Dollar bills decreasing in size along a timeline stretching from 10 to 40 years, symbolizing the erosion of purchasing power in a structured settlement over decades

Structured Settlement Long Term Value Explained

Content

When you accept a structured settlement after a personal injury case, you're not just signing up for monthly checks—you're locking in a financial instrument that will either preserve or erode your purchasing power over decades. A 35-year-old plaintiff receiving $3,000 monthly for life faces a completely different economic reality at age 75 than the nominal payment amount suggests.

Most settlement recipients focus on the advertised total: "You'll receive $1.8 million over 30 years!" But that figure ignores inflation, opportunity cost, and the actual spending power those dollars will command when you're 65 instead of 35. Understanding structured settlement long term value requires looking past marketing materials and examining what your payment stream will actually accomplish across multiple decades of your life.

The difference between a well-structured settlement and a poorly planned one can mean the gap between financial security and struggling to cover basic expenses in your later years. This guide breaks down exactly how to evaluate, calculate, and maximize the real value your settlement will deliver over 20, 30, or 40+ years.

How Structured Settlement Payments Accumulate Value Over Decades

A structured settlement converts a lump-sum settlement into a series of guaranteed payments funded by an annuity purchased from a highly-rated life insurance company. Unlike investment accounts that fluctuate, your payment schedule is locked in at the time of settlement—both the amount and timing are contractually guaranteed.

The "value accumulation" happens differently than with traditional investments. You're not earning returns on a growing principal balance. Instead, the insurance company invests your lump sum and uses actuarial calculations to determine payment amounts that exhaust the principal plus earnings over your expected lifetime (or specified period).

For example, a $500,000 lump sum might be structured to pay $2,500 monthly for 25 years—a total nominal payout of $750,000. That extra $250,000 represents the insurance company's guaranteed return, typically based on bond yields and conservative investment returns at the time of settlement. If interest rates are 4% when your settlement is structured, that's roughly the embedded return you're receiving, though you never see it itemized that way.

Author: Olivia Carmichael;

Source: avayabcm.com

The present value concept matters here: $2,500 received in year 20 is worth substantially less than $2,500 today. If you discount future payments at 3% annually (a reasonable inflation estimate), a payment 20 years out has roughly 55% of today's purchasing power. This is why the total nominal payout can look impressive while the actual economic value delivered may be far less.

Payment schedules vary enormously. Some settlements front-load larger payments for immediate medical needs, then drop to lower amounts. Others increase payments over time. A 30-year settlement might include a $50,000 payment every five years for major medical equipment replacement, monthly payments for living expenses, and a final lump sum at age 65 to supplement retirement. Each design choice affects long-term value differently.

The guaranteed nature provides value beyond simple dollars. You cannot outlive a lifetime payment structure, cannot lose principal to market crashes, and cannot make poor investment decisions that deplete the funds. For someone with a severe injury and uncertain investment experience, this certainty carries real economic value that's difficult to quantify but shouldn't be ignored.

7 Factors That Determine Your Settlement Annuity's Lifetime Value

Interest rate environment at settlement time: The prevailing interest rates when your annuity is purchased determine how much "growth" is built into your payment stream. A settlement structured in 2008 when rates were higher delivers more total payout from the same lump sum than one structured in 2020 during historic low rates. You have no control over this timing, but it significantly impacts lifetime value.

