Locked stack of dollar bills with heavy chain and padlock, judge gavel and legal documents in blurred background, concept of structured settlement liquidity restrictions

How to Evaluate Structured Settlement Liquidity Options Before Selling

Content

Life has a way of throwing curveballs when you least expect them. Your structured settlement sends $1,200 every month like clockwork, but suddenly your roof caves in, your kid needs emergency surgery, or a business opportunity lands in your lap that requires $30,000 next week—not next year.

Here's the uncomfortable truth: those regular payments you've been counting on? They're locked up tighter than Fort Knox. Getting your hands on that money early means navigating a maze of legal hoops, paying brutal fees, and potentially losing 40-60% of your settlement's value. But sometimes you don't have a choice.

Let's cut through the marketing spin and look at what your actual options are.

What Makes a Structured Settlement Liquid or Illiquid?

When you settled your injury case or lawsuit, the defendant's insurance company bought an annuity in your name. That annuity pumps out payments on a predetermined schedule—maybe $800 monthly for 20 years, or $2,500 quarterly for life. You don't own the annuity itself; you own the right to receive those payments.

That distinction matters because you can't just cash out an annuity you don't technically own.

The feds made things even trickier back in 1997. IRC Section 5891 slaps a 40% excise tax on anyone who messes with settlement terms after the ink dries. That's aimed at defendants and insurance companies, but it creates a massive roadblock. They won't touch your settlement structure with a ten-foot pole.

Then states jumped in during the early 2000s. Legislators watched recipients sell 20 years of payments for pennies on the dollar, then end up broke and desperate. So 48 states passed Structured Settlement Protection Acts. These laws force you to get a judge's blessing before selling even one payment.

The court approval requirement isn't just red tape—it's your safety net. A judge reviews whether the sale makes sense for your situation, whether the company is ripping you off, and whether you'll wind up worse off after the dust settles. That process takes weeks or months and creates uncertainty for everyone involved.

How easily you can tap your settlement depends on several variables. If you've got 30 years of payments left, buyers will compete for your business. Five years remaining? Much less interest. Larger monthly amounts attract better offers. And your state matters enormously—California and Florida have streamlined processes, while some states make it painful.

