Cracked glass shield on insurance documents symbolizing structured settlement credit risk over decades

Structured Settlement Credit Risk and Insurer Stability Guide

Content

Here's something most personal injury lawyers won't tell you upfront: when you sign that structured settlement agreement, you're betting your financial future on an insurance company staying solvent for the next 20, 30, maybe 50 years. Think about that. A 35-year-old accepting monthly payments until retirement is trusting a single corporation to survive half a century of economic chaos, management changes, and market disruptions.

Most people spend weeks researching which car to buy—a $30,000 decision they'll replace in a decade. Yet they'll sign off on a multi-million-dollar annuity after a 20-minute explanation from a settlement planner they just met.

Remember 2008? AIG needed $182 billion in taxpayer money to avoid complete collapse. Sure, their structured settlement division ultimately survived, but for several terrifying months, nobody knew if payment checks would keep arriving. That wake-up call showed how quickly "too big to fail" becomes "currently failing." Evaluating structured settlement credit risk isn't being paranoid. It's basic financial self-defense.

What Credit Risk Means for Your Structured Settlement Payments

Let's strip away the technical jargon. Credit risk means: "What's the chance this insurance company goes belly-up before they've finished paying me?"

Unlike your auto insurance—where State Farm processes your fender-bender claim and you're done—structured settlements obligate the insurer to make payments potentially for decades. They set aside reserves today, invest that money, and use investment returns to fund your future checks. If they miscalculate returns, make terrible investment choices, or face unexpected claim surges, those reserves evaporate.

The Role of Life Insurance Companies in Settlement Annuities

Why life insurers? Because they're already in the business of making payments that stretch across decades. When someone buys whole life insurance at 30 and dies at 85, the insurer's been managing that liability for 55 years. They've built systems for long-term reserve management, asset-liability matching, and mortality projections.

Author: Danielle Morgan;

Source: avayabcm.com

Here's how the money flows: The defendant in your injury lawsuit doesn't hand you an annuity directly. Instead, they purchase what's called a "qualified assignment" from a specialty assignment company. That assignment company then purchases an annuity from a life insurance carrier. This carrier—the one you've probably never heard of until settlement day—becomes responsible for cutting your checks every month.

Notice the problem? You didn't pick this insurance company. You might not even get a meaningful vote. The defendant's liability carrier and the assignment company choose the annuity issuer, and they're heavily incentivized to pick the cheapest option. A carrier offering annuities 0.3% cheaper wins the business, even if their financial strength ratings lag competitors. That 0.3% saves the defendant $6,000 on a $2 million settlement but potentially exposes you to an insurer with shakier finances.

New York and California require minimum credit ratings for settlement annuity issuers. Most states don't. Even where requirements exist, the bar sits surprisingly low—often "adequate" rather than "excellent." You could end up with an A- rated carrier when A++ options exist, simply because nobody insisted on better.

Why Insurer Solvency Matters for 30+ Year Payment Streams

Consider the difference between insurance products. If your homeowner's insurance company fails midway through your policy term, you buy replacement coverage. Annoying, maybe more expensive due to market changes, but doable.

Structured settlements don't work that way. If your annuity issuer collapses in year 15 of a 30-year payout, you can't just transfer your payment rights to another carrier. Those contractual obligations are locked to the failed company. You're stuck navigating state guaranty association claims, potential payment reductions, and years of uncertainty.

Executive Life Insurance Company collapsed in 1991, then the largest life insurer failure in American history. Policyholders eventually received most benefits through guaranty associations and court-supervised asset sales. "Eventually" meant years of litigation. "Most benefits" meant some people with large annuities exceeded guaranty fund limits and lost money permanently.

The math gets ugly fast with long-duration obligations. An insurer projecting 6% annual investment returns sets reserves accordingly. If actual returns average 4.5%—entirely possible during prolonged low-rate environments—the funding shortfall compounds annually. By year 15, reserves might be 20% inadequate. By year 20, the company's insolvent.

The Four Major Rating Agencies That Evaluate Settlement Annuity Insurers

Four organizations dominate insurance company credit analysis: A.M. Best, Standard & Poor's, Moody's, and Fitch Ratings. Each uses proprietary methodologies examining capital adequacy, operating performance, business profile, and enterprise risk management. They're like Yelp reviews for billion-dollar corporations—imperfect, occasionally wrong, but the best tools available.

