Insurance company envelope with legal documents, calculator, and pen on wooden desk next to framed photo of elderly woman

Structured Settlement Beneficiary Rights Guide for Heirs and Designees

Content

Your aunt passed away last month. At the funeral, her attorney mentioned you're designated to receive her structured settlement payments—$1,800 every month for the next twelve years. But where's the money? Who actually sends it? Can creditors take it?

Here's what catches people off guard: inheriting structured settlement funds works nothing like getting a house or a savings account. The payments come from an insurance company, not an estate. They follow rules set years ago when your aunt negotiated her personal injury case. And they're protected by laws most inheritance attorneys have never studied.

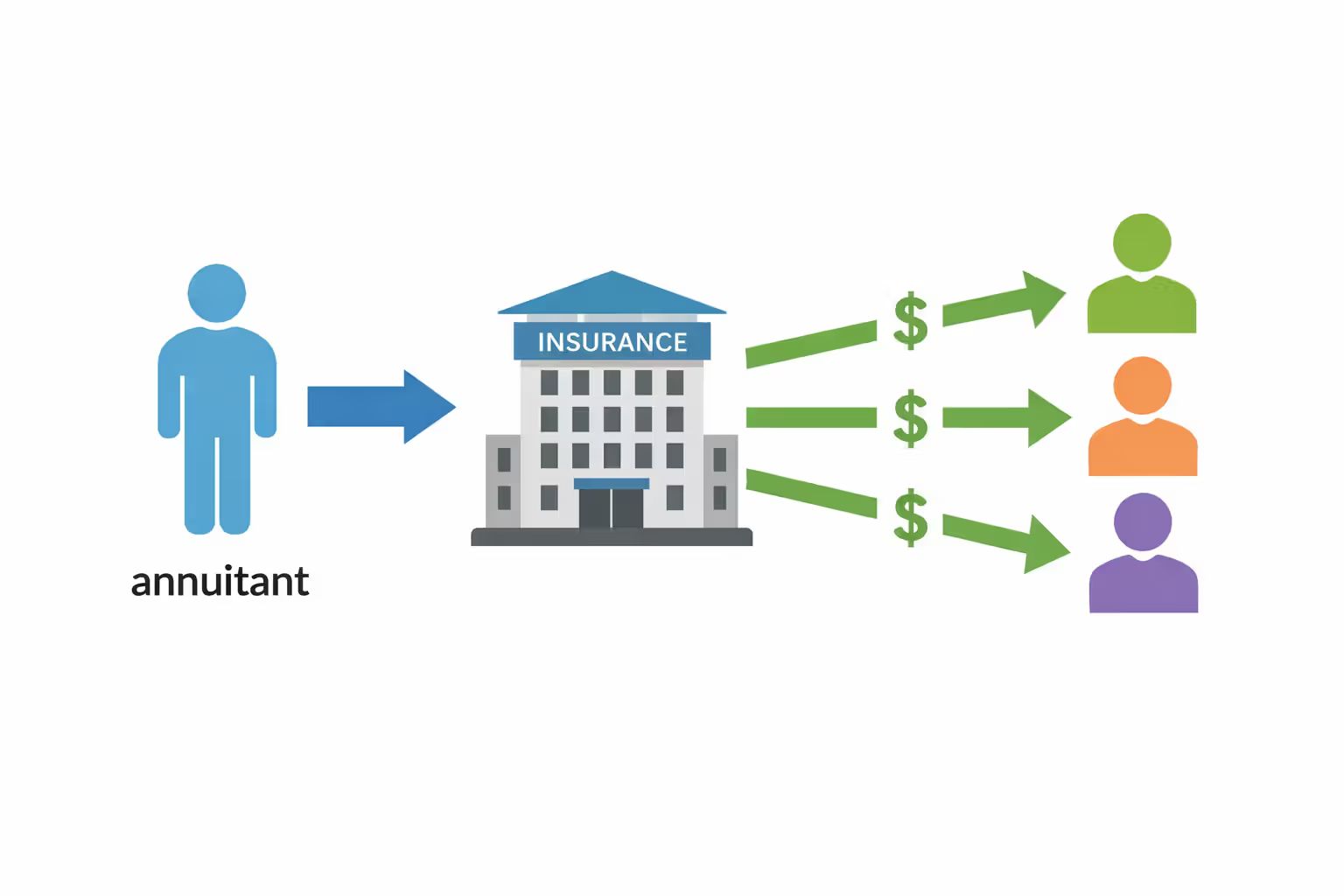

Structured settlements spring from legal cases—someone got hurt at work, injured in a car accident, or died due to negligence. Rather than cutting one giant check, the defendant's insurance company sets up an annuity that pays the victim gradually. When that victim (called the annuitant in legal speak) dies with payments still coming, beneficiaries step into specific rights. But "specific" means restricted, protected, and complicated.