Five Primary Methods to Access Structured Settlement Cash

Full Sale of Future Payments

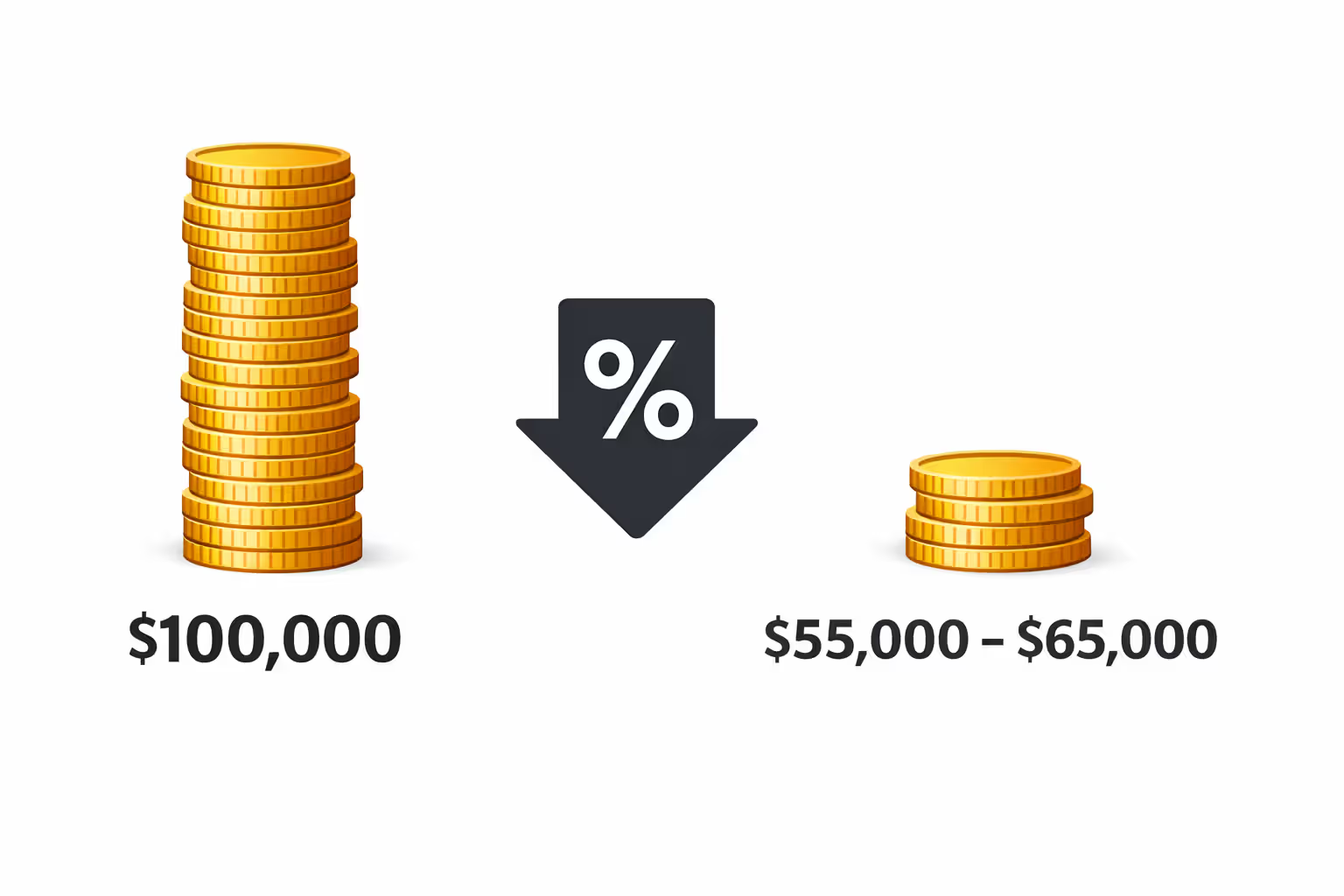

This is the nuclear option. You're essentially telling the court: "I want to trade my entire future payment stream for a lump sum today." A factoring company calculates what they'll pay (spoiler: way less than face value), you agree to the terms, and once the judge signs off, you get a check.

Let's say you've got $100,000 in payments coming over the next decade. You might walk away with $55,000 to $65,000 cash, depending on the discount rate the company applies. That missing $35,000 to $45,000? That's their profit.

People choose this route for major life purchases—buying a house outright, starting a business that requires substantial capital, or covering catastrophic medical expenses that insurance won't touch. One guy I know about sold his entire settlement to buy a franchise location. He'd done the math and knew the business income would replace what he lost. Smart? Debatable. But at least he had a plan.

The downside is permanent. You're giving up guaranteed, tax-free income for the rest of that payment period. If your circumstances improve, if you regret the decision, if the reason you needed money evaporates—tough luck. The sale is forever.

Author: Andrew Halvorsen;

Source: avayabcm.com

Partial Sale (Splitting Payment Rights)

This approach lets you keep your cake and eat some of it too. You might sell your next 60 monthly payments while keeping everything after that. Or you could split each payment 50/50 indefinitely—you get $400 per month, the buyer gets $400.

Partial sales make sense when you need a specific chunk of money but want to preserve some future income. Say you need $25,000 for a medical procedure. Instead of selling everything, you calculate how many payments it takes to get that amount (plus the company's cut), sell just those, and keep the rest.

The math works differently depending on which structure you choose. Selling a set number of payments means you'll eventually get back to full payment amounts. You're creating a temporary gap in your income. Splitting payments permanently reduces what you receive forever, but you maintain some cash flow throughout.

Both options use the same brutal discount rates as full sales. You're still losing a huge percentage of your settlement's value. But at least you're not gutting your entire financial future for a current need.

Lump Sum Advances vs. Factored Sales

Here's where things get sketchy. Companies throw around terms like "advance" and "immediate cash" to make it sound like you're getting a friendly loan. You're not.

