arrangements, and every state has since adopted conforming legislation. These laws clarify the tax treatment, establish standards for assignment companies, and create consumer protections.

State regulations vary. California requires specific disclosures and mandates that claimants receive information about their right to reject structured settlements. Florida requires assignment companies to be licensed. New York has strict solvency requirements for annuity issuers. Your attorney should know your state's specific rules.

One more critical point: don't confuse structured settlements with installment payments from the defendant. If the defendant just agrees to pay you $5,000 monthly for ten years without purchasing an annuity or using qualified assignment, you've got a very different deal. That arrangement offers no tax advantages, and if the defendant goes bankrupt, you're an unsecured creditor who might get nothing.

When Structured Payments Beat Lump Sum Settlements

Neither option is universally superior. The right choice depends on your specific situation. But certain circumstances strongly favor structuring.

Long-Term Medical Care and Future Expenses

Suffered a spinal cord injury that'll require $4,000 monthly in attendant care for the rest of your life? Structuring $4,000+ monthly payments ensures you can pay those caregivers without worrying whether your investment portfolio survived the latest market crash.

Brain injuries, amputations, severe burns, and other catastrophic injuries typically involve decades of ongoing medical costs. Medications, equipment replacement, therapy, periodic surgeries—the bills never stop. Matching your payment schedule to these expenses removes the burden of managing investments and the risk of outliving your money.

Future surgeries present another opportunity for smart structuring. If your orthopedic surgeon says you'll need a knee replacement in approximately seven years and another in fifteen years, build $80,000 lump sum payments into your structure for years seven and fifteen. The money appears exactly when you need it.

Younger plaintiffs face the longest time horizons. A 22-year-old settling a case might need income for 60+ years. Even disciplined investors with professional help struggle to make a lump sum last six decades. Structured payments guarantee income regardless of how long you live, what happens in financial markets, or whether you make smart decisions in your 30s and 40s.

Protection from Poor Financial Management

Most Americans live paycheck to paycheck and carry credit card debt. They've never managed more than a few thousand dollars at once. Suddenly receiving $300,000 or $800,000 overwhelms them.

Research on lottery winners tells a consistent story: within five years, most have spent everything and often end up in worse financial shape than before they won. Injury settlement recipients follow similar patterns. The new car becomes three new cars. The modest house becomes a mansion with a massive mortgage. "Friends" appear with investment opportunities. Family members need loans that never get repaid.

Structured settlements remove the temptation because the money literally isn't available. You can't blow through $500,000 on stupid purchases if you're only receiving $2,000 monthly. This forced discipline protects you from your own worst impulses and from the people around you who suddenly want a piece of your settlement.

The protection extends to predators. Con artists target injury victims—it's public record when substantial settlements occur. They pitch land deals, business ventures, investment schemes, all designed to separate you from your money. Can't pitch what you can't access. Your money's locked up in an annuity owned by an assignment company that won't return the investment advisor's calls.

In 23 years of practice, I've watched the aftermath of both approaches. Clients who structured their settlements almost always maintain financial stability 10, 15, 20 years later. They're still covering medical expenses, still housed, still solvent. Clients who took lump sums? Maybe one in ten still has any of that money after a decade, even when they hired me immediately to help manage it. The psychological impact of guaranteed monthly income versus watching an account balance decline is profound. When you receive monthly payments, it feels like a paycheck you can budget around. When you're drawing down a lump sum, every withdrawal feels like you're getting poorer, which creates anxiety that leads to either hoarding the money until an emergency forces you to spend it all at once, or panic-spending it early. For anyone without substantial prior experience managing investments—which describes 95% of injury victims—structured payments deliver security that no financial advisor can replicate

— Jennifer Martinez

Structured settlements also offer psychological benefits beyond financial protection. You don't need to monitor stock markets, rebalance portfolios, or worry about another 2008-style crash. The insurance company bears all investment risk. Your payments arrive like clockwork regardless of what's happening on Wall Street.

Common Mistakes People Make When Choosing Settlement Payment Structures

Even with good legal advice, injury victims regularly make expensive errors in this decision. Understanding these pitfalls helps you avoid them.