Author: Danielle Morgan;

Source: avayabcm.com

A.M. Best Company's Rating Scale and Methodology

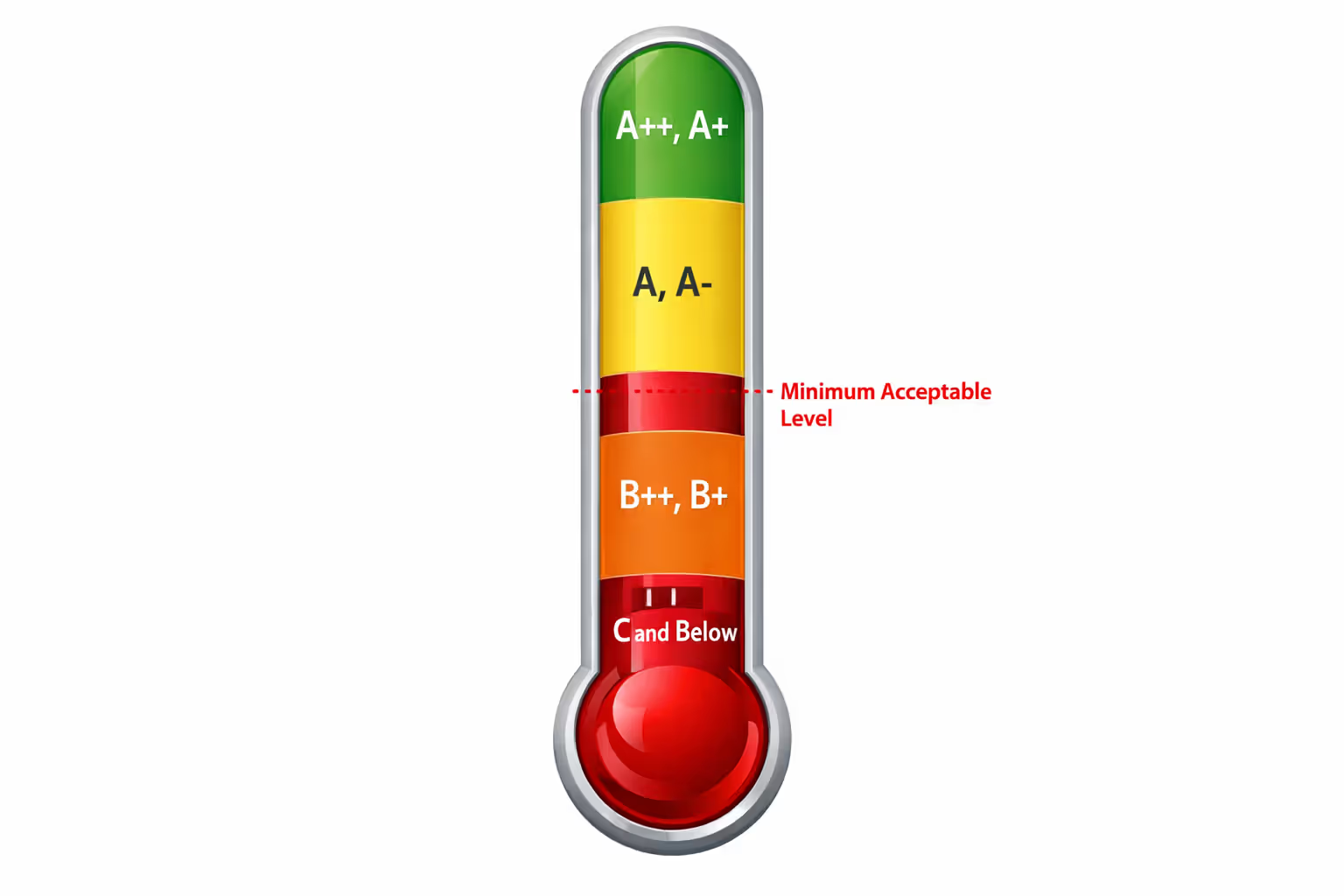

A.M. Best stands apart because they rate only insurance companies. While S&P and Moody's assess everything from sovereign nations to corporate bonds, A.M. Best focuses exclusively on insurers. Their Financial Strength Ratings span 16 levels from A++ (Superior) down to F (In Liquidation).