A true factored sale means the company owns those payments after the court approves the transfer. You've sold them property rights—they get the money from the insurance company going forward, regardless of what happens to you.

What some outfits call "advances" are actually factored sales with faster timelines. They're not lending you money against your settlement; they're buying payment rights and positioning it like a loan to sound less permanent.

Genuine advances—where a company lends you money and you repay them from incoming payments—barely exist anymore. When you do find them, the effective interest rates are insane. We're talking 80%, 100%, sometimes 150% when you calculate the actual annual percentage rate. Loan sharks charge less.

If someone's offering you cash in 48 hours with no court approval, run. Either they're operating illegally, charging predatory rates that would make a payday lender blush, or they're flat-out scamming you.

Settlement Loan Products

A handful of companies will loan you money using your settlement as collateral instead of buying your payment rights. Think of it like a home equity loan, except your structured settlement is the house.

These products are rare for good reasons. The lender typically gives you less money than a factored sale would (maybe 40-50% of your payment value instead of 55-60%) because they want a cushion protecting their loan. Interest rates run 15-25% annually. And you've got to make loan payments whether you're still receiving settlement money or not.

The one advantage? Reversibility. Pay off the loan and you keep all your future payments intact. That flexibility costs you in the form of high interest and lower upfront cash, but at least there's an exit ramp.

Default on one of these loans and you're in deep trouble. The lender can force a sale of your payments to recover what you owe, leaving you with neither the loan money (you already spent it) nor your future income.

Court-Approved Payment Modifications

In a perfect world, you'd go to the insurance company and say, "Hey, instead of these monthly payments, how about restructuring to give me a lump sum now?" They'd crunch some numbers and agree to terms that don't cost you an arm and a leg.

That world doesn't exist.

Insurance companies have zero incentive to modify settlement terms. They've already paid for the annuity. Changing the structure creates administrative headaches, potential tax complications, and no upside for them. The original defendant? They're long gone, with no reason to revisit a settled case.

This option theoretically exists if your settlement paperwork includes modification language, or if every original party agrees to changes. In 15 years of covering this industry, I've seen it happen maybe twice. Both times involved terminal illness situations where the insurance company agreed out of basic human decency, not legal obligation.

Don't count on this path. Focus your energy on the realistic options.

