Calculator, financial documents, laptop with percentage rate charts, and dollar bills on an office desk — structured settlement pricing concept

What Factors Affect Structured Settlement Pricing When You Sell

Content

Understanding what drives the cash value of your structured settlement can mean the difference between accepting a fair offer and leaving tens of thousands of dollars on the table. The pricing mechanisms behind these transactions involve complex calculations that most settlement holders never see, yet these factors directly determine how much money lands in your bank account.

The structured settlement secondary market operates differently than traditional asset sales. You're not selling something with an easily observable market price—instead, buyers calculate what your future payment stream is worth today based on mathematical formulas, risk assessments, and their own profit requirements. Seven primary factors shape these calculations, and knowing how each one affects your payout puts you in a stronger negotiating position.

How Discount Rates Impact Your Settlement's Cash Value

The discount rate represents the single most powerful force in determining what you'll receive for your structured settlement. This percentage—typically ranging from 9% to 18%—gets applied to your future payments to calculate their present value. Think of it as working backwards: if you're supposed to receive $100,000 over ten years, a buyer applies their discount rate to determine what that future money is worth in today's dollars.

Here's a concrete example: A settlement with $120,000 in remaining payments might fetch $75,000 at a 12% discount rate but only $68,000 at a 15% discount rate. That three-percentage-point difference costs you $7,000.

Why such a wide range? Several factors influence where your rate falls. Larger purchasing companies with lower operating costs often offer better rates than smaller brokers who need wider margins. The length of your payment stream matters too—longer-term payments typically face higher discount rates because buyers take on more uncertainty about future economic conditions. A payment stream extending 25 years will usually be discounted more heavily than one ending in five years.