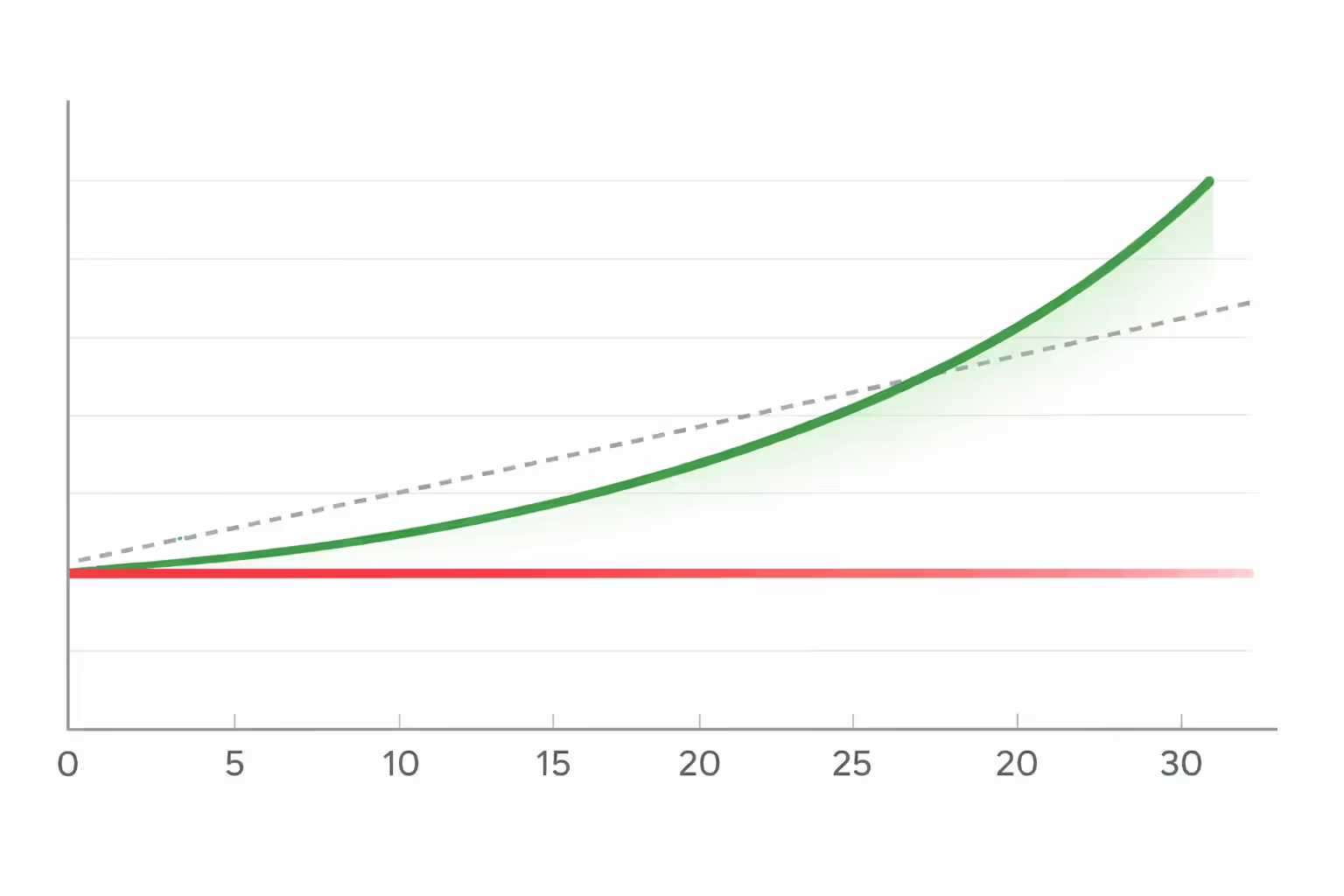

Inflation impact: This is the silent killer of long-term settlement value. At 2.5% annual inflation (the long-term US average), purchasing power cuts in half every 28 years. Your $3,000 monthly payment will buy roughly $1,500 worth of today's goods in 28 years. Over a 40-year settlement, inflation compounds brutally—that same payment has only 37% of its original purchasing power at year 40.

Payment frequency and timing: Monthly payments provide regular income but no opportunity to invest lump sums for potentially higher returns. Annual or semi-annual payments give you larger amounts to potentially invest elsewhere, though this introduces market risk. Front-loaded structures give you more dollars when they're worth more (today), while back-loaded structures pay more later when dollars are worth less.

Cost-of-living adjustments (COLAs): This is the single most important feature for preserving settlement annuity lifetime value, yet many plaintiffs skip it because it reduces initial payment amounts.

Author: Olivia Carmichael;

Source: avayabcm.com

Insurance company ratings: Your settlement is only as secure as the insurance company backing it. A highly-rated company (A+ or better from multiple rating agencies) provides confidence that payments will continue for decades. Lower-rated companies may offer slightly higher payments but introduce risk that matters enormously over 30+ years.

Tax advantages: Qualified structured settlements from physical injury cases are tax-free under IRC Section 104(a)(2). This creates substantial value compared to taxable alternatives. A $3,000 monthly tax-free payment equals roughly $3,750-$4,000 monthly from a taxable source for someone in a 25% tax bracket.