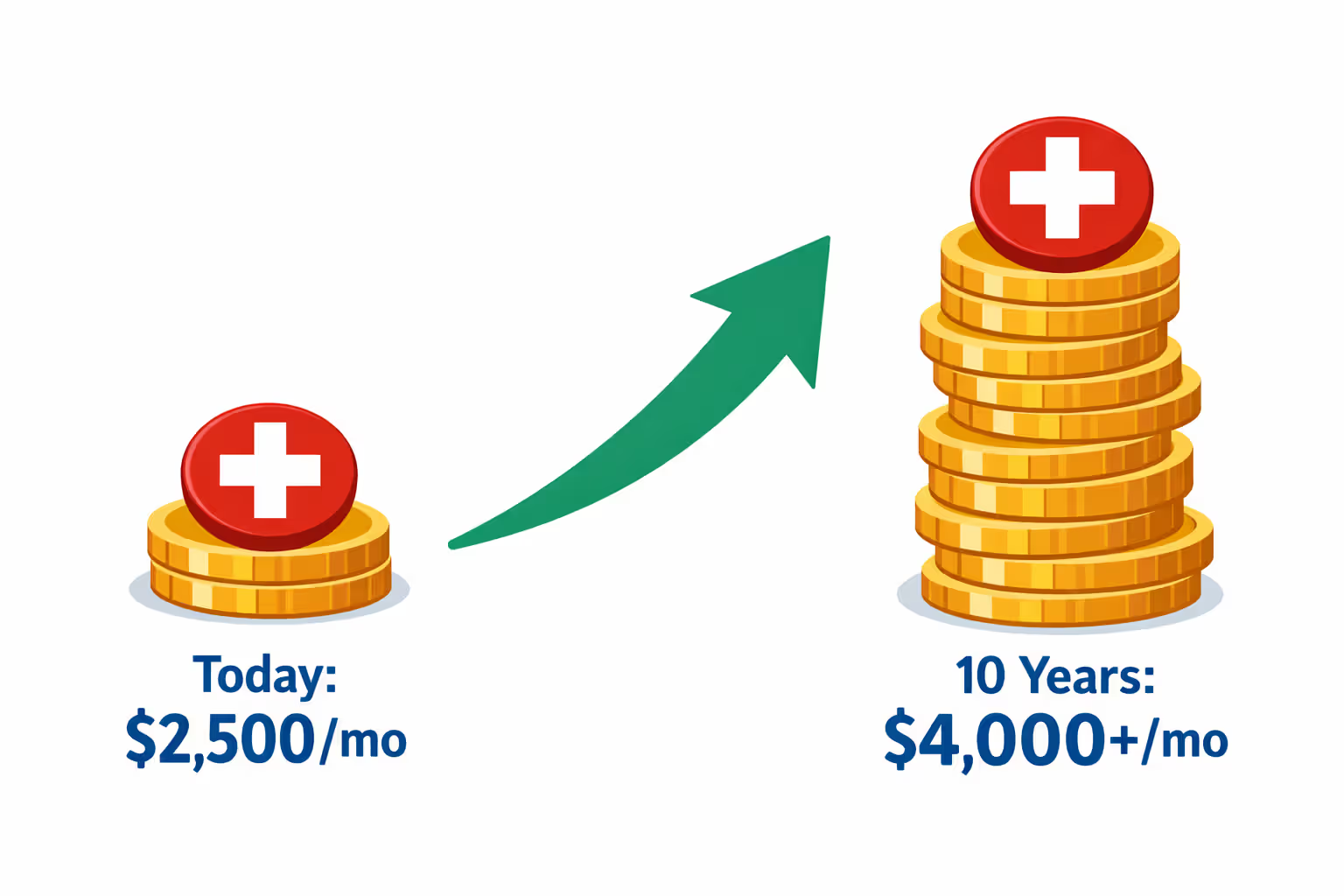

Underestimating future costs tops the list. Your medical expenses today are $2,500 monthly. You structure payments at $2,600 monthly, figuring that gives you a small cushion. Sounds reasonable.

Except healthcare inflation runs 5-7% annually—double the general inflation rate. In ten years, those expenses that cost $2,500 today will cost $4,000+. Your $2,600 monthly payment hasn't changed. Now you're $1,400 short every month with no way to fix it.

Better approach: structure increasing payments that rise 3-4% annually, or build in periodic lump sums every few years that you can use for rising medical costs. You might also structure only your baseline needs and keep some settlement funds accessible for the inevitable cost increases.

