Desk with legal settlement documents, financial charts, calculator, pen, glasses, and scales of justice in background

Structured Settlement Annuity Taxation Guide to Tax-Free Payments

Content

Receiving a structured settlement annuity can provide financial security for years or decades. But many recipients worry about how much they'll lose to taxes. The good news: most structured settlement payments from personal injury cases are completely tax-free. The bad news: seemingly small mistakes in how your settlement is structured can turn that tax-free income into a taxable nightmare.

Understanding which settlement payments escape taxation—and which don't—makes the difference between keeping your full award and handing a chunk to the IRS every year.

How the IRS Treats Structured Settlement Annuities

The foundation of structured settlement annuity tax treatment rests on Internal Revenue Code Section 104(a)(2). This provision excludes from gross income "the amount of any damages (other than punitive damages) received (whether by suit or agreement and whether as lump sums or as periodic payments) on account of personal physical injuries or physical sickness."

That language matters enormously. Congress revised Section 104(a)(2) in 1996 to add the word "physical" before injuries and sickness. Before that change, settlements for non-physical injuries like employment discrimination or emotional distress qualified for tax-free treatment. After 1996, only settlements compensating actual physical harm receive favorable tax treatment.

A qualified structured settlement involves a defendant (or their insurer) transferring the obligation to make periodic payments to a third-party assignment company. That company purchases an annuity from a highly-rated life insurance company, which then makes payments directly to you. When properly structured, the entire arrangement qualifies for tax exclusion under Section 104(a)(2) and Section 130 (qualified assignments).

Non-qualified structured settlements—typically those funding non-physical injury claims—don't receive the same treatment. The principal may be tax-free (you already paid tax on the underlying claim), but any interest or investment growth becomes taxable income.

Physical Injury vs. Non-Physical Injury Claims

The physical injury distinction creates a bright line in the tax code. A car accident that causes whiplash, a slip-and-fall resulting in a broken bone, or a surgical error leading to nerve damage all qualify as physical injuries. Settlements compensating these harms escape federal income tax entirely—both the principal and any growth from the annuity.

Employment discrimination, defamation, or emotional distress claims without a physical injury component don't qualify. Even if your employer's harassment caused diagnosed anxiety and depression, without an accompanying physical manifestation (like stress-induced ulcers documented as a physical ailment), the IRS treats the settlement as taxable income.

Here's where it gets tricky: emotional distress damages attributable to a physical injury receive tax-free treatment. If you developed PTSD after a physical assault, and your settlement compensates both the assault injuries and the resulting emotional trauma, the entire amount qualifies for exclusion. But standalone emotional distress claims remain taxable.

Medical expenses present another nuance. If you previously deducted medical expenses on your tax return and later receive a settlement reimbursing those expenses, you must include the reimbursement as income to the extent you received a tax benefit from the deduction. This prevents double-dipping.

Author: Danielle Morgan;

Source: avayabcm.com

When Interest and Investment Gains Become Taxable

A properly structured settlement annuity grows tax-free inside the annuity contract. The insurance company invests your funds, and that growth compounds without annual tax reporting. This mirrors the tax treatment of the underlying settlement—if the principal is tax-free under Section 104(a)(2), the growth remains tax-free too.

But taking a lump sum and investing it yourself changes everything. Suppose you receive $500,000 for a personal injury and deposit it in a brokerage account. The settlement itself isn't taxable, but every dividend, interest payment, and capital gain from your investments becomes taxable income. The Section 104(a)(2) exclusion doesn't extend to post-settlement investment returns you generate.

This creates a powerful incentive to structure settlements as annuities rather than taking lump sums. The annuity allows tax-free compounding that can significantly increase your lifetime payments.

Interest on delayed payments sometimes becomes taxable even in physical injury cases. If a court awards you $100,000 plus interest from the date of injury to the date of payment, the underlying $100,000 remains tax-free, but the interest component may be taxable. The IRS views that interest as compensation for the time-value of money, not compensation for your injury.