Customization options: Settlements can include increasing payments, decreasing payments, lump sums at specified intervals, or lifetime payments with guaranteed minimum periods. Each choice affects total value differently depending on how long you live and when you need larger amounts.

Why Cost-of-Living Adjustments Matter for 30+ Year Settlements

A COLA rider increases your payment by a fixed percentage annually—typically 2%, 3%, or 4%. The trade-off is harsh: to fund future increases, your initial payment drops significantly. A settlement that would pay $3,000 monthly fixed might only pay $2,100 monthly with a 3% COLA.

Many plaintiffs reject COLAs because they need maximum income now. But run the numbers over 30 years:

Without COLA, you receive $3,000 monthly for 30 years = $1,080,000 nominal total. With 2.5% inflation, the real value of year 30 payments is about $1,420 in today's dollars.

With 3% COLA starting at $2,100, year 30 payments reach $5,091 monthly. The nominal total is $1,186,000, and the year 30 payment has real value of roughly $2,500 in today's dollars—still losing to inflation but far better than the fixed payment.

The crossover point where COLA payments exceed fixed payments typically occurs around year 8-12, depending on the COLA percentage. If you're under 50 and expecting to receive payments for 30+ years, skipping COLA protection is almost always a mistake from a structured settlement future value planning guide perspective.

How Insurance Company Strength Protects Long-Horizon Value

Insurance companies can fail, merge, or face financial distress over multi-decade periods. While state guaranty associations provide backup (typically covering $250,000-$500,000 depending on state), you don't want to rely on this safety net for a large settlement.

Check ratings from all major agencies: A.M. Best, Standard & Poor's, Moody's, and Fitch. Require A+ or better from at least two agencies. For settlements over $1 million, consider splitting between two highly-rated carriers to diversify risk.

The insurance company cannot change your payment terms once established—your contract is guaranteed. But if the company becomes insolvent, you may face payment delays, legal proceedings, or reduced payments beyond guaranty association limits. Over 40 years, company strength matters more than a 0.5% difference in payment amounts.

Calculating Real vs. Nominal Returns: A Settlement Annuity Long Term Evaluation Guide

Nominal value is the actual dollar amount you receive. Real value is what those dollars can buy after accounting for inflation. The gap between these figures determines whether your settlement maintains your standard of living or forces gradual lifestyle reduction.

To calculate real value, discount each future payment by the expected inflation rate. If you expect 2.5% annual inflation and will receive $3,000 in year 15, the present value (real value in today's dollars) is $3,000 ÷ (1.025^15) = $2,054.

Most plaintiffs never perform this calculation and are shocked when their settlement feels inadequate 20 years later. The nominal amount hasn't changed, but everything costs more.

The discount rate you choose for evaluation matters enormously. Use 2.5%-3% for conservative inflation estimates based on long-term US averages. Some planners use higher rates (4%-5%) to account for healthcare inflation, which typically exceeds general inflation and matters greatly for injury victims.

Here's a practical example: You're offered either a $500,000 lump sum or $2,500 monthly for 25 years (total nominal value $750,000). Which delivers more real value?

The lump sum has immediate value of $500,000. The structured payments total $750,000 nominally, but discounting each payment at 3% annually gives a present value of approximately $476,000. The lump sum appears better—but this ignores taxes, investment risk, and the possibility you'll mismanage or outlive the lump sum.

If you invest the lump sum at 6% annually but pay 25% taxes on earnings, your after-tax return is 4.5%. Starting with $500,000 and withdrawing $2,500 monthly while earning 4.5% annually, you'd deplete the funds in about 28 years. The structured settlement guarantees payments for exactly 25 years with zero market risk and zero taxes.

Comparison of $500,000 Settlement Structured Three Different Ways Over 25 Years

| Metric | Lump Sum Invested (6% return, taxable) | Fixed Structured Settlement | COLA-Adjusted Settlement (3% annual increase) |

| Year 1 annual payment | $30,000 withdrawn | $30,000 | $21,000 |

| Year 10 annual payment | $30,000 withdrawn | $30,000 | $27,450 |

| Year 25 annual payment | $30,000 withdrawn | $30,000 | $43,731 |

| Total nominal value | $750,000 | $750,000 | $855,000 |

| Inflation-adjusted value (2.5% inflation) | ~$567,000 | ~$476,000 | ~$593,000 |

| After-tax value | ~$425,000 (taxes on gains) | $750,000 (tax-free) | $855,000 (tax-free) |

| Risk of depletion | High (market losses, overspending) | None (guaranteed) | None (guaranteed) |

Assumptions: 6% annual return on lump sum investment, 25% tax rate on investment gains, 2.5% annual inflation, disciplined $30,000 annual withdrawal from lump sum. Real-world investment returns vary; market losses could significantly reduce lump sum value.