You'll need to understand exactly what you're entitled to receive, the roadblocks you might hit when claiming it, and why companies will start calling you within days offering to "buy out" your inheritance.

Who Qualifies as a Structured Settlement Beneficiary?

Your name appearing in someone's will doesn't automatically qualify you for their settlement money. The annuity contract—signed years earlier when the lawsuit settled—controls everything.

Primary vs. contingent beneficiaries

Think of beneficiary designation like airplane boarding: primary beneficiaries board first. When the annuitant dies, these people get the remaining payments. Period.

Most people name their spouse or kids as primaries during settlement negotiations. Sometimes it's parents or siblings. The annuitant picks one person or splits the payments among several—maybe three kids each get one-third. That designation happened years ago when the plaintiff's lawyer, settlement consultant, and insurance company finalized the deal.

Author: Christopher Vaughn;

Source: avayabcm.com

Contingent beneficiaries sit in the backup row. They board only if every primary beneficiary is dead or missing. Your sister names you as primary and her best friend as contingent? You get the money. But if you die before your sister does, the friend receives it instead—unless the contract uses per stirpes distribution.

Per stirpes means "by branch" in Latin. It's crucial when families span generations. Say your dad named you as primary beneficiary but you died before he did. Without per stirpes, the money goes to contingent beneficiaries. With per stirpes, your kids step into your shoes and inherit what you would've gotten. I've seen families lose six-figure inheritances because nobody understood this distinction.

Factored vs. non-factored settlement distinctions

Here's where things get messy. Some annuitants sell their payment rights before dying—a process called factoring. Your uncle might've been getting $2,000 monthly, but last year he sold the next 60 payments to J.G. Wentworth for $80,000 cash.

Guess what that means for you as his beneficiary? Those 60 payments are gone. The factoring company owns them now. You'll only receive whatever payments he didn't sell.

Non-factored settlements stay with the original insurance company. Everything works as planned. You notify the insurer, prove you're the designated beneficiary, and the money starts flowing to you instead of the deceased annuitant.

Before celebrating your inheritance, check the courthouse. Factoring transactions require court approval in 48 states, creating public records. Search for your benefactor's name in their county's civil court database. Look for "petition for transfer of structured settlement payment rights." Each approved petition shows exactly which payments got sold and which remain.

The designation itself isn't something you can retroactively join. When the plaintiff finalized their settlement—maybe in 2015, maybe in 2003—the beneficiaries got locked in. You're either on that contract or you're not.

Legal Protections for Settlement Annuity Beneficiaries Under Federal and State Law

Beneficiaries don't just inherit money—they inherit a fortress of legal protections most people never realize exists.

Anti-assignment rules prevent anyone (including you) from freely signing away payment rights. The annuitant couldn't just hand their payments to a creditor or family member without court involvement. Once you inherit those rights? Same restrictions apply. You're actually protected from your own impulsive decisions, especially during the grief-soaked weeks after someone dies.

Let's talk creditors, because this trips people up. Say your father owed $75,000 when he died—credit cards, medical bills, the works. His creditors cannot intercept your structured settlement inheritance to satisfy his debts. The payments pass to you clean.

However—and this matters—your own creditors might reach the money once it hits your bank account. The distinction: protected from the deceased person's financial problems, but not necessarily from yours.

State exemption laws determine your personal protection level. Texas treats structured settlement payments like untouchable assets. Florida too. New Hampshire? Not so much. Creditors can garnish the payments in some states the same way they'd garnish wages. The settlement bypasses your father's creditors but might not escape yours.