They analyze five core areas: balance sheet strength, operating performance, business profile, enterprise risk management, and management quality. For life insurers backing structured settlements, they scrutinize reserve adequacy with particular intensity. Are reserves sufficient assuming various interest rate scenarios? What happens if mortality assumptions prove overly optimistic? How concentrated are the insurer's investments—could a single sector collapse crater their portfolio?

An insurer earning A++ demonstrates exceptional balance sheet strength and operating performance. They maintain capital levels significantly above regulatory minimums, generate consistent underwriting profits, and show sophisticated risk management. Drop down to B++ or B+, and you're looking at "good" financial strength—adequate under normal economic conditions but potentially vulnerable during stress.

For structured settlement purposes, accepting anything below A- introduces meaningful risk you shouldn't tolerate.

Standard & Poor's, Moody's, and Fitch Ratings Criteria

These three agencies bring broader perspective, applying methodologies developed for banks, corporations, and government debt to insurance companies. S&P's scale runs from AAA (Extremely Strong) through AA, A, BBB, down to R (Regulatory Action), with plus/minus modifiers. Moody's uses Aaa, Aa, A, Baa through C. Fitch mirrors S&P's approach.

They weigh competitive positioning heavily. An insurer with adequate capital but shrinking market share might earn a "negative outlook"—analyst-speak for "we're watching closely and might downgrade soon." Management strategy matters enormously. Insurers pursuing aggressive growth through premium undercutting raise red flags even if current finances look solid.

Moody's particularly emphasizes liquidity and asset quality. During 2008, carriers holding residential mortgage-backed securities faced brutal downgrades as those assets lost 40-60% of value virtually overnight. Fitch runs extensive stress testing, modeling insurer performance during severe recessions, interest rate spikes, or market crashes.

How to Read and Compare Different Rating Systems

You can't directly equate ratings across agencies. A.M. Best's A+ doesn't equal S&P's A+—they represent different risk levels on different scales. This table translates between rating systems:

| A.M. Best Rating | S&P | Moody's | Fitch | Interpreted Risk Level |

| A++, A+ | AAA | Aaa | AAA | Superior financial security with exceptional capital cushion |

| A | AA+, AA, AA- | Aa1, Aa2, Aa3 | AA+, AA, AA- | Excellent financial strength with very strong fundamentals |

| A- | A+ | A1 | A+ | Strong to excellent creditworthiness |

| B++, B+ | A, A- | A2, A3 | A, A- | Good financial security, adequate under normal conditions |

| B | BBB+, BBB | Baa1, Baa2 | BBB+, BBB | Fair financial security with moderate vulnerability |

| B- | BBB- | Baa3 | BBB- | Fair financial security showing some weakness |

| C++, C+ | BB+, BB, BB- | Ba1, Ba2, Ba3 | BB+, BB, BB- | Marginal security, vulnerable to economic stress |

| C, C- | B+, B, B- | B1, B2, B3 | B+, B, B- | Weak security, highly vulnerable to default |

| D | CCC and below | Caa and below | CCC and below | Poor security, extremely vulnerable or defaulting |

| E, F | R, SD, D | Ca, C | DDD, DD, D | Under regulatory supervision or liquidation |

For settlement annuities, insist on carriers rated A or higher from A.M. Best, or AA- and above from S&P/Fitch, or Aa3+ from Moody's. These thresholds provide meaningful security margins without limiting you to only the top three insurers in America.

Red Flags: Warning Signs of Insurer Financial Weakness

Credit ratings capture today's snapshot, but trajectory matters more. An insurer currently rated A who was A++ three years ago and AA+ five years ago? That's a fire alarm. They're hemorrhaging financial strength. Conversely, a carrier upgraded from A- to A over the past two years shows improving fundamentals.

Any rating below A- from A.M. Best (or equivalent) means elevated risk. At B++ or B+, agencies are essentially saying "probably fine under normal circumstances." Structured settlements don't care about normal circumstances. They need certainty across recessions, market crashes, and industry disruptions spanning decades.