The COLA-adjusted settlement delivers the highest inflation-adjusted, after-tax value despite the lowest initial payment. The lump sum offers flexibility but introduces substantial risk and tax drag. The fixed settlement provides certainty but loses significant purchasing power over 25 years.

Common Mistakes That Erode Structured Settlement Future Value

Front-loading payments without planning: Many plaintiffs request large initial payments for immediate medical bills or debts, leaving insufficient funds for later years. A settlement that pays $100,000 in year one, then $1,500 monthly thereafter, may solve immediate problems but creates long-term income inadequacy. Better approach: structure immediate payments to cover specific known expenses, then maximize the ongoing stream.

Ignoring inflation protection: As covered earlier, skipping COLAs is the most common and costly mistake for long-term settlements. The psychological appeal of higher immediate payments blinds plaintiffs to the mathematical certainty of purchasing power erosion.

Author: Olivia Carmichael;

Source: avayabcm.com

Selling payments at steep discounts: Factoring companies buy future structured settlement payments at 8%-18% discount rates—far higher than any reasonable investment return. Selling $100,000 in future payments might net you $60,000-$75,000 today. This is occasionally necessary for emergencies, but it permanently destroys value. If you need $50,000 now, selling $100,000 in future payments to get it is a catastrophic financial decision.

Not coordinating with other income sources: Your settlement should complement Social Security disability, workers' compensation, or other benefits—not jeopardize them. Some means-tested benefits have income limits; poorly timed settlement payments can trigger benefit reductions. A qualified settlement planner can structure payments to minimize these conflicts.

Failing to consider tax implications: While qualified structured settlements are tax-free, investment returns on lump sums are taxable. Some plaintiffs take lump sums without realizing that a $500,000 settlement invested at 6% generates $30,000 in taxable income annually. In a 25% bracket, that's $7,500 in annual taxes that could have been avoided with proper structuring.

Choosing payment periods that don't match life expectancy: A 30-year-old with a lifetime injury who structures payments for only 20 years faces a financial cliff at age 50. Lifetime payments (with guaranteed minimums for heirs) are usually better for younger plaintiffs with permanent injuries. Conversely, a 65-year-old might prefer a 15-year certain period rather than lifetime payments that cease at death.

How to Project and Maximize Your Settlement's Value Over 20–40 Years

Start with your current age, life expectancy, and injury-related needs over time. A 28-year-old paralyzed plaintiff faces 50+ years of expenses; a 55-year-old with a back injury has different planning horizons. Your structured settlement value projection guide should account for predictable expense changes: children's education, home modifications, vehicle replacements, caregiver costs as you age.

Use online present value calculators to discount future payments. Input your payment schedule, choose a discount rate (2.5%-3% for inflation, or higher if you want to compare against investment alternatives), and calculate the present value of your entire payment stream. This gives you the "real" value in today's dollars.

Project major expenses at future dates and ensure your settlement includes lump sums to cover them. Wheelchairs need replacement every 5-7 years at $30,000-$50,000. Vans with modifications cost $60,000-$80,000 and last 8-10 years. Structure specific lump sums for these known expenses rather than trying to save monthly payments.

Balance immediate needs against future security. You need enough income now to maintain stability, but not so much that you shortchange your later years. A common rule: structure at least 60%-70% of your settlement for long-term payments if you're under 45 and have a permanent injury.

Work with a qualified structured settlement consultant (not just the defendant's annuity broker). These professionals can model multiple scenarios showing total payout, present value, and purchasing power under different structures. Good consultants charge plaintiffs nothing—they're compensated by the insurance company—but work for your interests.

Consider hybrid structures combining guaranteed payments with some lump sum flexibility. For example: lifetime monthly payments of $2,000 plus $25,000 annually for 10 years gives you both security and flexibility to invest or cover variable expenses.

Negotiate COLA percentages. If a 3% COLA reduces initial payments too much, try 2%. Some increase is better than none for structured settlement long horizon value guide purposes.

