Structured settlement financial planning desk with calendar, money piles, calculator and budget notebook

How to Build a Structured Settlement Financial Strategy That Works

Content

Getting a structured settlement changes your financial life overnight. The challenge? Your real planning work starts the moment you sign those papers. You're not dealing with one big check you can spend or save immediately—instead, you'll get regular payments stretching out for months, years, maybe even the rest of your life.

What separates people who build wealth from settlement income and those who constantly struggle? Planning. I've seen people receive generous settlements only to watch the money evaporate on everyday bills, leaving them with nothing when emergencies hit or they need to think about retirement.

What Makes Structured Settlements Different from Lump-Sum Payments

When you settle a legal claim through a structured settlement, you're agreeing to receive your compensation as scheduled installments instead of one payment. Most of these agreements come out of personal injury lawsuits, workers' comp cases, or wrongful death claims. The defendant or their insurer buys an annuity that guarantees your income according to whatever schedule was negotiated.

Your payment structure depends entirely on what you negotiated. Maybe you'll get $2,500 every month for the next 20 years. Perhaps it's $8,000 quarterly for a decade. Some people negotiate increasing amounts—starting at $3,000 monthly, jumping to $4,500 after five years, then $6,000 after ten. Others combine everything: a $50,000 payment upfront, monthly payments for 15 years, then a balloon payment of $100,000 at year 20.

Compare that to taking a lump sum. You walk away with the full amount immediately. Want to invest it? Go ahead. Need to spend it? Your call. But you're also stuck with the responsibility of making that money stretch as long as you need it—something that overwhelms most people who've never managed six or seven figures before.

Structured settlements take away some of that pressure by spreading your money across time. The flip side? You sacrifice flexibility. Can't access those future payments without selling them—usually for 40-60 cents on the dollar. That's why planning becomes absolutely critical. You're building your entire financial life around income you receive on a fixed schedule you can't easily modify.

Author: Danielle Morgan;

Source: avayabcm.com

Here's what makes it trickier: most people earn variable income from their jobs. Work extra hours, get a raise, take a second job—you can boost your income when needed. Settlement payments arrive on schedule regardless of whether you need more money or less. Your budget has to work around that reality, not the other way around.

Core Components of a Settlement Income Financial Strategy

You need to understand several foundational pieces before building any comprehensive plan for your settlement income.

Understanding Your Payment Schedule and Terms

Your settlement paperwork spells out everything: how much you get, when you get it, for how long, and whether amounts change over time. These details control every financial decision you'll make going forward.

Take stepped payments, for example. Your agreement might say you'll receive $1,800 monthly for the first seven years, which then increases to $2,700 monthly for years eight through fifteen, with a final increase to $3,500 monthly from year sixteen until payment ends at year 25. Other settlements keep payments level throughout—same amount, same schedule, beginning to end. A handful include special lump sums at certain anniversaries while maintaining regular payments.

Read through your agreement looking for special provisions. Some include extra payments triggered by specific events—$25,000 when your child starts college, for instance. Others build in annual cost-of-living bumps tied to the Consumer Price Index. Knowing these details prevents surprises and lets you plan accurately for the long term.

Payment duration matters enormously. Are you getting payments for 15 years or for life? With a finite timeline, you'll need plans for income after your settlement ends. With lifetime payments, you can build a permanent budget around that income (though you'll still need beneficiary planning and estate strategies).

Tax Advantages and Reporting Requirements

Here's where structured settlements shine. Federal tax law (specifically IRC Section 104(a)(2)) exempts payments from physical injury or sickness settlements from income tax. You don't pay tax on the principal or on any growth happening inside the annuity that funds your settlement.

That tax break is huge. If $3,000 arrives in your account each month tax-free, it's equivalent to earning roughly $4,200-$4,500 in taxable income (depending on which tax bracket you'd fall into). Factor this difference into any decisions about working versus living on settlement income alone, or when comparing settlement returns to other investments.

Not every settlement qualifies, though. Did you settle an employment discrimination case? That's taxable. Emotional distress claim without physical injury? Also taxable. Punitive damages? Yep, taxable. Your attorney fees might have tax implications too, depending on how everything was structured.