The Factoring Process: Steps from Application to Cash

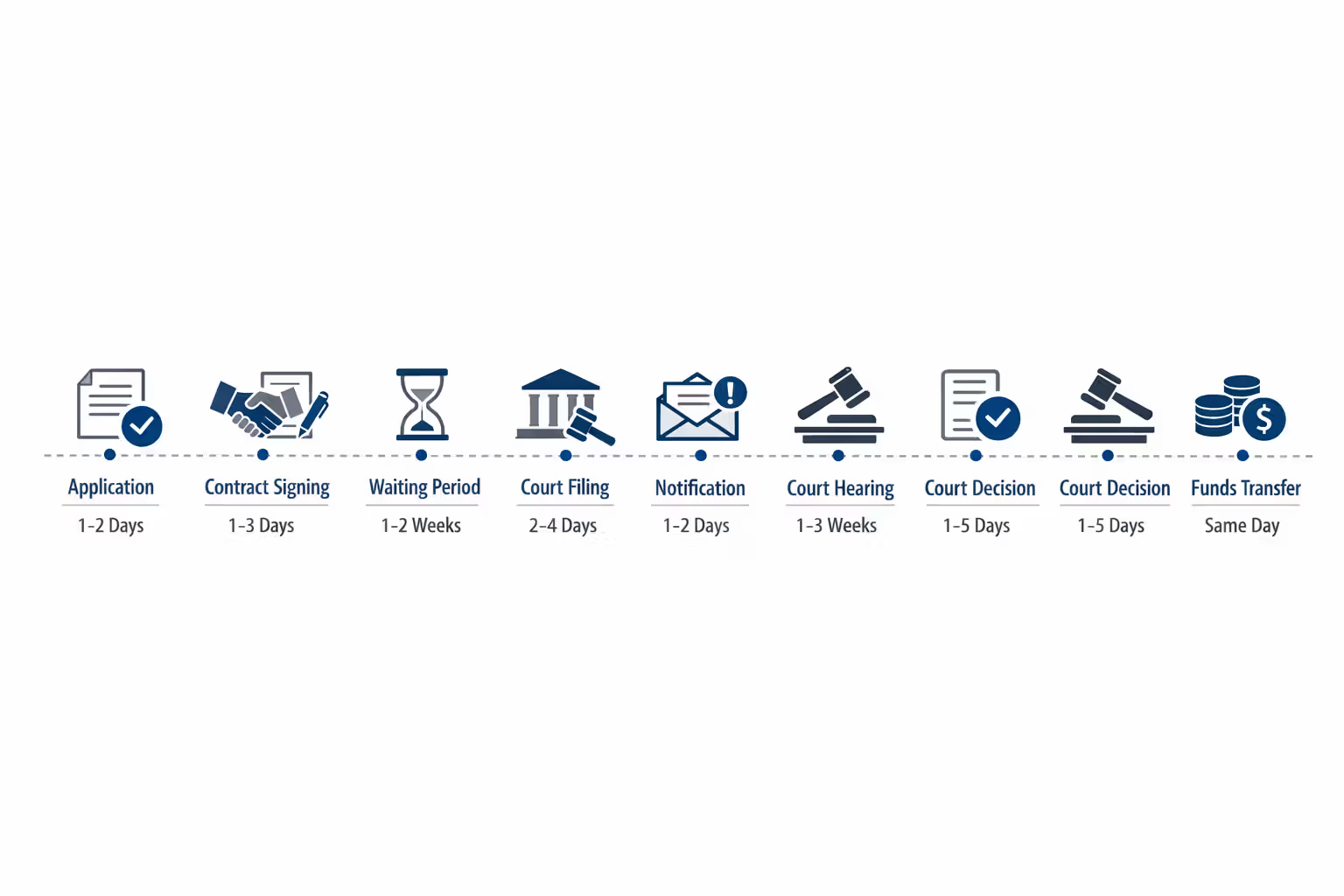

Most companies promise 45 to 90 days from "hello" to check in hand. Expedited services claim two to three weeks for simple cases. Here's what actually happens:

Initial Application and Quote: You contact a factoring company—let's call them QuickCash Settlement Buyers—and give them the basics. How much do you get monthly? How long do payments continue? Who's the insurance company? They run calculations using their discount rate (typically 9-18% depending on competition and how desperate you seem) and spit out a quote. "We'll give you $42,000 for your next 72 payments totaling $72,000."

Contract Signing: Their quote looks acceptable, so you sign a transfer agreement. This document spells out exactly which payments you're selling and what you're getting. Read every word. Seriously. I've seen contracts where the payment description on page 3 didn't match the quote on page 1. Those discrepancies aren't accidents.

Disclosure Period: Most states mandate a waiting period after signing—anywhere from three days to two weeks. During this window, you can walk away without consequences. This pause exists specifically so you can wake up the next morning, reconsider, and bail if you're having second thoughts.

Court Petition Filing: QuickCash files paperwork with your county court asking a judge to approve the transfer. The petition includes your signed agreement, disclosure statements explaining the costs, and typically a financial affidavit where you explain why you need the money.

Notification: The court sends notice to the insurance company holding your annuity and potentially the original defendant. These parties can object if they think you're getting screwed or the company is behaving unethically. Objections are uncommon but not unheard of. When they happen, everything grinds to a halt while the judge sorts it out.

Court Hearing: You show up to court (most states require in-person attendance, though some allow phone appearances) and answer the judge's questions. Why do you need this money? Do you understand how much you're losing? Have you considered other options? Did anyone pressure you? The hearing usually takes 10-15 minutes unless complications arise.

