Hand removing several payment envelopes from a neatly stacked pile on an office desk, illustrating the concept of a partial structured settlement buyout

How a Structured Settlement Partial Buyout Works

Content

A structured settlement provides guaranteed income over time, but life doesn't always wait for scheduled payments. Medical emergencies, business opportunities, or major life changes can create urgent financial needs that your monthly checks can't cover. Rather than selling your entire settlement—and losing all future income—you can sell just a portion of your payments while keeping the rest intact.

Understanding how partial buyouts work, what they cost, and how to structure them properly can mean the difference between solving a financial problem and creating a bigger one.

What Is a Partial Buyout and How Does It Differ from a Full Sale?

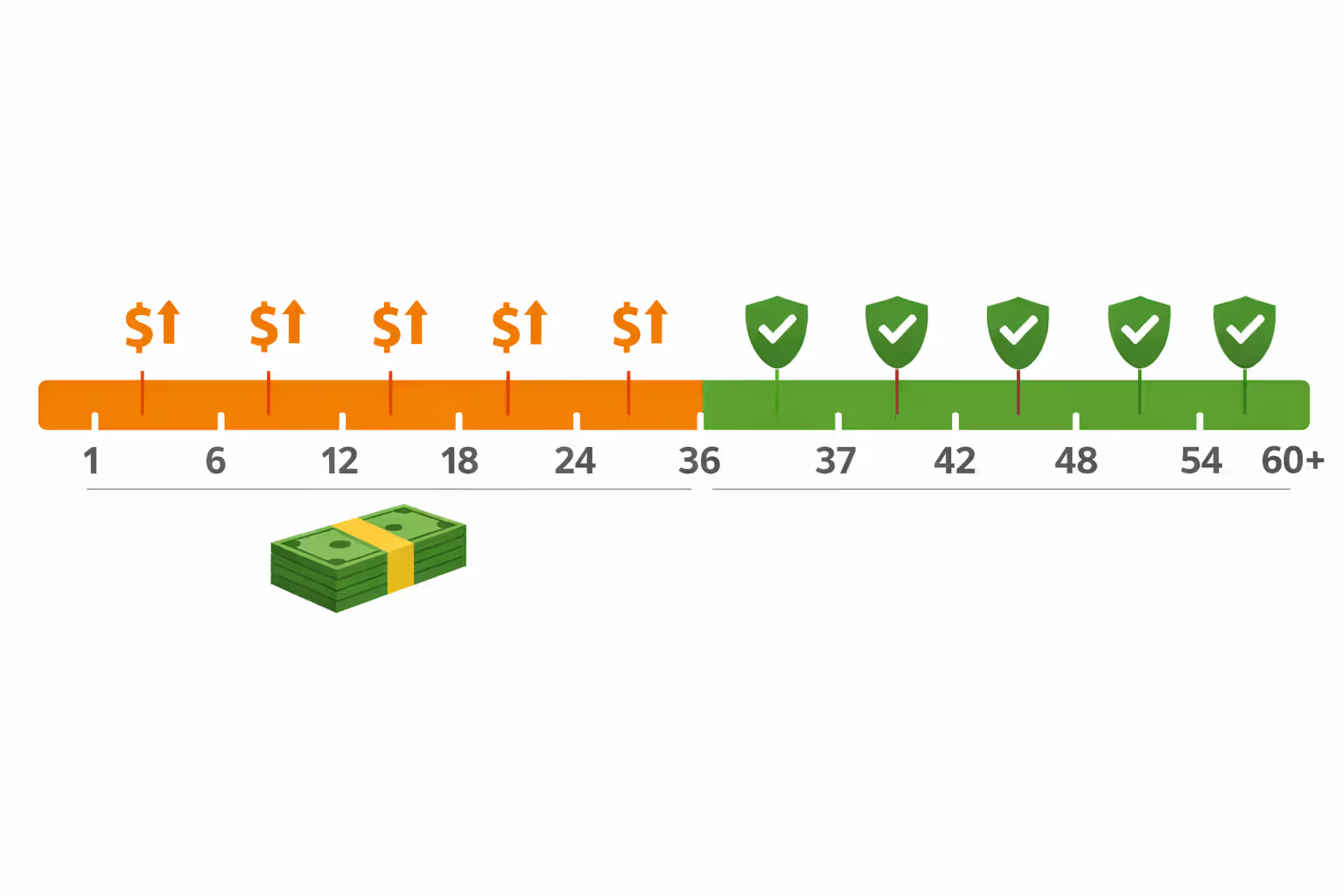

A structured settlement partial buyout means selling select future payments to a purchasing company in exchange for immediate cash, while continuing to receive your remaining scheduled payments. You might sell three years of payments while keeping everything after that, or sell every other payment for the next decade, or cherry-pick specific high-value payments that suit your needs.