Tax-exempt settlement payments don't need reporting on your return, but keep documentation about where the money came from. If the IRS comes asking questions, you'll need proof. Settlements with taxable portions will generate tax forms (like 1099-MISC), and you'll report those normally.

Author: Danielle Morgan;

Source: avayabcm.com

Inflation Protection Considerations

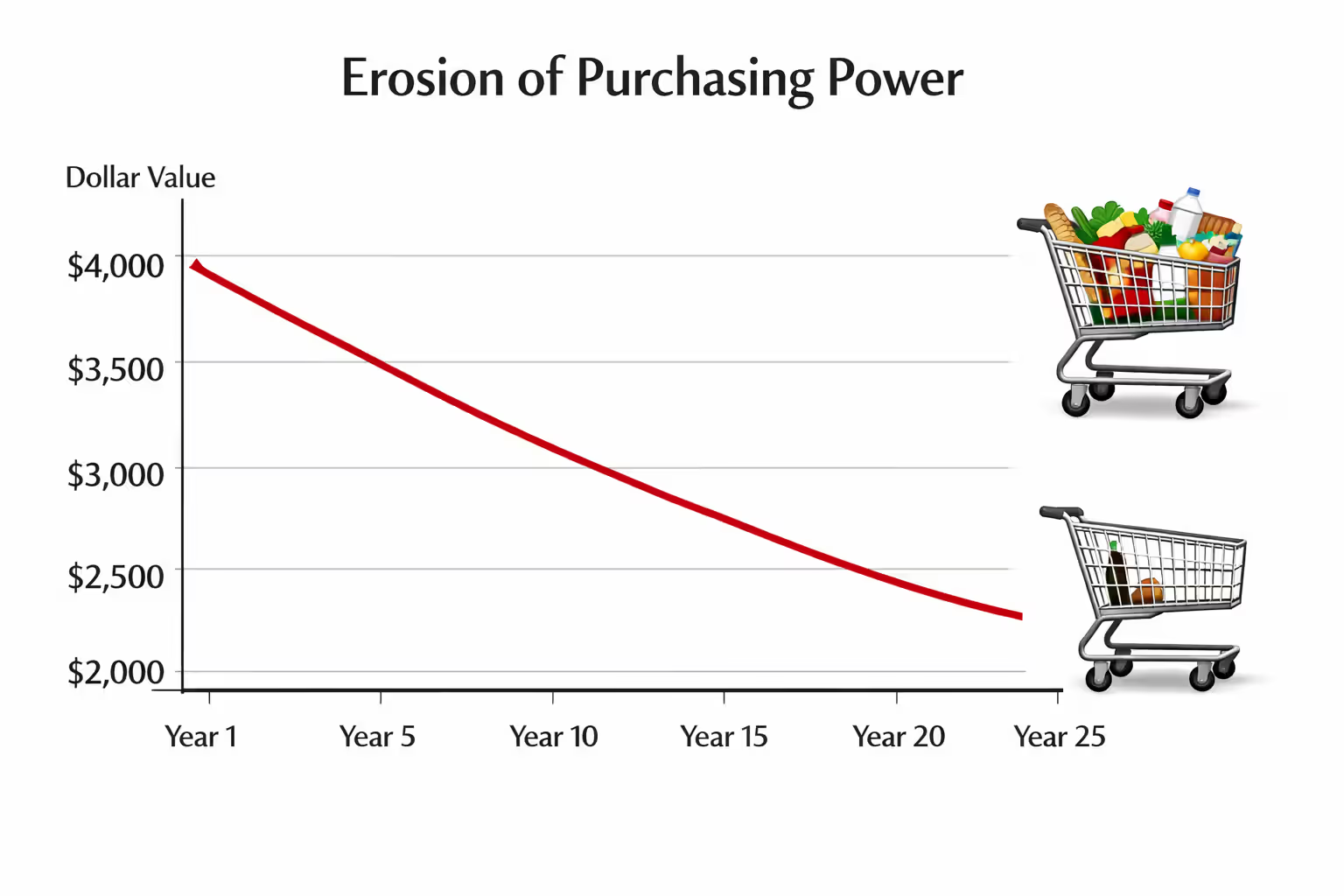

Each dollar you receive today buys more than a dollar arriving ten years from now. With typical inflation around 3% yearly, your purchasing power gets cut roughly in half every 24 years. That $2,000 monthly payment covering your needs today? In 20 years, it'll feel more like $1,100 in today's purchasing power.