Judicial Review: The judge evaluates whether the sale serves your best interest under state law. They're looking at your age, financial sophistication, how you'll use the funds, whether the discount rate is reasonable, and whether the company followed all legal requirements. Judges reject 5-10% of petitions, usually for excessive discount rates or concerning circumstances.

Order Entry and Funding: After approval, the court issues an order authorizing the transfer. QuickCash sends your payment within 5-10 business days. Watch for last-minute deductions—some companies have a magical way of discovering "administrative fees" or "processing costs" right before funding. Get the final net amount in writing before the hearing.

You'll need to provide identification, proof of address, your original settlement agreement, and often financial records like bank statements. Companies also need your annuity contract details. If you don't have that paperwork, you can request it from the insurance company, though they'll take their sweet time sending it.

Author: Andrew Halvorsen;

Source: avayabcm.com

Calculating the Real Cost of Selling Future Payments

Discount rates sound deceptively simple. "We use a 12% discount rate" sounds almost reasonable—until you realize what it actually means.

That rate gets applied to calculate present value of future payments. A payment you'd receive in year eight is worth substantially less today than a payment coming next month. The company calculates the present value of every payment they're buying, adds them up, and that's your offer. They'll collect the full face value while you get the discounted amount.

The longer the time period, the more violent the discount. Here's what different scenarios look like in practice:

| Scenario | Original Payment Value | Payments Being Sold | Discount Rate | Cash Received | Total Cost | Effective Annual Cost |

| Five-year partial | $50,000 total | 60 months × $833 | 12% | $36,800 | $13,200 | 26.4% |

| Ten-year partial | $100,000 total | 120 months × $833 | 12% | $58,200 | $41,800 | 41.8% |

| Five-year with higher rate | $50,000 total | 60 months × $833 | 18% | $32,100 | $17,900 | 35.8% |

| Fifteen-year full sale | $150,000 total | 180 months × $833 | 15% | $70,500 | $79,500 | 53.0% |

Look at that last scenario. You're giving up more than half your settlement's total value. The discount rate is only 15%, but you're losing 53% of your money because of how far out those payments extend.

Even the "best" scenario costs you over a quarter of your settlement. That's not a small price tag.

Beyond the discount rate, watch for hidden deductions. Court filing fees run $500 to $2,000—sometimes the company pays these, but often they come out of your proceeds. Some outfits charge administrative fees, processing fees, or broker commissions. I've seen total deductions reach $5,000 on top of the discount rate losses.

Independent advice costs money upfront ($500-$1,500 for an attorney or financial advisor to review everything) but often saves you multiples of that fee. A good advisor spots unfavorable clauses, negotiates better terms, or identifies alternatives you hadn't considered. Companies that discourage independent review are telling you everything you need to know about whether they have your best interests at heart.