Here's what beneficiaries discover too late: they've inherited something more valuable than ordinary money—a legally protected asset that survives death. But I watch heirs throw away those protections monthly. They deposit settlement checks into their regular checking account alongside grocery money. They sign paperwork from aggressive buyers without reading. One client lost $180,000 in protections because he didn't understand he'd inherited a specialized financial instrument, not just 'some insurance payments

— Rebecca Thornton

Tax implications depend entirely on what generated the original settlement. Physical injury cases—broken bones, brain damage, burns—qualified for tax-free treatment under Section 104(a)(2) of the Internal Revenue Code. When you inherit those payments, they stay tax-free.

Non-physical claims tell a different story. Employment discrimination settlements? Taxable. Emotional distress without physical symptoms? Taxable. Punitive damages? Usually taxable. If the original annuitant paid taxes on their payments, you'll pay taxes too.

Watch out for interest accrued between death and payment receipt. Even if the underlying settlement was tax-free, any interest earned during the transition period counts as taxable income. It's usually small—maybe $200 to $800—but it still needs reporting.

State-specific variations create headaches for people inheriting settlements across state lines. California's Structured Settlement Protection Act includes beneficiary provisions that differ wildly from New York's rules. Some states demand court approval for any transfer of beneficiary rights, regardless of dollar amount. Others allow transfers under $10,000 without judicial oversight.

Which state's law controls? Generally the state where you live—not where the annuitant lived or where the original case settled. If your aunt's settlement was finalized in Illinois, she lived in Ohio, and you live in Georgia, Georgia's laws govern your beneficiary rights.

How Beneficiary Payments Work After the Annuitant's Death

The contract signed years ago determines everything about how you'll actually receive money.

Lump sum vs. continued periodic payments

Most settlements include a "guaranteed period certain"—insurance-speak for "we'll keep paying for X years no matter what happens." Your uncle's settlement guaranteed 20 years of payments. He died in year 9. You're entitled to the remaining 11 years.

Payments continue on the same schedule: monthly stays monthly, quarterly stays quarterly. If he got $2,500 on the first of every month, you'll receive $2,500 on the first of every month. The amount doesn't shrink based on beneficiary count—it gets divided. Three beneficiaries sharing that $2,500? You each get $833.33.

Some older contracts have "life only" provisions. Payments stop the moment the annuitant dies. No guaranteed period, no beneficiary payments, nothing. These structures are rare now but still exist, particularly in settlements from the 1990s when injured plaintiffs wanted maximum monthly payments and agreed to eliminate survivor benefits.

How do you know which you've inherited? Read the annuity contract. Page 3 or 4 usually spells it out: "Guaranteed Period: 240 months" or "Life Only - No Guaranteed Period." Can't find the contract? Call the insurance company directly (not a broker—the actual annuity issuer listed in settlement paperwork).

Author: Christopher Vaughn;

Source: avayabcm.com

Commutation clauses and payout options

Commutation means converting all those future monthly payments into one check right now. Not every contract allows it—the option must've been negotiated into the original agreement.

If you've got commutation rights, here's how it works: The insurance company calculates what all your future payments are worth today. They use a discount rate specified in your contract—usually 4% to 7%. Higher discount rates mean smaller lump sums because the insurer's essentially saying "we could invest this money and earn 6% annually, so we're deducting that growth when paying you early."

Real numbers? You're owed $1,500 monthly for 15 years. That's $270,000 total. The commuted lump sum at a 5% discount rate might be $195,000. At 7%? Maybe $175,000. You're sacrificing $75,000 to $95,000 for immediate access.

| What You're Getting | Here's What Happens | What the IRS Does | The Upside | The Downside |

| Keep receiving monthly checks | Money keeps arriving on schedule until the guaranteed years run out | No taxes if the original injury case qualified under IRS code 104(a)(2) | You know exactly when money's coming; impossible to blow it all in one weekend; you'll receive every dollar owed over time | Can't access big chunks for emergencies; inflation erodes buying power—that $2,000 buys less in 2035 than today; you're locked in long-term |

| Convert everything to one payment now | Insurance company does math on what future payments are worth today, then cuts you one check for that discounted amount | Principal stays tax-free; any interest from the calculation period might be taxable | Money hits your account immediately; you can pay off your mortgage or start a business; no more dealing with the insurance company | You'll receive maybe 70-80% of the total value; creditor protections often disappear once it's in your bank; people frequently mismanage windfall cash |

| Payments locked in for specific years regardless of death | The insurance company promised to pay for—say—20 years, so they will, even if the annuitant died in year 4 | Tax-free if it was a qualified physical injury settlement | Beneficiaries have certainty about the inheritance; no gambling on life expectancy | Once those guaranteed years end, payments stop forever even if the annuitant died young |

| Lifetime payments with a guaranteed minimum period | Payments continue either for the annuitant's entire life OR the guaranteed period, whichever lasts longer | Tax-free under the same rules | Protects against both dying young (guaranteed period) and living decades (lifetime coverage) | Claims adjusters sometimes miscalculate; disputes emerge about what "life expectancy" meant in the contract |