Watch for "negative outlook" designations or "under review for downgrade" warnings. These signal deteriorating metrics that could trigger rating cuts within 12-24 months. An insurer on negative watch today might fall below acceptable thresholds before your settlement paperwork finalizes.

Rapid growth sometimes masks danger. An insurer aggressively pursuing market share might underprice annuities to win business, setting inadequate reserves. Metropolitan Life and Prudential dominate the settlement annuity market specifically because they grow steadily while maintaining pricing discipline. The upstart offering quotes 2% cheaper than MetLife might be setting themselves up for insolvency in 15 years.

State guaranty associations function as safety nets, but they're nets with enormous holes. Coverage limits typically range from $250,000 to $500,000 per person, varying by state. If your structured settlement pays $400,000 annually over 20 years (present value maybe $5 million), guaranty funds cover a small fraction. Worse, guaranty payments may take years to begin after insurer failure, creating cash flow crises if you depend on settlement income for medical care or living expenses.

Look at historical failures for perspective. Executive Life's 1991 implosion resulted from excessive junk bond exposure—the insurer chased higher yields by buying risky corporate debt that defaulted during recession. Conseco's 2002 bankruptcy demonstrated how even large, established carriers face solvency crises. While Conseco eventually restructured rather than liquidating, policyholders endured years of uncertainty.

Author: Danielle Morgan;

Source: avayabcm.com

How to Research and Verify Your Settlement Issuer's Reliability

Checking insurer ratings takes 10 minutes and costs nothing. Before signing settlement documents, verify the proposed annuity issuer's current ratings from multiple agencies.

Start at A.M. Best's website, which provides limited free rating information. Enter the insurance company's complete legal name—marketing names won't work. Ratings apply to specific legal entities. New York Life Insurance Company carries different ratings than New York Life Insurance and Annuity Corporation, despite both being owned by New York Life.

Standard & Poor's (standardandpoors.com), Moody's (moodys.com), and Fitch (fitchratings.com) similarly offer free current rating access. Check all four agencies. Significant discrepancies between them warrant investigation. If A.M. Best rates a carrier A+ but Moody's assigns Baa2 (roughly equivalent to B+ on A.M. Best's scale), these agencies see very different risk profiles.

State insurance department websites list all licensed insurers and sometimes publish financial data. The National Association of Insurance Commissioners (NAIC) maintains detailed financial statements for every licensed insurer, accessible through state regulators. These filings are technical—pages of balance sheets and actuarial calculations—but reveal capital levels, investment portfolio composition, and reserve adequacy.

Your attorney is ethically obligated to protect your interests, including annuity issuer selection. Ask directly: "What's the proposed insurer's current A.M. Best rating? Have they maintained this rating for at least five consecutive years? What alternatives exist with higher ratings?" Don't accept vague reassurances.

Settlement consultants who work independently—meaning they advise injury victims rather than defendants—provide valuable unbiased guidance. Unlike consultants employed by insurance companies, plaintiff consultants have no financial incentive to steer you toward particular carriers.

I've analyzed over 3,000 structured settlements during my career, and I can tell you the most common mistake costs people millions in aggregate. They accept the first annuity proposal without questioning the insurer's credit strength. Defendants naturally prefer the cheapest option available, which often means choosing lower-rated carriers. But here's what surprises people: simply asking 'Can we use a higher-rated insurer instead?' frequently works. Defendants agree without pushback because they assumed the plaintiff wouldn't notice or care about the difference. That five-minute conversation—insisting on A+ or A++ rated carriers—might increase settlement cost by 2-3%, which is trivial compared to decades of enhanced payment security. I've seen catastrophic situations where an insurer failed twenty years into a thirty-year payment stream. The beneficiary lost hundreds of thousands of dollars beyond guaranty fund limits. That disaster was 100% preventable by insisting on stronger carriers upfront when the settlement was still negotiable

— Jennifer Morrison

Demand rating documentation in writing. Verbal assurances mean nothing legally. Get rating confirmation letters directly from agencies or recent rating reports showing current status and outlook. If anyone resists providing this documentation, that resistance itself is a red flag.