Tax Rules for Different Types of Settlement Annuities

Not all settlements receive identical tax treatment. The nature of your underlying claim determines whether your annuity payments arrive tax-free or generate annual 1099 forms. This annuity settlement taxation guide breaks down the most common scenarios:

| Settlement Type | Principal Taxability | Interest/Growth Taxability | IRS Code Reference |

| Personal Injury (Physical) | Tax-free | Tax-free | IRC § 104(a)(2) |

| Workers' Compensation | Tax-free | Tax-free | IRC § 104(a)(1) |

| Medical Malpractice (Physical harm) | Tax-free | Tax-free | IRC § 104(a)(2) |

| Wrongful Death (Physical injury basis) | Tax-free | Tax-free | IRC § 104(a)(2) |

| Employment Discrimination | Taxable | Taxable | Excluded from § 104(a)(2) |

| Emotional Distress (No physical injury) | Taxable (except medical expenses) | Taxable | Excluded from § 104(a)(2) |

| Punitive Damages | Taxable | Taxable | IRC § 104(a)(2) exclusion |

| Breach of Contract | Taxable | Taxable | General income principles |

Workers' compensation cases receive particularly favorable treatment. Section 104(a)(1) excludes workers' comp benefits from income, and this exclusion extends to structured settlements funding workers' comp claims. Even states with their own income taxes typically exempt workers' comp settlements.

Medical malpractice settlements depend entirely on whether the malpractice caused physical harm. A surgeon's error resulting in permanent disability qualifies for tax-free treatment. But a therapist's breach of confidentiality causing emotional distress—even if it's clearly malpractice—produces taxable settlement income.

Wrongful death settlements inherit the tax status of the deceased's underlying claim. If your spouse died from injuries in an accident, the settlement compensating your loss receives tax-free treatment because it stems from physical injuries. The decedent's estate may face different rules for pain and suffering damages incurred before death.

Employment settlements create the most confusion. Back pay, front pay, and compensatory damages for discrimination are all taxable as ordinary income. The employer should withhold taxes just like regular wages. Emotional distress damages in employment cases are taxable, though you can exclude the portion allocating to medical expenses you didn't previously deduct.

Punitive damages are always taxable, even in physical injury cases. Congress explicitly carved out punitive damages from Section 104(a)(2)'s exclusion. If your settlement includes both compensatory and punitive components, only the compensatory portion escapes taxation.

Common Mistakes That Trigger Unexpected Tax Bills

The difference between a tax-free structured settlement and a taxable mess often comes down to timing and paperwork. Small errors in how your settlement is documented or structured can cost tens of thousands in unexpected taxes.