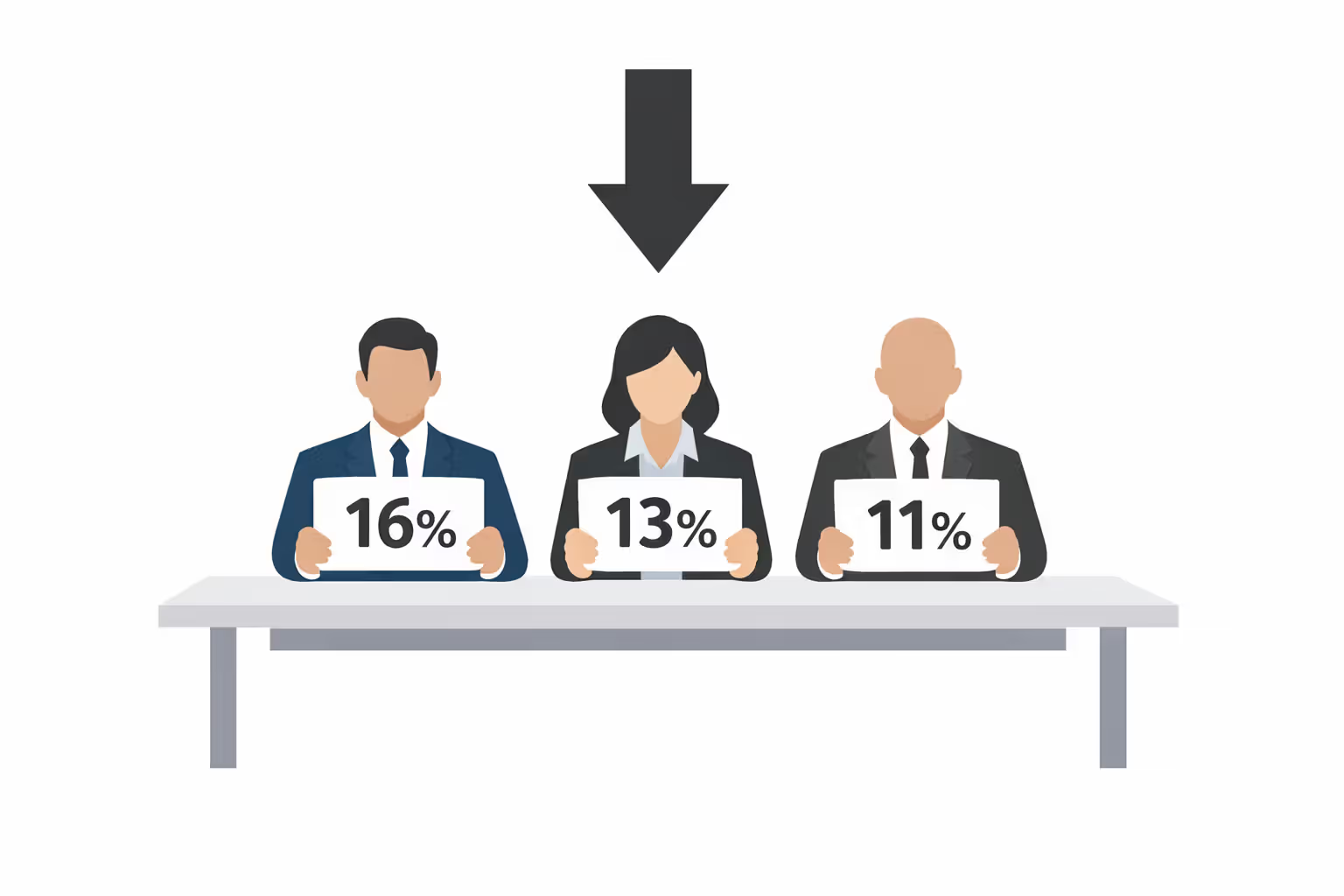

Competition plays a significant role. When multiple buyers bid for your settlement, rates improve. A single quote might come in at 16%, but three competing offers could push the best rate down to 11%. The difference between these scenarios on a $150,000 settlement can exceed $20,000.

Author: Christopher Vaughn;

Source: avayabcm.com

The buyer's cost of capital also factors in. Companies that borrow money to purchase settlements must cover their own interest expenses plus profit margin. During periods when institutional lending rates rise, you'll see those costs passed along through higher discount rates.

Payment Schedule and Timing: Why When You Get Paid Matters

Not all structured settlements are created equal from a pricing perspective. The timing and structure of your payments significantly affect how much cash you'll receive, even when the total dollar amount is identical.

Immediate vs. Deferred Payments

Payments scheduled to arrive within the next 12-24 months command premium pricing. A settlement paying $50,000 over the next two years will fetch a higher percentage of face value than one paying the same amount over ten years. The reason is straightforward: money received sooner carries less risk and requires shorter holding periods for buyers.

Consider two settlements, each worth $100,000 total. Settlement A pays $2,000 monthly for 50 months starting immediately. Settlement B pays $2,000 monthly for 50 months but doesn't begin for five years. Settlement A might sell for 72% of face value while Settlement B fetches only 48%. The five-year deferral period dramatically reduces present value.

Lump Sum vs. Periodic Payment Structures

Settlements structured with occasional large balloon payments mixed with smaller periodic payments create pricing complexities. Buyers typically value the near-term lump sums more favorably. If your settlement includes a $30,000 payment next year followed by $500 monthly for ten years, the large payment will be discounted less aggressively than the smaller ongoing stream.

Payment frequency also matters, though less dramatically. Monthly payments are standard and price predictably. Annual payments in smaller settlements sometimes face slightly higher discount rates because buyers prefer more frequent cash flow for their own financial management.

Market Conditions and Economic Factors Affecting Settlement Values

The broader economic environment shapes settlement pricing in ways most sellers don't anticipate. These settlement pricing variables guide what buyers can afford to pay while maintaining their business models.