Claiming benefits normally takes 6 to 12 weeks from your first phone call to receiving money. The insurance company needs proof: certified death certificate, your driver's license, documentation showing you're the named beneficiary. They verify everything, process paperwork, and set up your first payment.

Some insurers keep auto-deposits running if the annuitant was already using direct deposit—they just switch the account. Others freeze everything until beneficiary verification completes. Ask specifically about their procedure during your first conversation.

Common Mistakes Beneficiaries Make When Claiming Settlement Payments

You can permanently damage your inheritance value through mistakes that seem minor at the time.

Missing notification deadlines won't erase your rights, but it stops the money flow. Most annuity contracts give beneficiaries "reasonable time" to notify the insurer—courts usually interpret this as 30-90 days. Wait six months? You'll still get the payments eventually, but nothing arrives during that delay. Worse, most states don't require insurers to pay interest on delayed payments caused by beneficiary inaction.

Tax misunderstandings drive terrible financial decisions. A woman in Ohio inherited $440,000 in structured payments from her husband's workers' comp settlement. She assumed all inherited money is taxable and sold the entire stream to a factoring company at a 45% discount to "avoid the tax bill." Workers' comp settlements are tax-free. By assuming otherwise, she threw away $198,000.

Predatory buyers circle obituaries like vultures. Your mother dies on Tuesday. By Friday, you've received three phone calls and two letters from companies offering to "expedite your inheritance" or "help with the complicated paperwork." They're not helping—they're buying your payment rights for 40-60 cents on the dollar.

Real factoring companies disclose the discount rate transparently and follow state court approval requirements. Scammers claim they're "processing your payments faster" or "handling administrative requirements." They pressure you to sign documents immediately, before you understand you're selling $300,000 in future payments for $120,000 cash.

Neglecting to update beneficiary designations creates multi-generational disasters. You inherit structured payments from your father. You want your daughter to get them after you die. Mentioning it in your will isn't enough—the annuity contract's beneficiary designation controls regardless of what any will says. You must submit written beneficiary changes to the insurance company.

Mixing settlement money with regular bank accounts destroys creditor protections in many states. When settlement payments hit your checking account alongside your paycheck, car payment, and grocery spending, courts often rule you've "commingled" the protected funds with general assets. Keep settlement money in a separate account clearly labeled "Structured Settlement Inheritance" or similar.

Author: Christopher Vaughn;

Source: avayabcm.com

Can Beneficiaries Sell or Transfer Their Settlement Payment Rights?

Yes, but lawmakers built a legal obstacle course to slow you down—for your own protection.

Forty-eight states enacted Structured Settlement Protection Acts requiring court approval before anyone can purchase your payment rights. These laws emerged in the late 1990s when injured people were signing away $500,000 in payments for $125,000 in cash, not understanding the terrible deal they'd accepted.

The court approval process forces you to petition a judge, typically in your home county. You'll explain why you need to sell, what you're receiving compared to the payments' full value, and whether you've explored alternatives. Judges evaluate:

- The effective discount rate (how much you're losing)

- Whether you truly need the money or just want it

- If you understand the transaction completely

- Whether the buyer provided clear written disclosures

- Whether state law requirements were followed

Judges reject roughly 15-25% of transfer petitions nationwide. Common rejection reasons: discount rates above 18% annually, evidence the seller doesn't understand what they're signing, insufficient disclosure from the buyer, or clear better alternatives (like a bank loan).

Some states impose tougher scrutiny on beneficiary transfers specifically. Florida courts apply stricter standards when beneficiaries—rather than original annuitants—want to sell. The logic: beneficiaries didn't choose this structured payout and might be especially vulnerable during the grief period.