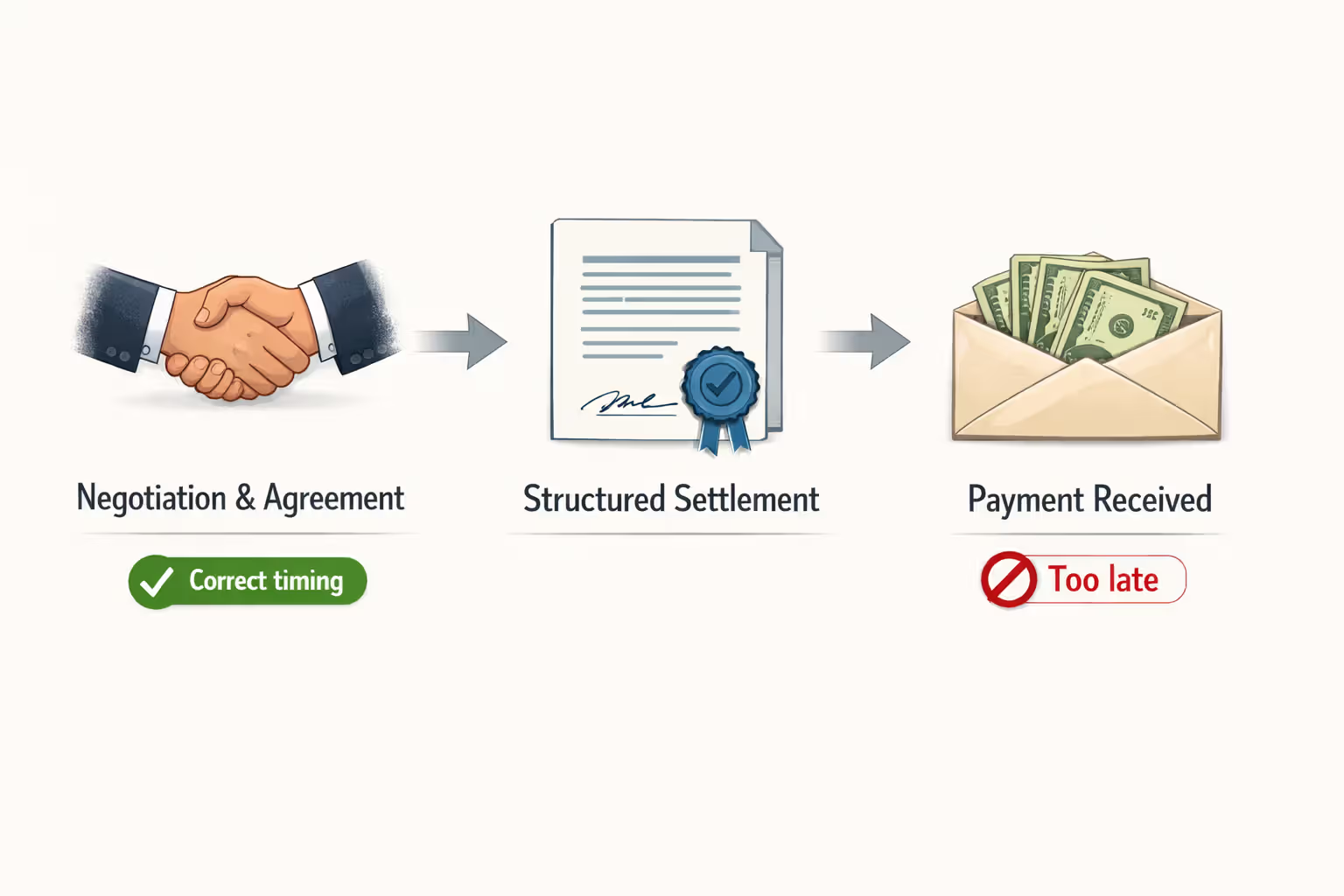

Constructive receipt kills more tax-free structures than any other mistake. The IRS applies the constructive receipt doctrine when you have unrestricted access to funds before they're placed in a structured settlement. If you receive a check for $500,000, deposit it, and then decide two weeks later to purchase an annuity, you've already constructively received the money. The annuity becomes a personal investment, and all growth is taxable.

The settlement must be structured before you have the right to receive the funds. Your attorney negotiates the periodic payment terms as part of the settlement agreement itself. Once you have the legal right to demand a lump sum, structuring that money no longer provides tax benefits.

Author: Danielle Morgan;

Source: avayabcm.com

Improper assignment occurs when the defendant or insurer fails to properly transfer payment obligations to a qualified assignment company. Section 130 requires specific language in the assignment agreement and restricts who can serve as the assignee. Using an assignment company that doesn't meet Section 130 requirements can disqualify the entire structure.

Commingling settlement types within a single annuity creates reporting headaches. Suppose your lawsuit included both physical injury claims (tax-free) and lost wage claims (taxable). If the settlement agreement doesn't clearly allocate amounts between these categories, the IRS may treat the entire annuity as taxable. Each component needs separate documentation and potentially separate annuities.

Punitive damages allocation errors happen when settlement agreements fail to specify how much compensates actual injury versus punishment. Without clear allocation, the IRS may recharacterize compensatory damages as punitive (and therefore taxable). Courts sometimes reject allocation agreements that appear unreasonable, especially when plaintiffs try to minimize punitive damages to reduce taxes.

The most expensive mistake I see is clients who negotiate their settlement without tax counsel, then call me afterward to 'fix' the tax problems. Once you've signed an agreement giving you the right to a lump sum, no amount of creative restructuring will restore Section 104 benefits. The time to plan is before you sign, not after

— Sarah Chen

Selling payments to factoring companies triggers harsh tax consequences. If you sell your structured settlement payments for a lump sum, Section 5891 imposes a 40% excise tax on the factoring company—and they typically pass this cost to you through a reduced purchase price. You'll also owe income tax on any gain from the sale. Many sellers don't realize they're giving up tax-free income for taxable cash.

Failing to obtain court approval for payment sales in states requiring it can void the transaction entirely. The Structured Settlement Protection Act and similar state laws require judicial review before you can sell payments. Proceeding without approval may leave you liable for taxes without actually receiving the sale proceeds.

Tax Planning Strategies for Settlement Recipients

Smart tax planning for settlement annuities begins during settlement negotiations, not at tax time. Once the agreement is signed and payments begin, your options narrow dramatically.

Structure before settlement is the cardinal rule. Your attorney should negotiate periodic payment terms as part of the original settlement agreement. The defendant agrees to fund a qualified assignment, which purchases an annuity to make payments. You never have the right to demand a lump sum, so constructive receipt never occurs.