Interest rates set the baseline. When Treasury yields and corporate bond rates rise, structured settlement buyers can earn better returns on alternative investments, which pushes them to demand higher discount rates on settlements. During 2022's rapid interest rate increases, typical discount rates climbed 2-3 percentage points compared to the previous three years. Sellers who transacted in late 2021 received substantially better pricing than those who waited until mid-2023.

Inflation expectations also influence pricing. Buyers recognize that the fixed payments they're purchasing will be worth less in real terms as inflation rises. During high-inflation periods, this concern translates into less aggressive pricing offers.

Competition among purchasing companies varies with market conditions. When capital is plentiful and many buyers are actively seeking settlements, pricing improves. Conversely, during credit crunches or economic uncertainty, fewer buyers compete and those remaining become more selective with tighter pricing.

| Economic Environment | Typical Discount Rate Range | Cash-Out Percentage | Buyer Competition Level |

| Low Interest Rates (2019-2021) | 8-14% | 65-80% of face value | High - Many active buyers |

| Moderate Rates (2015-2019) | 10-16% | 60-75% of face value | Moderate - Stable market |

| High Interest Rates (2022-2024) | 12-18% | 55-70% of face value | Lower - Selective buyers |

The table shows how dramatically market conditions can shift your potential payout. A $100,000 settlement might fetch $80,000 in favorable conditions but only $55,000 when rates spike and competition wanes.

Your Credit Profile and Financial Circumstances

While structured settlement sales aren't loans and don't require credit approval in the traditional sense, your financial profile affects the pricing you'll receive in subtle ways.

Buyers assess whether you're likely to complete the transaction. Court approval is required for structured settlement transfers, and judges sometimes deny petitions they view as financially imprudent. If your credit report shows recent bankruptcy, numerous defaults, or patterns suggesting financial mismanagement, some buyers perceive higher risk that a judge might reject the transfer. This concern may lead them to offer less competitive pricing or require more extensive documentation before committing resources to the transaction.

Your demonstrated financial need influences negotiating leverage. Buyers know that sellers facing foreclosure or urgent medical bills have less flexibility to wait for better offers or shop extensively. While this shouldn't affect pricing in an ideal market, the reality is that urgent circumstances often result in accepting the first available offer rather than pursuing the best possible deal.

The opposite holds true as well. Sellers who clearly have time to evaluate multiple offers and no pressing emergency typically negotiate better terms. One structured settlement consultant noted that clients who obtained three or more competitive quotes received offers averaging 11% higher than those who accepted their first quote.

Author: Christopher Vaughn;

Source: avayabcm.com

State Regulations and Legal Requirements That Influence Pricing

The state where your settlement was issued and where you reside significantly impacts pricing through varying legal requirements and associated costs. These settlement price determinants guide what buyers must spend beyond the purchase price itself.

Court approval processes vary widely. Some states have streamlined procedures costing $500-$1,000 in legal fees and completing within 45-60 days. Others require more extensive hearings, independent professional advice, and longer waiting periods that can push legal costs to $2,500-$4,000 and extend timelines to 90-120 days. Buyers factor these costs and delays into their pricing.

Transfer fees and recording costs add up. Depending on jurisdiction, you might encounter court filing fees ($200-$500), document recording fees ($50-$200), and mandatory independent advisor fees ($300-$1,000). While buyers typically cover these costs, they reduce the net amount they can offer while maintaining their profit margins.

Some states impose specific consumer protections that affect pricing. A few require buyers to disclose their effective discount rates in plain language or mandate minimum waiting periods between signing agreements and court hearings. While these protections benefit sellers, they add compliance costs that buyers incorporate into pricing models.

State-specific attorney requirements also matter. Certain jurisdictions require both parties to have separate legal representation, doubling legal costs compared to states where a single attorney can handle the transaction. A settlement transfer in New York or California might cost $1,500 more in legal fees than the identical transaction in Florida or Texas.

Insurance Company Ratings and Payment Security

The financial strength of the insurance company making your settlement payments—called the obligor—directly affects what buyers will pay. This often-overlooked factor can swing pricing by 5-10% on identical payment streams.