Strategies to Minimize Credit Risk in Structured Settlements

Proactive protection during settlement negotiations beats reactive scrambling after problems emerge. Once you've signed settlement documents specifying an annuity issuer, changing carriers becomes virtually impossible without defendant cooperation—which you won't get.

First strategy: Require minimum rating thresholds directly in settlement agreements. Specify that the annuity issuer must maintain an A.M. Best rating of A+ or higher (or equivalent) at the time of annuity purchase. Include language requiring carrier substitution if the proposed insurer's rating falls below this threshold between settlement signing and funding.

Some sophisticated settlement agreements include ongoing monitoring provisions. If the issuer's rating drops below specified levels after funding, the defendant must provide additional security or the claimant gains specific rights (like ability to sell the payment stream without court approval). Defendants resist such terms, but they're negotiable in settlements exceeding $2 million where credit risk materially impacts present value.

Second strategy: Portfolio diversification across multiple highly-rated insurers reduces concentration risk dramatically. Rather than a single $3 million annuity from one carrier, structure the settlement as three separate $1 million annuities from different A++ rated insurers. This approach costs slightly more—carriers offer volume discounts—but eliminates single-point-of-failure risk.

Author: Danielle Morgan;

Source: avayabcm.com

Diversification works best for larger settlements with multiple payment streams. A settlement providing both monthly living expenses and annual lump sums for future medical procedures can assign each component to different insurers. If one carrier fails, guaranty associations may cover some payments while other streams continue uninterrupted from solvent carriers.

Third strategy: Understand state guaranty fund protections realistically—they're last-resort safety nets, not comprehensive protection. Don't rely on them as primary security.

| State | Maximum Life Insurance Coverage | Maximum Annuity Coverage |

| California | $300,000 | $300,000 |

| Texas | $300,000 | $250,000 |

| Florida | $300,000 | $300,000 |

| New York | $500,000 | $500,000 |

| Pennsylvania | $300,000 | $300,000 |

| Illinois | $300,000 | $300,000 |

| Ohio | $300,000 | $300,000 |

| Georgia | $300,000 | $300,000 |

| North Carolina | $300,000 | $300,000 |

| Michigan | $300,000 | $300,000 |

Important caveat: These limits apply per individual per insurer, not per policy. If you hold multiple annuities from the same failed insurer totaling $600,000 in present value, you only receive your state's maximum (often $300,000). You lose the excess permanently.

Also critical: Guaranty funds cover present value, not nominal future payments. A structured settlement promising $500,000 in payments over 20 years might have present value of only $350,000, which is what guaranty associations would protect.

Guaranty fund payments take time—often years. State regulators must liquidate failed insurer assets, determine valid claims, calculate present values, and process payments. During this period, you receive nothing, creating severe financial hardship if you depend on settlement income for housing, medical care, or daily living expenses.

FAQ: Structured Settlement Insurer Credit Risk

Structured settlement credit risk deserves the same intensive scrutiny you'd apply to any multi-million-dollar financial decision affecting your family's security for decades. The annuity issuer you accept today must remain financially viable through economic recessions, industry disruptions, management turnovers, and regulatory changes spanning potentially 30-50 years.

Rating agencies provide essential evaluation tools, but ratings alone don't eliminate risk—they quantify and compare it. Combine strong ratings (A+ or higher from A.M. Best) with portfolio diversification across multiple insurers when settlement size permits. Negotiate minimum rating requirements and substitution provisions into settlement agreements before signing anything. Understand realistically that state guaranty associations offer limited backup protection, not comprehensive insurance replacing failed insurer obligations.

The ten minutes spent researching proposed insurers and requesting higher-rated alternatives can prevent financial catastrophe. Defendants often accept requests for better-rated issuers without resistance, particularly when you present specific rating comparisons showing material differences. Your attorney and settlement consultant should aggressively advocate for credit quality, but ultimate responsibility rests with you—it's your financial future.

A structured settlement represents a contractual obligation potentially spanning 50+ years. The insurance company behind that contract deserves at least as much evaluation as the payment schedule itself. Choose wisely and carefully, because unlike virtually every other financial decision you'll make, this one cannot be reversed, modified, or corrected later.