Use qualified assignment companies that specialize in Section 130 assignments. These companies have the expertise and financial stability to properly structure the arrangement. They'll prepare the required documentation, work with highly-rated annuity issuers, and ensure compliance with IRS requirements.

Maintain clear documentation of your settlement's tax status. Keep copies of the settlement agreement, release, qualified assignment agreement, and annuity contract. If the IRS ever questions your non-reporting of annuity payments, you'll need these documents to prove Section 104(a)(2) qualification.

Author: Danielle Morgan;

Source: avayabcm.com

Separate physical and non-physical components into distinct settlements when possible. If your case includes both physical injuries and employment claims, negotiate separate settlement agreements with separate annuities. This prevents contamination of the tax-free physical injury settlement by the taxable employment components.

Consider state tax implications even though federal law governs most settlement taxation. A handful of states tax certain settlements that federal law treats as tax-free, or impose special reporting requirements. California, for example, requires information returns for some structured settlements even when no tax is due.

Coordinate with benefit programs carefully. While structured settlement payments from physical injuries don't generate taxable income, they may still count as resources for means-tested programs like Supplemental Security Income or Medicaid. Special needs trusts can preserve benefit eligibility while protecting settlement funds.

Document medical expenses separately from other damages. If your settlement includes reimbursement for medical expenses you previously deducted, that portion becomes taxable. Careful allocation in the settlement agreement can minimize this issue.

Plan for future flexibility by including commutation provisions if appropriate. Some structured settlements allow you to accelerate payments under specific circumstances (like buying a home or paying for education) without triggering adverse tax consequences. These provisions must be carefully drafted to avoid constructive receipt problems.

Avoid qualified settlement funds for physical injury cases when possible. While Section 468B qualified settlement funds serve useful purposes in some cases, they can complicate tax treatment and create unnecessary reporting requirements for straightforward physical injury settlements.