This differs fundamentally from a full sale, where you transfer all remaining payments to a buyer in exchange for one lump sum. With a full sale, you sever your relationship with the annuity entirely—no more checks arrive, ever. Your guaranteed income stream ends.

The flexibility of partial buyouts lets you customize the transaction. Need $50,000? You might sell 36 monthly payments of $1,500 each. Need $100,000 but want to preserve retirement income? Sell payments scheduled for the next five years while keeping everything from age 60 onward.

Courts generally favor partial sales over full buyouts because they preserve some financial stability. Judges reviewing these transactions want to see that you'll still have income after the sale closes, reducing the risk that you'll burn through the lump sum and end up destitute.

People first, then money, then things. Never sacrifice your long-term financial foundation for a short-term fix

— Suze Orman

Why Sell Only Part of Your Structured Settlement Payments

Financial advisors recommend partial buyouts when you face a specific, quantifiable expense rather than vague "financial difficulties." The most defensible reasons include:

Medical procedures not covered by insurance. A $75,000 surgery that could improve your quality of life or prevent future complications makes a compelling case. Courts view this as using settlement money—originally awarded for injury or harm—to address related medical needs.

Home down payments. Converting $80,000 in future payments into immediate cash to secure housing eliminates rent payments and builds equity. The trade-off between paying rent indefinitely versus owning property often justifies the discount rate you'll pay.

Starting or saving a business. A $60,000 investment in a viable business plan, especially one that generates income to replace sold payments, demonstrates forward thinking. Courts want to see business plans, not just ideas.

Debt consolidation with high-interest obligations. If you're paying 18-24% interest on credit cards or payday loans, selling payments at a 12% discount rate actually improves your financial position mathematically.

Education expenses. Funding a degree that increases earning potential shows long-term planning. A nursing degree that leads to a $65,000 annual salary justifies selling $40,000 in payments.

The key advantage of keeping future payments is maintaining a financial safety net. If you receive $2,000 monthly and sell three years of payments, you know with certainty that checks resume in month 37. That guaranteed future income provides stability that a lump sum—however large—cannot match. Money in hand gets spent, stolen, lost in bad investments, or simply disappears. Money still held by the insurance company remains protected.

Author: Andrew Halvorsen;

Source: avayabcm.com

Step-by-Step Process for a Partial Settlement Payment Transfer

Finding and Vetting Buying Companies

Start by identifying companies licensed to purchase structured settlements in your state. Not all buyers operate nationwide, and using an unlicensed company can invalidate your transaction. Check your state's Department of Insurance website for licensed purchasers.