Buyers evaluate obligor risk because they're stepping into your shoes. If the insurance company fails, payments stop. Settlements backed by highly-rated insurers (A.M. Best rating of A+ or A++) command premium pricing. These top-tier carriers have demonstrated decades of financial stability and maintain substantial reserves.

Settlements backed by lower-rated insurers (A- or below) face steeper discount rates. A payment stream from a B+ rated carrier might be discounted 2-3 percentage points more heavily than an identical stream from an A++ carrier. On a $100,000 settlement, this rating difference could cost you $6,000-$8,000.

Some buyers won't purchase settlements from insurers below certain rating thresholds regardless of price. If your obligor carries a rating below B+, you may find fewer buyers willing to bid, which reduces competition and further pressures pricing.

The obligor's rating can change over time. If your insurance company was downgraded since your settlement was established, you'll face tougher pricing than anticipated. Conversely, upgrades can improve your position.

Author: Christopher Vaughn;

Source: avayabcm.com

Common Pricing Mistakes That Cost Sellers Thousands

Most settlement holders make predictable errors that diminish their payouts. Recognizing these pitfalls helps you avoid them.

Accepting the first offer without comparison shopping ranks as the costliest mistake. The first buyer who contacts you has no incentive to provide their best pricing upfront. They're testing whether you'll accept a below-market offer. One analysis of transactions found that sellers who obtained only one quote received offers averaging 14% lower than fair market value. Getting three quotes from reputable buyers should be standard practice.

Misunderstanding fee structures creates confusion and disappointment. Some buyers quote attractive headline numbers but bury significant fees in the paperwork. Always ask for the net amount you'll receive after all fees, costs, and deductions. A quote of "$75,000 purchase price" might actually deliver only $69,000 after various charges.

Selling more payments than necessary is another expensive error. If you need $50,000, don't sell $80,000 worth of payments just because a buyer suggests it. Partial sales—transferring only enough payments to meet your needs—preserve more of your long-term financial security. The payments you keep continue arriving tax-free on their original schedule.

Failing to verify buyer credentials leads some sellers to work with unlicensed brokers or companies with poor track records. Check whether buyers are members of the National Association of Settlement Purchasers and verify their standing with the Better Business Bureau. Disreputable buyers may offer attractive initial quotes but create problems during the transaction or add unexpected fees.

The biggest pricing factor most settlement holders overlook is the time value of their own patience. Sellers who take 30 days to gather multiple competing bids typically receive 8-12% more than those who rush to accept the first offer within a week. That patience translates directly into thousands of additional dollars

— Robert Chen

Timing your sale poorly relative to market conditions can be costly. Selling during periods of rising interest rates typically results in worse pricing than selling when rates are stable or falling. While you can't always control when financial needs arise, understanding rate trends helps you decide whether to proceed immediately or wait a few months if circumstances allow.

Frequently Asked Questions About Settlement Pricing

The seven factors controlling structured settlement pricing interact in complex ways that make each transaction unique. Your specific combination of payment timing, obligor strength, market conditions, and state regulations creates a distinct valuation profile.

Armed with knowledge of these settlement pricing components, you can approach the market strategically. Obtain multiple quotes from established buyers. Ask detailed questions about discount rates and fees. Verify that you're selling only what you truly need. Consider market timing if your circumstances allow flexibility.

The difference between an uninformed seller accepting the first convenient offer and a knowledgeable seller who shops carefully often exceeds $15,000-$25,000 on a typical six-figure settlement. These aren't trivial amounts—they represent months of your original settlement payments that you either preserve or sacrifice based on how well you understand the pricing mechanisms at work.

Your structured settlement represents years of future financial security. Understanding exactly what drives its cash value today ensures you make decisions that serve your long-term interests rather than simply solving immediate problems at excessive cost