What Happens When You Sell or Transfer Your Annuity Payments

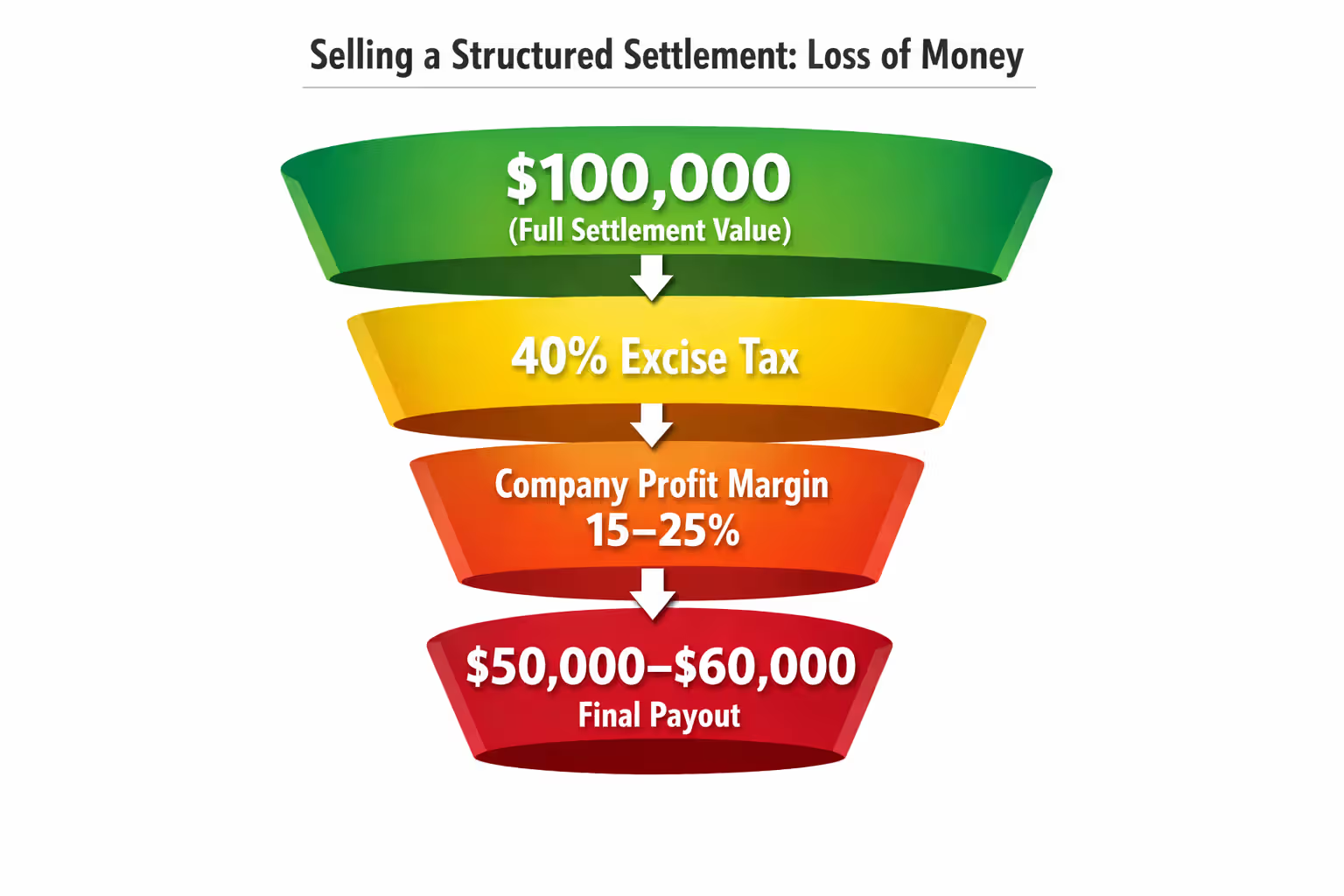

Factoring companies advertise heavily, promising cash now for your structured settlement payments. What they don't emphasize: selling those payments can cost you 40% or more in taxes and fees, converting tax-free income into taxable cash.

Section 5891 imposes a 40% excise tax on factoring companies that purchase structured settlement payment rights. The statute technically taxes the factoring company, but in practice, they reduce what they pay you to cover this cost. If your payments have a present value of $100,000, expect offers around $50,000-$60,000 after the excise tax and the company's profit margin.

The excise tax applies to the difference between the present value of the payments acquired and the amount paid to acquire them—effectively taxing the factoring company's discount. But since this reduces what you receive, you're economically bearing most of the tax burden.

You'll also owe income tax on any gain from the sale. Even though your original settlement was tax-free under Section 104(a)(2), selling the payment stream can create taxable income. The tax treatment depends on whether you're considered to have sold a capital asset (capital gains rates) or ordinary income rights (ordinary income rates). Recent IRS guidance suggests most sales generate ordinary income.

The factoring company will issue Form 1099-MISC reporting the transaction. You must report this income on your tax return, and you'll owe taxes at your marginal rate. Combined with the economic impact of the Section 5891 excise tax, you might net only 50 cents on the dollar.

State structured settlement protection acts require court approval before you can sell payments. The judge must find that the transfer is in your best interest, considering factors like your financial situation, the terms of the transfer, and whether you received independent professional advice. Some states prohibit transfers entirely for certain types of settlements, like workers' compensation.

Courts sometimes reject transfer applications when the discount rate seems excessive or the seller appears not to understand the long-term consequences. Judges have blocked sales where sellers would receive $20,000 for payments worth $100,000 over time.

If you're considering selling payments, explore alternatives first. Personal loans, home equity lines, or even credit cards may cost less than giving up tax-free structured settlement income. Some annuity contracts allow partial withdrawals or policy loans that preserve the tax-free nature of your payments.

Never sign transfer documents without independent legal advice. Factoring companies often have sellers sign agreements waiving rights or limiting the company's liability. An attorney can review the terms and calculate the true cost of the transaction.

Author: Danielle Morgan;

Source: avayabcm.com

Frequently Asked Questions About Settlement Annuity Taxes

Structured settlement annuity taxation follows clear rules, but the stakes are high enough that small mistakes carry big price tags. Physical injury settlements structured properly before you have the right to receive funds provide completely tax-free income for life. Non-physical injury settlements, punitive damages, and improperly structured arrangements generate taxable income that can significantly reduce what you actually keep.

The key to maximizing your after-tax settlement value is planning before you sign the settlement agreement. Work with attorneys and tax professionals who understand Section 104(a)(2), qualified assignments, and constructive receipt rules. Once you've signed an agreement giving you the right to a lump sum, you can't retroactively create tax-free structured payments.

If you already have a structured settlement, protect its tax-free status by avoiding sales to factoring companies except in genuine emergencies. The 40% excise tax and income tax on gains can consume half your payment value, converting tax-free income into expensive cash.

Keep thorough documentation of your settlement's tax status, report taxable settlements properly, and consult professionals before making changes to your payment stream. The tax benefits of properly structured settlements are too valuable to risk through careless mistakes.