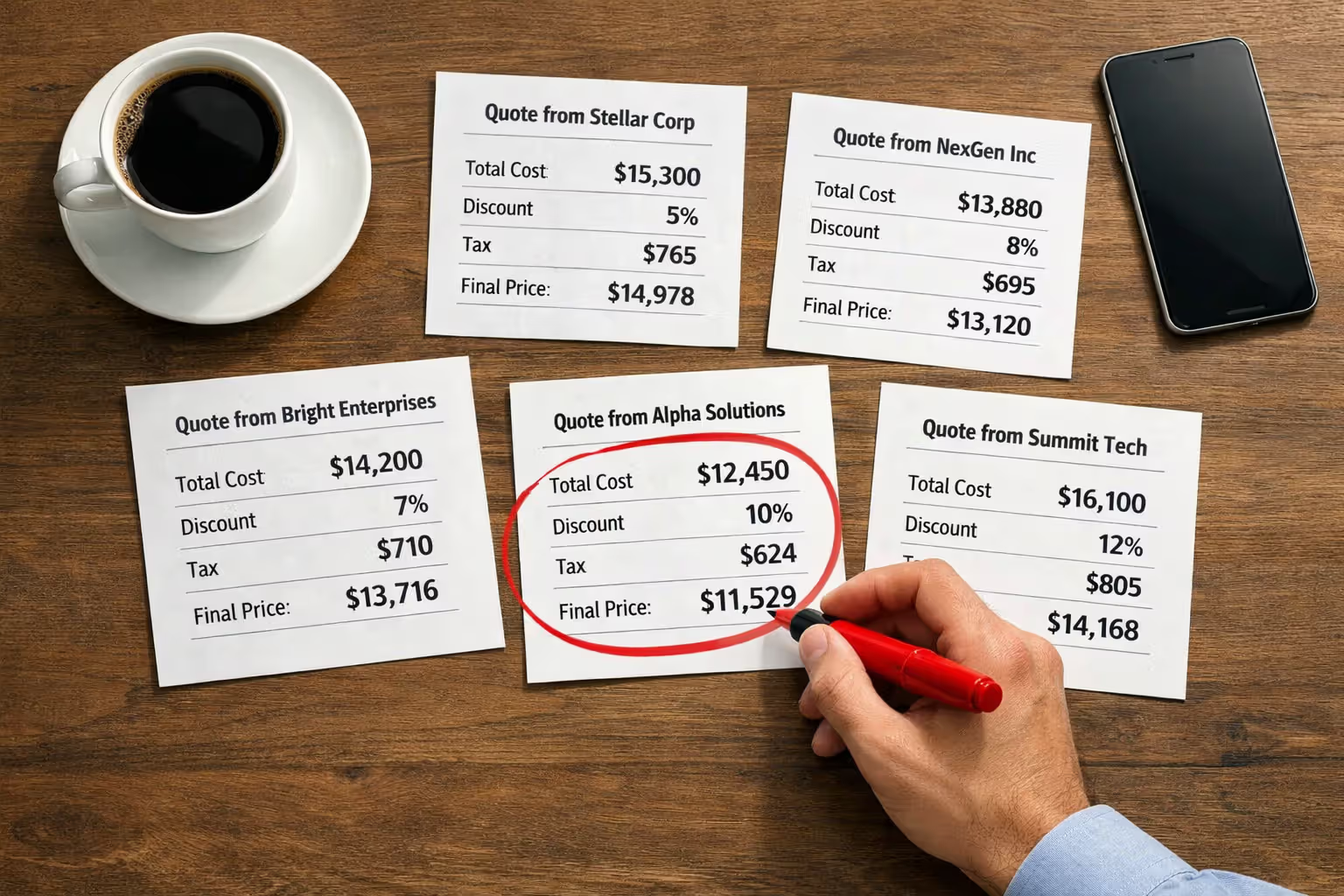

Request quotes from at least three companies. Provide identical information to each—which payments you want to sell, your age, the insurance company holding your annuity—so you can compare offers directly. Legitimate buyers won't charge application fees or require upfront payments.

Red flags include pressure tactics ("this offer expires in 24 hours"), requests for money before closing, or buyers who discourage you from seeking multiple quotes. Reputable companies expect you to shop around and won't penalize you for doing so.

Receiving and Comparing Purchase Quotes

Each quote should specify the discount rate, the exact payments you're selling, the lump sum you'll receive, and all fees. A quote might show: "We'll purchase 60 monthly payments of $1,500 (total face value $90,000) for a lump sum of $68,400, representing a 12.5% discount rate. Court filing fee: $1,200. Your net proceeds: $67,200."

Compare the net proceeds after all fees, not just the discount rate. A company offering an 11% rate but charging $3,000 in fees might deliver less cash than a competitor charging 13% with $800 in fees.

Ask how each company structures the sale. Some buyers prefer purchasing consecutive payments (months 1-60). Others might suggest skipping payments to reduce the discount rate—selling every other payment for 120 months instead of 60 consecutive months. The structure affects both the lump sum you receive and when your remaining payments resume.

Court Approval Requirements by State

Federal law requires court approval for all structured settlement transfers, and states add their own requirements. You cannot sell payments through a private agreement, even if both parties consent. A judge must review the transaction and determine it serves your best interest.

The court evaluates whether you understand the terms, whether the discount rate is reasonable, whether you're receiving independent advice, and whether the sale addresses a genuine need rather than frivolous spending. Some states require the buyer to prove the discount rate doesn't exceed statutory limits (typically 15-20% annually).

You'll attend a hearing, either in person or by phone. The judge will ask why you need the money, whether you understand you're receiving less than the face value of your payments, and whether anyone pressured you into the sale. Answer honestly and specifically. "I need $50,000 to pay for spinal surgery that will reduce my chronic pain" is compelling. "I want money for stuff" is not.

Expect the court to inquire about alternatives. Be prepared to explain why a bank loan won't work, whether family members can help, or why you chose a partial sale over a full buyout.

Author: Andrew Halvorsen;

Source: avayabcm.com

Timeline from Application to Funding

The entire process typically takes 60-90 days, though simple cases in cooperative states can close in 45 days. Complex situations—disputes with insurance companies, multiple beneficiaries, unclear annuity terms—can stretch to 120 days.