Some settlement agreements build in inflation protection through annual cost-of-living adjustments. These provisions bump your payments up each year based on an inflation index—usually the CPI. A settlement with 3% annual increases maintains real purchasing power far better than flat payments.

Many settlements offer flat payments with zero inflation adjustment, though. If that's your situation, you must plan around eroding purchasing power. You might need to live well below your means initially while building reserves, or develop additional income streams that supplement settlement payments as their real value declines over time.

I see the same mistake constantly—people build their lifestyle around that initial payment without considering what inflation does over time. Someone getting $4,000 monthly thinks they're financially set forever. Fast forward 15-20 years when that $4,000 buys what $2,500 buys today, and they're suddenly struggling to cover basic expenses

— Rebecca Martinez

Five Common Budgeting Mistakes Settlement Recipients Make

Learning from others' mistakes helps you sidestep these common problems.

Mistake #1: Inflating lifestyle the moment payments start. That first payment arrives, and people immediately upgrade everything—bigger apartment, newer car, better everything. Within months, they've committed to expenses consuming nearly every payment. Zero margin remains for emergencies, savings, or dealing with inflation. When unexpected costs hit, they're stuck.

Mistake #2: Treating today's payment value as permanent. Recipients with level payments budget as though each payment will always cover the same expenses. They lock into fixed commitments—mortgages, car notes, subscriptions—eating up most of each payment. No room remains when utility bills rise, groceries cost more, or insurance premiums increase. Within five years, they're squeezed.

Mistake #3: Ignoring how settlement income interacts with other money sources. Your settlement doesn't exist in a vacuum. Maybe you're still working. Perhaps you collect Social Security benefits. Some people don't realize settlement income might affect means-tested programs like Medicaid or SSI eligibility. Others miss opportunities to optimize taxes across multiple income sources, leaving money on the table.

Mistake #4: Skipping emergency savings entirely. Working a regular job? You could grab overtime, ask for a raise, or pick up side work when unexpected bills arrive. Settlement payments arrive on schedule whether you need extra money or not. Without emergency reserves, recipients face impossible choices when the transmission fails or the ER sends a $4,000 bill—often leading them toward expensive debt or predatory settlement-buying schemes.

Mistake #5: Forgetting about beneficiaries. Most settlement annuities include provisions for beneficiaries if you die before receiving all payments. Yet people neglect designating beneficiaries, forget to update them after divorce or remarriage, or never coordinate settlement beneficiary planning with their broader estate plan. That oversight creates expensive headaches for their heirs.

How to Build a Structured Settlement Budgeting Strategy That Works

Creating a budget for settlement income means adapting traditional methods to work with periodic payment schedules and settlement-specific characteristics.

Mapping Payments to Essential vs. Discretionary Expenses

Start by splitting every expense into two buckets: essential or discretionary. Essentials include your rent or mortgage, utilities, groceries, insurance premiums, required debt payments, and healthcare costs—things you can't eliminate easily. Discretionary covers entertainment, restaurant meals, hobbies, upgrades, and lifestyle expenses that make life enjoyable but aren't strictly required for survival.

Calculate monthly essential expenses even if payments arrive on different schedules. Let's say essentials total $3,200 monthly and you get $10,000 quarterly. You need $9,600 from each quarterly payment covering three months of essentials, leaving just $1,400 for discretionary spending, savings, and everything else.

This exercise shows whether your payment timing matches your spending reality. Monthly payments naturally align with how most people spend money. Quarterly or annual payments demand more active cash-flow management—you must set aside money from each payment to cover expenses between now and your next payment.

Here's a useful guideline: keep essential expenses below 70% of settlement income. That leaves breathing room for savings, fun money, and inevitable expense increases over the years.

Creating Emergency Reserves Between Payment Periods

Everyone needs emergency funds. Settlement recipients need them even more. You can't pick up extra work hours or access future payments without selling them at massive discounts, so reserves provide your only cushion against financial shocks.