Ignoring liquidity needs creates different problems. You structure 100% of your $400,000 settlement into monthly payments because the guaranteed income sounds great. Six months later, your roof needs $15,000 in repairs. Your car dies and you need $8,000 for a replacement. Your daughter needs braces at $5,000. None of this is covered by your monthly payment stream.

You have two bad options: drain your credit cards at 22% interest, or sell some of your structured payments at a massive discount (we'll cover this later). Either way, you're losing money you didn't need to lose.

Financial planners typically recommend keeping 10-25% of your settlement as an accessible lump sum—call it an emergency fund or liquidity reserve. Structure the rest for long-term income. This gives you the security of guaranteed payments plus the flexibility to handle unexpected expenses.

Accepting unfavorable terms happens when you don't shop the deal or lack negotiating leverage. Not every annuity carrier offers identical rates. One might quote $2,600 monthly for your $500,000 premium while another quotes $2,850 monthly for the same premium. That's $9,000 annually—$180,000 over 20 years—just by choosing the better carrier.

Your attorney should obtain quotes from multiple carriers and push for the best terms. The difference between a strong quote and a weak one often exceeds 8-10% in total lifetime payments. That's tens of thousands of dollars.

Failing to consider existing resources also causes issues. If you're 55 years old with $800,000 in retirement accounts, a paid-off house, and a pension starting at 62, you probably don't need to structure your entire $300,000 settlement for lifetime income. You've already got retirement covered. Maybe take the lump sum to pay off debts and fund some bucket-list goals while you're healthy enough to enjoy them.

Conversely, if you're 35 with no savings, no retirement plan, and a family depending on you, structuring most of your settlement makes sense because you have nothing else to fall back on.

Some people structure payments beyond realistic life expectancy without properly designating beneficiaries. You're 68 years old and structure payments for 30 years. Statistically, you'll die before the payments end. What happens to the remaining payments?

If you've designated beneficiaries, they receive the remaining payments on the same schedule, maintaining tax-free status. If you haven't designated beneficiaries, remaining payments go to your estate. That means probate, estate taxes potentially, and creditors can reach the money before your heirs see a dime. A simple beneficiary designation avoids all this.

Tax planning mistakes happen even though settlement proceeds are tax-free. If your settlement includes both compensatory damages (tax-free) and punitive damages (taxable), you should generally take the punitive portion as a lump sum. Structuring punitive damages provides zero tax benefit while locking up money you could invest for better returns.

Author: Andrew Halvorsen;

Source: avayabcm.com

Can You Change or Sell Your Structured Settlement Payments?

The simple answer: no, you cannot change your structured settlement. Period.

The payment schedule is contractually fixed when you finalize the settlement. You can't call the insurance company and say "I'd like to skip the next six months of payments and take a larger amount next year instead." You can't accelerate payments. You can't defer them. You can't increase or decrease them. The rigidity is baked into the legal structure that creates the tax benefits.

But you can sell your payment rights. Several companies—called factoring companies or structured settlement purchasers—will buy some or all of your future payments for an immediate lump sum.

Here's how it works. You're receiving $3,000 monthly for the next 15 years, which totals $540,000 in future payments. You need $60,000 immediately for a business opportunity. A factoring company offers to buy the next 30 months of your payments ($90,000 face value) for $60,000 cash today.

That's a 33% discount, meaning you're giving up $90,000 in future payments to receive $60,000 now. The factoring company gets a 50% gross profit ($90,000 received vs. $60,000 paid), minus their cost of capital and administrative expenses.

These transactions require court approval under the Structured Settlement Protection Act and similar state laws enacted in all 50 states. You must petition the court for permission to transfer payment rights. The factoring company must provide extensive disclosures about the discount rate, what you're giving up, and how the transaction affects your financial situation.

Courts scrutinize these deals because factoring companies historically exploited financially unsophisticated claimants, offering absurdly low amounts for valuable payment streams. Judges must find that the transfer serves your best interest and doesn't result from fraud, duress, or undue influence.

Expect the court to ask: - Why do you need the money? - Have you explored alternatives like loans or payment plans? - Do you understand what you're giving up? - Have you sold payments before? - Is the discount rate reasonable?

Judges frequently deny petitions when the stated need seems frivolous ("I want to buy a boat"), the discount exceeds 20-25%, or the claimant has already sold payments multiple times, suggesting financial mismanagement.

The effective discount rate typically runs 10-18% annually, far exceeding what you'd pay for most other forms of credit. A $60,000 personal loan at 8% interest costs much less than selling $90,000 in structured payments.