Week 1-2: You submit applications to multiple buyers and receive quotes. Week 3: You select a buyer and sign a purchase agreement. Week 4-6: The buyer files court paperwork and serves notice to all required parties (the insurance company, any beneficiaries, government agencies if you receive benefits). Week 7-8: The court schedules a hearing. Week 9-10: The hearing occurs and the judge issues an order. Week 11-12: The insurance company processes the order and the buyer funds your lump sum.

The insurance company holding your annuity can delay the process by requesting additional documentation or objecting to the sale terms. They cannot block a sale simply because they don't like it, but they can raise legitimate concerns about fraud, forged signatures, or violations of the original settlement agreement.

Legal Rules and Restrictions Governing Partial Sales

The federal Structured Settlement Protection Act, enacted in 2002, establishes baseline protections. It requires court approval, mandates that buyers disclose all terms in plain language, and imposes tax penalties on buyers who circumvent state laws. The Act doesn't set discount rate limits or dictate specific approval criteria—it defers to state regulations for those details.

State laws vary significantly. Florida caps discount rates at 18% annually. California requires buyers to pay for independent professional advice (typically an attorney or financial advisor) to counsel you before the sale. New York demands extensive documentation proving financial hardship. Some states require waiting periods between when you apply and when the court can approve the sale, preventing impulsive decisions.

The "best interest" standard appears in nearly every state's statute. Courts must find that the transfer serves your best interest, considering your age, mental capacity, financial situation, and the reason for selling. A judge can reject a sale even if you want to proceed, if they believe it harms your long-term welfare.

Disclosure requirements force buyers to provide a written document explaining the discount rate, the total amount you're giving up versus receiving, all fees, and your right to cancel within a specified period (usually 3-5 business days after signing). You must acknowledge receiving and understanding this disclosure.

Special rules apply if you receive government benefits. Medicaid, SSI, and other means-tested programs count lump sums as assets, potentially disqualifying you from benefits. Courts scrutinize these situations carefully, sometimes requiring you to establish a special needs trust to hold the proceeds.

Calculating Your Buyout: Discount Rates and What You'll Actually Receive

Discount rates reflect the time value of money and the buyer's profit margin. A dollar today is worth more than a dollar in five years because today's dollar can be invested and earn returns. Buyers apply discount rates to calculate what your future payments are worth in today's dollars, then subtract their profit.

Typical discount rates range from 9% to 18% annually, depending on several factors. Lower rates (9-12%) apply when you're selling near-term payments to highly-rated insurance companies with minimal processing complexity. Higher rates (14-18%) apply when you're selling distant payments, when the insurance company has a lower credit rating, or when the transaction involves complications like multiple beneficiaries or unclear annuity terms.

A 10% discount rate doesn't mean you receive 90% of your payment's face value—it compounds annually. Selling $100,000 in payments due over five years at 10% yields approximately $62,000, not $90,000. The further in the future your payments, the more the discount rate reduces their present value.

| Scenario | Payments Sold | Face Value | Discount Rate | Lump Sum (Before Fees) | Approximate Fees | Net Proceeds | Payments Retained |

| A: Short-term need | 36 months @ $1,500 | $54,000 | 10% | $41,800 | $1,200 | $40,600 | All payments after month 36 |

| B: Medium-term need | 60 months @ $1,500 | $90,000 | 12% | $62,400 | $1,500 | $60,900 | All payments after month 60 |

| C: Larger immediate need | 120 months @ $1,500 | $180,000 | 14% | $105,300 | $2,000 | $103,300 | All payments after month 120 |

| D: Cherry-picking high payments | 10 annual payments @ $18,000 | $180,000 | 11% | $108,900 | $1,800 | $107,100 | All monthly payments continue |

Scenario D demonstrates a strategic approach: selling ten large annual payments while keeping smaller monthly payments provides substantial cash without eliminating regular income. This works well if your settlement includes both monthly and annual payments.

To estimate your net proceeds, find a present value calculator online (many structured settlement companies provide them). Input the payment amount, frequency, number of payments, and discount rate. Subtract 2-4% for fees. That's roughly what you'll receive.

Common Mistakes When Selling a Portion of Your Structured Settlement

Selling too much too soon. Clients often overestimate how much they need or underestimate future expenses. Needing $40,000 for a down payment doesn't mean you should sell $80,000 in payments "just in case." Sell the minimum that addresses your specific need. You can always sell more payments later if necessary, but you cannot undo a sale.