Build an emergency fund covering three to six months of essential expenses. Got $3,000 monthly in essentials? You need $9,000-$18,000 in reserves. Build this fund before increasing discretionary spending, even if it takes over a year of directing most payments toward savings.

Your timeline depends on payment size and frequency. Someone receiving $5,000 monthly might sock away $2,000 per month, hitting a $12,000 fund in six months. Someone getting $15,000 quarterly might dedicate $5,000 from each payment, building the same fund over 18 months.

Once you've built it, maintain it. If you pull from emergency savings, replace that money before resuming normal spending. This discipline ensures you'll always have a buffer available, even after tapping reserves for unexpected costs.

Author: Danielle Morgan;

Source: avayabcm.com

Coordinating Settlement Income with Employment or Benefits

Plenty of settlement recipients keep working, at least initially. Others collect Social Security disability, SSI, or similar benefits. Smart planning requires understanding how these income sources fit together.

For workers, settlement income creates opportunities to scale back hours, pursue less stressful work, or aggressively build retirement savings. Someone earning $40,000 annually who receives $30,000 in yearly settlement payments might drop to part-time work, improving their quality of life while maintaining roughly the same total income.

Benefits recipients face trickier situations. Tax-free structured settlement payments from physical injury claims typically don't affect Social Security Disability Insurance (SSDI) eligibility, but they can impact means-tested programs like SSI or Medicaid. These programs impose strict income and asset limits—settlement payments might push you over the threshold.

Before accepting a settlement, consult a benefits specialist if you receive means-tested benefits. Special needs trusts or other planning strategies might preserve eligibility while still delivering financial security. Don't assume settlement income automatically gets exempted—rules vary by program and state.

| Payment Frequency | Essential Expenses | Emergency Fund | Discretionary | Savings/Investment |

| Monthly ($3,000) | 60-70% ($1,800-2,100) | 10-15% ($300-450) | 10-15% ($300-450) | 10-15% ($300-450) |

| Quarterly ($9,000) | 60-70% ($5,400-6,300) | 10-15% ($900-1,350) | 10-15% ($900-1,350) | 10-15% ($900-1,350) |

| Annual ($36,000) | 60-70% ($21,600-25,200) | 10-15% ($3,600-5,400) | 10-15% ($3,600-5,400) | 10-15% ($3,600-5,400) |

Monthly Budget Template for Structured Settlement Recipients

This template shows recommended allocation percentages for different payment schedules. Adjust percentages based on your situation—someone with paid-off housing might allocate less to essentials, while someone with ongoing medical costs might need more. The goal is balancing current needs, emergency protection, and future planning.

Settlement Annuity Financial Management: Investment and Growth Options

You can't modify, redirect, or access the structured settlement annuity itself without selling payment rights. However, once payments hit your bank account, you've got substantial opportunities for growing that money.

Each payment becomes spendable cash you can allocate toward spending, saving, or investing according to your goals. The tax-free nature of qualified settlement payments gives you an edge—you're investing the full amount rather than what's left after taxes, providing more capital to work with.

Most settlement recipients should stick with conservative investment approaches. Since settlement payments already provide steady income, you don't need risky investments chasing high returns. Focus on preserving capital and achieving moderate growth.

High-yield savings accounts or money market funds work well for emergency reserves and short-term goals. These accounts offer liquidity—access funds quickly when needed—while earning reasonable interest. Right now, many online banks pay 4-5% annually on savings, though rates fluctuate with economic conditions.

For longer-term objectives, consider diversified investment accounts. Low-cost index funds provide exposure to stock and bond markets without requiring expertise in selecting individual securities. A balanced portfolio might hold 60% in stock index funds and 40% in bond index funds, delivering growth potential with moderate risk.

Tax-advantaged retirement accounts deserve attention. Even though settlement payments arrive tax-free, you can still contribute to IRAs or 401(k)s if you've got earned income from employment. Maximizing these contributions makes sense for most recipients—additional tax benefits plus building retirement security beyond settlement payments.