Selling makes sense in limited circumstances:

- Avoiding foreclosure on your primary residence

- Starting a business with strong prospects and a solid plan

- Paying for education that credibly increases your earning capacity

- Covering major medical expenses not anticipated when you structured the settlement

- Preventing bankruptcy from overwhelming debt

Selling rarely makes sense for vacations, luxury purchases, helping relatives who should handle their own finances, or paying off credit cards you'll just run up again.

Partial sales offer middle ground. Instead of selling all future payments, you sell a defined portion—perhaps the next three years of payments, or every other payment for six years. You get immediate cash while retaining significant future income.

Some states heavily restrict these transactions. New Jersey essentially prohibits them. Minnesota requires independent professional advice from an attorney or financial advisor not paid by the factoring company. Washington caps discount rates at specific levels.

Before selling, exhaust alternatives:

- Personal loans from banks or credit unions (usually 6-12% APR)

- Home equity lines of credit (often 7-10% APR if you own a home)

- Payment plans with creditors (medical providers often accept $200/month for years)

- Assistance from family (probably cheaper than a 15% effective discount rate)

- Credit counseling and debt management plans

The factoring company is not your friend. They profit by paying you significantly less than your payments are worth. Everything in their sales pitch emphasizes the benefits of immediate cash while minimizing the cost. Read the disclosures carefully. Calculate the actual discount rate. Compare it to other borrowing costs.

And remember: once the court approves the transfer and you receive the money, those payments are gone forever. If you sell ten years of payments and then discover you desperately need guaranteed income in year eight, too bad. You already sold it.

Frequently Asked Questions About Personal Injury Structured Settlements

No universal right answer exists. Structured settlements work brilliantly for some people and terribly for others. Your decision should reflect your specific circumstances, not generic advice or what worked for someone else.

Start by honestly assessing your financial discipline. Have you successfully managed money in the past, or do you struggle to stick to budgets? Do you have family members or advisors you trust to help, or will you be navigating this alone? Can you resist pressure from relatives who want loans, salespeople pitching investments, and your own impulses to spend?

If you're uncertain about any of those questions, structured payments provide valuable guardrails.

Consider your age and life expectancy. A 28-year-old needs to make money last potentially 60+ years. A 62-year-old might only need 25 years of income. Younger claimants benefit more from guaranteed lifetime income and tax-free compounding over longer periods.

Examine your injury severity and future medical needs. Catastrophic injuries requiring lifelong care strongly favor structured payments matched to anticipated expenses. Minor injuries that healed completely might not require the same long-term planning.

Look at your existing resources. Do you have retirement savings, home equity, other assets, or family wealth to fall back on? If so, you might not need to structure your entire settlement. If this settlement represents your only financial asset, protecting it through structured payments becomes more important.

Think about liquidity realistically. Will you need access to substantial cash in the near future for business opportunities, education, housing, or other major expenses? If so, structure less and keep more accessible. If you can't identify any likely major expenses beyond what your monthly payments will cover, structure more.

Talk to multiple professionals before deciding. Your attorney understands the legal aspects but might not grasp investment implications. A fee-only financial planner (not one paid commissions by insurance companies) can model different scenarios and show you the financial outcomes. A structured settlement consultant specializes in these decisions and can obtain quotes from multiple carriers.

Remember that hybrid approaches often work best. Maybe structure 60% for guaranteed income and take 40% as a lump sum for flexibility. Or structure 75% and keep 25% accessible. There's no requirement to choose 100% of one approach or the other.

Model different scenarios. What happens if you take everything as a lump sum and invest it conservatively? What happens if you structure everything? What happens with a 70/30 split? Run the numbers with realistic assumptions about investment returns, spending patterns, inflation, and life expectancy.

Give yourself time to make this decision. Don't let attorneys or insurance companies pressure you into choosing quickly. This affects your financial life for decades. A few extra days or weeks spent analyzing your options is time well spent.

And understand that while structured settlements offer valuable benefits—guaranteed income, tax-free growth, protection from mismanagement—they're not magic. They won't solve financial problems caused by overspending or poor decisions in other areas of your life. They're a tool, not a cure-all.

The choice you make today ripples through the rest of your life. Choose the structure that genuinely matches your needs, circumstances, and capabilities—not the one that sounds best in theory or that worked for someone else. Your situation is unique. Your settlement structure should be too.