Ignoring tax implications. Structured settlement payments received for physical injury or sickness are tax-free under IRS rules. The lump sum you receive from selling those payments remains tax-free. However, if you invest the lump sum and it generates income, that investment income is taxable. More critically, if you receive means-tested benefits, the lump sum counts as an asset that could disqualify you from Medicaid, SSI, or housing assistance until you spend it down.

Choosing the wrong payment periods. Selling your next 60 payments seems straightforward, but what if those include higher annual payments mixed with smaller monthly ones? You might give up $120,000 in face value when selling different payments would cost you only $100,000 in face value for the same lump sum. Map out your entire payment schedule and identify which payments to sell for maximum efficiency.

Not shopping multiple buyers. A 3% difference in discount rate on a $100,000 transaction means $3,000 more in your pocket. Accepting the first offer costs you real money. Get at least three quotes, preferably five.

Missing court dates or submitting incomplete paperwork. Courts dismiss cases when applicants don't appear for hearings or fail to provide required documentation. Dismissal means starting over, delaying your funding by another 60-90 days. Mark your court date on multiple calendars, set phone reminders, and confirm the hearing date with the court clerk one week prior.

Failing to read the purchase agreement carefully. Some agreements include clauses requiring you to sell additional payments to the same buyer if you need money in the future, or restricting your ability to sell other payments to competitors. These clauses may not be enforceable, but fighting them in court costs time and money.

Underestimating living expenses during the waiting period. If you're selling payments to pay off debt, remember that you'll still need to make minimum payments during the 60-90 day approval process. Budget for this gap.

Author: Andrew Halvorsen;

Source: avayabcm.com

Alternatives to Consider Before Proceeding with a Partial Buyout

Structured settlement loans. Some companies offer loans secured by your future payments, advancing you money now that you repay from incoming payments. Interest rates are typically high (15-25%), but you retain ownership of your payments. If you need money for six months until another income source materializes, a short-term loan might cost less than permanently selling payments at a discount.

Personal loans or lines of credit. If you have decent credit, a bank personal loan at 8-12% interest might beat selling payments at a 14% discount rate, especially if you can repay the loan from your ongoing settlement income. The loan preserves your full payment stream.

Payment acceleration clauses. Some structured settlements include provisions allowing you to request accelerated payments directly from the insurance company in emergencies. These clauses are rare, but check your original settlement agreement. If available, acceleration avoids discount rates entirely.

Negotiating with creditors. If debt drives your need for cash, contact creditors directly. Many will accept reduced lump-sum settlements (60-70% of the balance) rather than risk receiving nothing if you file bankruptcy. Selling $40,000 in payments to settle $60,000 in debt makes sense. Selling $60,000 in payments to settle $60,000 in debt does not.

Family loans. Borrowing from relatives eliminates discount rates and court fees. Structure it formally with a written agreement, repayment schedule, and modest interest rate to keep it legitimate. Repay the loan from your ongoing settlement income.

Financial counseling. Non-profit credit counseling agencies (find them through the National Foundation for Credit Counseling) provide free budget analysis and debt management plans. A counselor might identify expense reductions or income sources you've overlooked, reducing or eliminating your need to sell payments.

Bankruptcy protection. If debt is overwhelming, bankruptcy might discharge obligations without touching your structured settlement. Federal law exempts structured settlements from bankruptcy estates in many cases, meaning creditors cannot seize your payments. Consult a bankruptcy attorney before selling payments to pay dischargeable debt.

Author: Andrew Halvorsen;

Source: avayabcm.com

Frequently Asked Questions About Partial Settlement Buyouts

A structured settlement partial buyout offers a middle path between financial crisis and long-term security. By selling only what you need and preserving future income, you address immediate challenges without sacrificing the guaranteed payments that provide stability.

Success requires careful planning: shop multiple buyers to find the best rates, understand exactly which payments you're selling and when your remaining payments resume, and prepare a clear explanation for the court about why this sale serves your best interest. The discount rate you pay is the cost of accessing future money now—make sure that cost is justified by a genuine need, not impulse spending or poor planning.

Before signing any agreement, verify the buyer is licensed in your state, read every clause in the purchase agreement, and calculate your net proceeds after all fees. Consider alternatives like personal loans or family assistance that might cost less than permanently selling payments.

The structured settlement was designed to protect you from spending a large award too quickly. A partial buyout respects that protection while acknowledging that life sometimes demands flexibility. Approach the decision methodically, use the transaction to solve a specific problem, and preserve as much future income as possible.