Some recipients purchase additional annuities with their settlement payments, essentially creating their own structured income stream. This strategy works well if you want guaranteed lifetime income but your settlement payments end after a set period. You're converting finite payments into perpetual income, though you sacrifice flexibility and liquidity.

Working with a fee-only financial advisor—one charging flat fees for advice rather than earning commissions from product sales—helps ensure recommendations serve your interests. Look for advisors experienced with structured settlements or personal injury financial planning, since they'll understand the unique considerations involved.

When to Consider Modifying Your Structured Settlement Plan

Life changes, and a settlement structure making perfect sense initially might not fit your current situation. Understanding when modification makes sense—and when it doesn't—protects you from expensive mistakes.

Major life events often trigger reassessment. Getting married, divorcing, having children, or losing a spouse all shift financial needs and priorities. A health crisis requiring immediate treatment funds might justify accessing future payments. Job loss eliminating other income could create urgent need for increasing settlement income if possible.

Author: Danielle Morgan;

Source: avayabcm.com

Here's the problem: you can't modify the underlying annuity contract. The payment schedule was locked in when the settlement was finalized, and the insurance company funding the annuity won't renegotiate terms. Your only option for accessing future payments early involves selling payment rights to a third party—called a structured settlement transfer or factored sale.

These transactions cost you significantly. Buyers purchase future payments at steep discounts, often paying just 50-70 cents per future dollar. Selling $50,000 in future payments might net you only $30,000-35,000 today. The discount covers time-value-of-money calculations, transaction costs, and the buyer's profit.

Courts must approve structured settlement transfers in most states, offering some consumer protection. The judge reviews whether the transfer serves your best interest and whether the discount seems reasonable given circumstances. This approval process takes time—typically 45-90 days—so transfers don't provide instant access to funds.

Partial sales offer middle ground. Rather than selling all future payments, maybe you sell just two years of payments or every other payment for five years. This approach provides needed funds while preserving some long-term settlement income. The discount still applies, but you maintain financial security going forward.

Before pursuing any transfer, exhaust other options first. Can you cut expenses, find additional income sources, or secure a conventional loan? These alternatives usually cost less than selling settlement payments at massive discounts. Reserve transfers for genuine emergencies or opportunities with clear financial benefits—launching a business, buying a home, or funding education that demonstrably increases earning potential.

Be extremely wary of companies aggressively marketing settlement purchases. Some use predatory tactics, pressuring recipients into terrible deals. Never accept the first offer. Consult an attorney or financial advisor before signing anything. The National Association of Settlement Purchasers maintains standards for ethical practices—verify any company's reputation thoroughly before engaging.

Frequently Asked Questions About Structured Settlement Financial Planning

Managing structured settlement income successfully requires adapting traditional money management strategies to work with periodic payment schedules and the unique characteristics of settlement income. The guaranteed nature of payments provides security you can rely on, but the inflexibility demands careful planning ensuring those payments support your financial goals throughout their entire duration.

Success starts with thoroughly understanding your specific settlement terms—payment amounts, timing, duration, and any special provisions built into your agreement. Build a realistic budget accounting for essential expenses, emergency reserves, and long-term savings while leaving room for discretionary spending that makes life worth living. Consider inflation's erosive impact, particularly if your payments don't include cost-of-living adjustments.

Sidestep common mistakes like immediately inflating lifestyle to match payment amounts, neglecting emergency savings, or failing to coordinate settlement income with other financial resources. Once you receive payments, invest them strategically to build wealth beyond the settlement itself, taking advantage of the tax-free nature of qualified settlement payments.

Resist selling future payments except in genuine emergencies or for clear financial opportunities with obvious long-term benefits. The substantial discount involved in these transactions makes them extremely expensive ways to access funds, and you'll sacrifice long-term security for short-term cash.

Professional guidance from experienced financial planners, tax advisors, and attorneys helps navigate the complexities of settlement income planning. The cost of professional advice typically pales compared to the value of avoiding mistakes or optimizing your financial strategy.

With thoughtful planning and disciplined execution, structured settlement payments can deliver lasting financial security, supporting your goals and needs for years or decades ahead. The key lies in treating settlement income not as windfall money to spend freely, but as a valuable financial resource requiring careful, intentional stewardship.