Red flags that you're dealing with a predatory operation:

- "You don't need court approval in this situation" (you do, in 48 states)

- Pressure to sign documents today or "the offer expires"

- Offering payment before the court hearing (illegal in most states)

- Refusing to provide written disclosure of the effective discount rate

- Claiming you'll receive 90-95% of your payments' value (market rates run 60-75%)

- Contacting you within days of the annuitant's death

Legitimate buyers like Peachtree Financial Solutions (now Fortitude Financial Solutions), J.G. Wentworth, and Catalina Structured Funding follow state laws, disclose pricing clearly, and maintain established court procedures. Even reputable companies pay 60-75 cents per dollar of present value—that's just market reality for this type of transaction.

Before selling anything, consult an attorney who doesn't work for the purchasing company. State bar associations maintain referral services for lawyers experienced in structured settlement transfers. The consultation costs $250-600 but protects inheritance often worth $200,000 to $500,000.

Steps to Verify and Claim Your Beneficiary Settlement Payments

Taking steps out of order causes delays that can stretch months.

Start by hunting down the annuity contract. The deceased should've received copies when their settlement finalized—check safe deposit boxes, filing cabinets, fireproof safes. Can't locate anything? Contact the attorney who represented them in the original case. Personal injury lawyers typically retain settlement files for 20-30 years specifically for situations like this.

Call the annuity issuer directly—not a broker, agent, or consultant. The contract names the insurance company: Pacific Life, MetLife, Prudential, New York Life, and others. Find their structured settlement department (general customer service can't help you) and report the death.

Assemble documentation before that first call:

- Certified death certificate—order 8-10 copies since multiple organizations demand originals

- Your driver's license or passport

- The annuity contract showing your beneficiary designation

- Your Social Security number for tax form preparation

- Bank account and routing numbers for direct deposit

Some insurers handle beneficiary claims internally. Others use third-party administrators—Sage Settlement Consulting, Structured Settlement Consultants, Strategic Capital. The administrator assigns you a claim number and case manager. Write down names, dates, and details from every conversation. Trust me on this—memories fade and details matter when questions arise months later.

Processing usually spans 45-90 days broken into stages:

- Days 1-14: You submit documents and the company opens your claim

- Days 15-30: They verify the death certificate and confirm your beneficiary status

- Days 31-45: Internal approvals and processing

- Days 46-65: Payment system setup and first disbursement

Delays stretch beyond 90 days when paperwork is incomplete, when multiple beneficiaries need verification, or when the annuitant's estate is stuck in probate court. If three months pass without explanation, attorney consultation time arrives. Several states penalize insurers who unreasonably delay valid beneficiary payments.

Request written confirmation of your payment schedule: exact amounts, specific dates, total duration. This prevents disputes later. Also ask about cost-of-living adjustments or future lump sums built into the contract—these details hide in the fine print.

Verify calculations independently. Guaranteed period was 25 years, annuitant died in year 11? You should receive 14 years of payments. Insurance companies occasionally miscalculate, especially with multiple beneficiaries or complex payment structures involving annual increases.

FAQ: Structured Settlement Beneficiary Rights

Your structured settlement inheritance carries protections that regular inherited assets don't enjoy—but only if you actually understand and invoke them properly.

These aren't typical inherited dollars. They come wrapped in statutory protections from creditors, predatory buyers, and tax collectors that ordinary inheritance doesn't receive. But protection requires action.

Most important move: educate yourself before making irreversible decisions. Don't sell payments during the emotional chaos following the annuitant's death. Don't sign anything from buyers who cold-call you. Don't assume you understand tax implications without consulting a CPA who specializes in structured settlement taxation.

Document everything obsessively. Keep copies of every letter from the insurance company, records of every payment deposited, proof of your beneficiary designation. This documentation shields you when disputes emerge and creates clear records for your own estate planning later.

Think about how these payments fit your broader financial life. Structured settlements deliver guaranteed income streams that can fund retirement, pay for education, or provide security during economic downturns. These advantages often outweigh the temptation of immediate lump sum access, particularly considering the 25-40% discounts involved in selling payments.

Feeling uncertain or pressured? Contact your state bar association for referrals to attorneys experienced in structured settlement beneficiary issues. Spending $400-1,000 on legal consultation protects inheritances frequently worth $250,000 to $600,000.

Your beneficiary rights exist to protect you and guarantee you receive what the annuitant intended you to have. Understanding these rights transforms you from a confused heir into an informed beneficiary who maximizes this unique inheritance's value.