State-Specific Regulations That Impact Your Liquidity Options

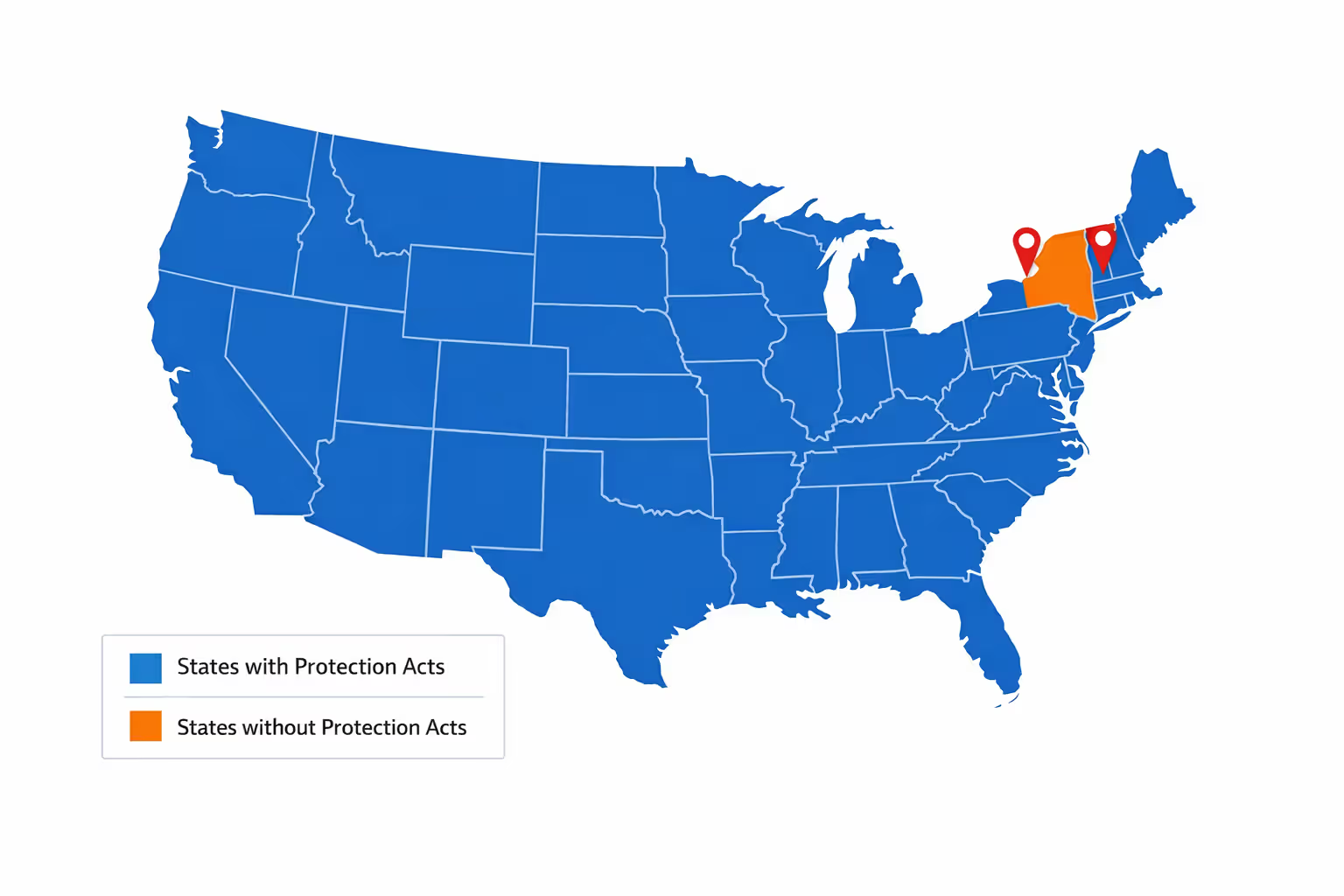

Forty-eight states have Structured Settlement Protection Acts on the books. New Hampshire and Vermont are the holdouts. But saying "48 states have protection acts" is like saying "48 states have speed limits"—technically true, but the details vary wildly.

Court Approval Thresholds: California requires judicial approval for any transfer, period. Minnesota exempts transfers under $15,000 if you meet certain disclosure requirements. Florida has one set of rules for settlements over $50,000 and different rules below that threshold. Check your specific state because companies sometimes "forget" to mention exemptions that would streamline your sale.

Best Interest Standards: Every protection act says judges must find the transfer serves your best interest. What that means depends on where you live. California requires judges to consider 11 specific factors, including whether you got independent advice. Florida gives judges broader discretion. Some states create a presumption that discount rates above certain levels don't serve your interest, making approval harder.

Disclosure Requirements: Most states mandate clear statements about discount rates, total amount being transferred, and net proceeds you'll receive. But formatting requirements differ. Some states require specific font sizes and bold warnings. Others are less prescriptive. Mississippi requires plain-language explanations of how much money you're losing by selling early—using words like "loss" and "cost" rather than softer terms like "discount."

Waiting Periods: That cooling-off period after signing ranges from zero days (some states don't mandate one) to 15 days. During this time window, you can cancel the transfer agreement without penalty or consequence. The company can't keep deposits or charge cancellation fees. Most reputable outfits provide waiting periods even when not legally required, but knowing your state's rule prevents companies from pressuring you to waive rights you didn't know existed.