Comparing Structured Settlements to Alternative Long-Term Financial Vehicles

Structured settlements occupy a unique space: safer than stocks, more income-focused than bonds, less flexible than investment accounts, but offering tax advantages and guarantees unavailable elsewhere.

Investment portfolios offer higher potential returns—historically 8%-10% annually for diversified stock/bond mixes—but with substantial volatility. A plaintiff who invested a $500,000 lump sum in 2007 saw it drop to $300,000 by March 2009. Even with recovery, the psychological toll and potential for panic selling destroys value. Injury victims often lack the financial sophistication or emotional capacity to ride out market crashes.

Immediate annuities (commercial products you purchase yourself) provide guaranteed income similar to structured settlements but lack the tax advantages. A $500,000 immediate annuity might pay $2,400 monthly for life, but that income is partially taxable. The equivalent structured settlement payment is entirely tax-free.

Bond ladders offer predictable income and principal preservation but require active management, provide fully taxable income, and lack the creditor protections structured settlements enjoy in most states.

Trusts provide asset protection and professional management but charge annual fees (typically 1%-2% of assets), generate taxable income, and don't guarantee income for life.

Feature Comparison Matrix

| Feature | Structured Settlements | Commercial Annuities | Bond Ladders | Managed Portfolios |

| Principal protection | Yes (guaranteed by insurance company) | Yes (guaranteed by insurance company) | Yes (if held to maturity) | No (market risk) |

| Income guarantee | Lifetime or period certain | Lifetime or period certain | Until bonds mature | No (withdrawals deplete principal) |

| Tax treatment | Tax-free (qualified settlements) | Partially taxable | Fully taxable | Fully taxable |

| Liquidity | Very low (can sell at discount) | Very low (surrender charges) | Moderate (can sell bonds) | High (can sell anytime) |

| Inflation protection | Optional (COLA riders) | Optional (COLA riders, expensive) | No (fixed payments) | Potential (stocks may outpace inflation) |

| Creditor protection | Strong (varies by state) | Moderate (varies by state) | Weak (generally accessible) | Weak (generally accessible) |

| Fees | None to plaintiff | Sales loads/commissions | Transaction costs | 1%-2% annually |

For catastrophically injured plaintiffs, structured settlements typically make sense for at least a portion of the settlement—the amount needed to cover basic living expenses and medical care for life. Additional funds can be allocated to investments for growth, trusts for asset protection, or special needs trusts to preserve government benefit eligibility.

The true value of a structured settlement isn't just the total dollars paid out—it's the guaranteed income stream that can't be outlived, lost to market crashes, or diminished by poor investment decisions. For catastrophically injured plaintiffs, that certainty over 30 or 40 years is often worth more than a higher-risk alternative

— ichael Thompson

Frequently Asked Questions About Structured Settlement Long-Term Value

Your structured settlement's long-term value depends less on the total nominal payout than on how well it preserves purchasing power, matches your changing needs over decades, and provides guaranteed security regardless of market conditions or personal financial decisions.

The mathematics are unforgiving: without inflation protection, a fixed payment structure loses roughly half its purchasing power every 28 years at average inflation rates. A settlement that feels generous at age 35 will feel inadequate at age 65 unless it includes cost-of-living adjustments.

Yet the value of certainty cannot be captured in spreadsheets alone. A guaranteed income stream that cannot be outlived, lost to market crashes, seized by creditors, or depleted through poor decisions provides economic security that alternatives cannot match. For catastrophically injured plaintiffs facing lifetime medical needs and uncertain investment expertise, this reliability often outweighs the higher potential returns of riskier alternatives.

The key is informed structuring at settlement time. Once finalized, your payment schedule is locked—you cannot add inflation protection later, cannot extend the payment period, cannot reduce current payments to increase future ones. Work with qualified professionals who can model multiple scenarios, calculate present values, and project purchasing power across your expected lifetime.

Balance immediate needs with long-term security. Ensure adequate income now, but protect your later years with COLA adjustments and lifetime payment options. Choose only highly-rated insurance companies. Coordinate with other benefits and income sources. Calculate real values, not just nominal totals.

A well-structured settlement can provide financial stability for 30, 40, or 50+ years. A poorly planned one creates a slow-motion financial crisis as inflation erodes purchasing power and fixed payments buy progressively less. The difference lies in understanding these principles and applying them before you sign.