Attorney Requirements: A handful of states require you to have your own lawyer before transferring payment rights. Even where not mandatory, having an attorney review documents protects you from predatory terms and ensures you understand what you're signing.

Multiple Transfer Restrictions: Some states limit how often you can sell payments. After one transfer, you might need to wait 12 or 24 months before selling additional payments. These restrictions prevent companies from coming back quarterly to chip away at your remaining settlement piece by piece.

Companies operate nationwide but must follow your state's rules. An outfit based in Texas selling to you in California must comply with California law, not Texas law. That creates opportunities for companies to "accidentally" overlook protections you're entitled to if you don't know they exist.

The National Association of Settlement Purchasers maintains state-specific resources, but honestly, their information serves members first and consumers second. Consulting a local attorney who handles structured settlements gives you reliable guidance tailored to your exact situation.

Author: Andrew Halvorsen;

Source: avayabcm.com

Strategic Planning: When Selling Makes Financial Sense

Some circumstances justify eating the huge cost of early access. The trick is distinguishing genuine needs from expensive wishful thinking.

Legitimate reasons include:

Medical procedures insurance won't cover that restore earning capacity or prevent disability progression. If you need spinal surgery that costs $40,000 and will let you return to work earning $50,000 annually, selling payments makes mathematical sense despite the discount rate. You're trading settlement money for earning ability.

Educational expenses that create significant income increases work similarly. Selling three years of payments ($36,000 face value, maybe $24,000 cash received) to finish a nursing degree that doubles your income from $35,000 to $70,000 generates positive return despite the loss.

Business opportunities with demonstrable return potential occasionally warrant consideration—emphasis on "demonstrable." I'm talking real business plans, market research, financial projections, not "my buddy says we should start a food truck." Most businesses fail. You'll still lose your settlement money even if the venture tanks.

Preventing foreclosure or vehicle repossession protects your stability. Losing your home costs more long-term than selling settlement payments, both financially and personally. That said, exhaust every other option first—loan modifications, payment plans, housing assistance programs all beat selling your settlement.

Red flags indicating poor decisions:

Vague purposes. "Catching up on bills" or "getting my finances in order" suggests selling won't solve your underlying problem. If expenses exceed income, a lump sum provides three to six months of breathing room before you're right back where you started.

Discretionary purchases—vacations, vehicle upgrades when your current car works fine, home improvements that are cosmetic rather than necessary. These wants don't justify sacrificing financial security.

Pressure from family or friends. Your settlement exists to support you, not bail out your brother's gambling debts or fund your cousin's MLM scheme. If someone's pushing you to sell, there's a 99% chance the decision serves them, not you.

Very recent settlements. If you agreed to structured payments eight months ago, selling them now indicates you didn't carefully consider whether the structure fit your needs. What changed so drastically that you're willing to lose half the settlement's value?

Author: Andrew Halvorsen;

Source: avayabcm.com

Alternatives to explore first:

Traditional personal loans carry interest rates of 8-18% depending on your credit. That's expensive, but not nearly as expensive as 40% effective annual costs from selling settlement payments. Credit unions typically offer better terms than banks, especially for members with imperfect credit.

Government assistance programs address specific needs without repayment requirements. Programs exist for medical expenses, housing costs, utility payments, and food security. Eligibility varies, but five phone calls might solve your problem without touching your settlement.

Negotiating payment plans with creditors works more often than you'd expect. Medical providers especially will accept reduced payments or extended terms rather than risking non-payment entirely. Hospital billing departments have discretion to write down balances, arrange interest-free payment plans, or connect you with charity care programs.

Family loans complicate relationships but avoid the brutal costs of factoring companies. A written agreement with clear terms protects everyone. Yes, it's awkward. But borrowing $20,000 from family at 5% interest beats selling $35,000 worth of payments to net $20,000 cash.

The permanence of selling demands exhausting every other option first.You can't undo the decision if circumstances change six months later

— Jennifer Martinez

Common Mistakes That Cost Settlement Holders Thousands

Accepting the first offer without shopping around. Discount rates vary by five or more percentage points between companies. That difference translates to $8,000 to $15,000 on a $50,000 face value sale. Contact at least three companies and make them compete for your business. Companies refusing to match competitive offers are telling you their profit margins matter more than your financial outcome.

Selling more payments than necessary. If you need $20,000, don't sell payments worth $32,000 just because the company suggests it or the math works out easier. Every additional payment you sell costs you money—money you won't have later when another need arises. Calculate your exact need, add maybe 10% buffer for unexpected costs, then sell precisely that amount.

Ignoring tax implications for how you'll use the money. Settlement payments themselves remain tax-free whether you receive them on schedule or sell them. But using sale proceeds for business investment or other income-generating activities creates tax situations you need to understand beforehand. Consult a tax professional if you'll use funds for anything beyond immediate consumption expenses.

Failing to read transfer agreements completely. These contracts contain crucial details about what you're selling and what you'll receive. Buried clauses sometimes include additional fees, broader transfer rights than you intended, or terms that contradict the company's verbal promises. Never sign documents you haven't read word-for-word, regardless of pressure to "expedite processing" or "lock in this rate."

Missing scheduled court hearings. Judges dismiss petitions when payees don't appear, forcing you to restart the entire process from scratch. This delay costs weeks or months and sometimes money if the company charges rescheduling fees. Mark the hearing date in multiple places and arrange transportation well in advance. If you absolutely cannot attend, contact the company immediately to reschedule rather than just not showing up.

Skipping independent professional advice. Spending $500 to $1,000 for an attorney or financial advisor to review the transaction feels expensive when you desperately need cash. But that professional might identify problems saving you $5,000 or $10,000, making their fee the best investment you make in the entire process.

Choosing companies based on advertising volume rather than reputation. Heavy advertising indicates marketing budget, not trustworthiness or fair dealing. Check Better Business Bureau ratings, state licensing records, and consumer review sites. Companies with numerous complaints, recent legal problems, or suspiciously perfect 5-star reviews should be avoided regardless of advertised discount rates.

Underestimating future needs. You might desperately need cash today for a specific problem. But selling all your payments leaves nothing for tomorrow's emergencies—and there will be emergencies. Retain at least some future payments to maintain income security, even if it means accepting a higher effective cost to get sufficient immediate cash from a partial sale rather than a full sale.

Frequently Asked Questions About Settlement Liquidity

Structured settlement liquidity options exist, but calling them "options" feels generous when every single path costs you 40-60% of your settlement's value. That's not a service fee or reasonable interest—it's real money disappearing from funds that were supposed to support you for years or decades.

Sometimes life backs you into a corner where losing half your settlement beats the alternative. Terminal illness, disability accommodations, foreclosure prevention, education that substantially increases earnings—these situations occasionally justify the brutal expense. But convenience, impatience, vague financial anxiety, or pressure from others almost never do.

Before contacting any factoring company, exhaust every alternative. Can you get a traditional loan? Negotiate payment plans? Qualify for assistance programs? Borrow from family? Most financial emergencies have solutions that don't involve permanently sacrificing future security.

If those options truly don't exist, approach the sale methodically. Contact at least three companies and make them compete. Sell only the minimum amount needed—not what's convenient, not what gets you the best discount rate, but the actual minimum. Read every document completely. Pay for independent professional advice even though you don't want to spend the money. And use the mandatory court hearing as a reality check—the judge's questions aren't obstacles to overcome, they're prompts for honest self-reflection about whether this irreversible transaction genuinely serves your long-term interests.

State laws requiring court approval exist because people facing financial stress sometimes make terrible decisions their future selves regret bitterly. That judicial review is your last line of defense against expensive mistakes.

Your structured settlement represents financial security—guaranteed, tax-free income requiring zero effort on your part. Treat decisions about accessing that security with appropriate gravity. The money you don't sell continues supporting you automatically. The money you do sell? Gone forever, along with whatever it would've grown to over time.

Choose carefully, because you won't get a second chance.