Top view of a financial advisor desk with settlement agreement documents, calculator, pen, glasses, stack of dollar bills, and laptop showing investment growth chart

Structured Settlement Tax Planning Guide

Content

Structured settlements represent one of the most powerful tax-advantaged financial tools available to personal injury victims, yet most recipients never fully leverage their benefits. Unlike nearly every other income source in the United States, properly structured settlement payments can flow to you completely free from federal income tax—no deductions needed, no phase-outs to worry about, and no Alternative Minimum Tax complications.

The difference between a well-planned structured settlement and a poorly managed one can easily exceed six figures over a lifetime. A $500,000 settlement structured to provide $2,000 monthly for 30 years grows tax-free inside the annuity, while that same amount taken as a lump sum and invested in taxable accounts could lose 25-35% of its growth to taxes depending on your bracket.

Most settlement recipients focus exclusively on the payment amount and schedule, overlooking critical tax planning opportunities that could save tens of thousands of dollars. Understanding structured settlement tax planning means grasping not just what's tax-free today, but how to coordinate these payments with your broader financial picture, avoid common pitfalls that trigger unexpected tax bills, and structure your settlement to provide maximum lifetime value.

What Makes Structured Settlements Tax-Advantaged

Internal Revenue Code Section 104(a)(2) creates an extraordinary exception to normal taxation rules. This provision excludes from gross income "the amount of any damages (other than punitive damages) received (whether by suit or agreement and whether as lump sums or as periodic payments) on account of personal physical injuries or physical sickness."

The critical word is "physical." If your settlement stems from a car accident, medical malpractice, slip-and-fall injury, or workers' compensation claim involving bodily harm, your damages qualify. Emotional distress claims without physical injury, employment discrimination cases, and breach of contract disputes do not qualify for tax-free treatment under this section.

The tax exclusion under IRC Section 104(a)(2) isn't just a minor benefit—it's a complete exemption that transforms the economic value of settlement proceeds. I've seen clients effectively increase their after-tax income by 40% compared to taking a lump sum and managing it themselves in taxable accounts. The key is understanding the rules before you finalize the settlement structure, because once signed, these decisions are typically irrevocable

— Patricia Hernandez

Qualified structured settlements enjoy three distinct tax advantages. First, the initial settlement amount—whether $100,000 or $10 million—generates no immediate tax liability when structured. Second, all investment growth inside the annuity accumulates tax-free. Third, every payment you receive maintains its tax-free character, regardless of how much the annuity has grown.

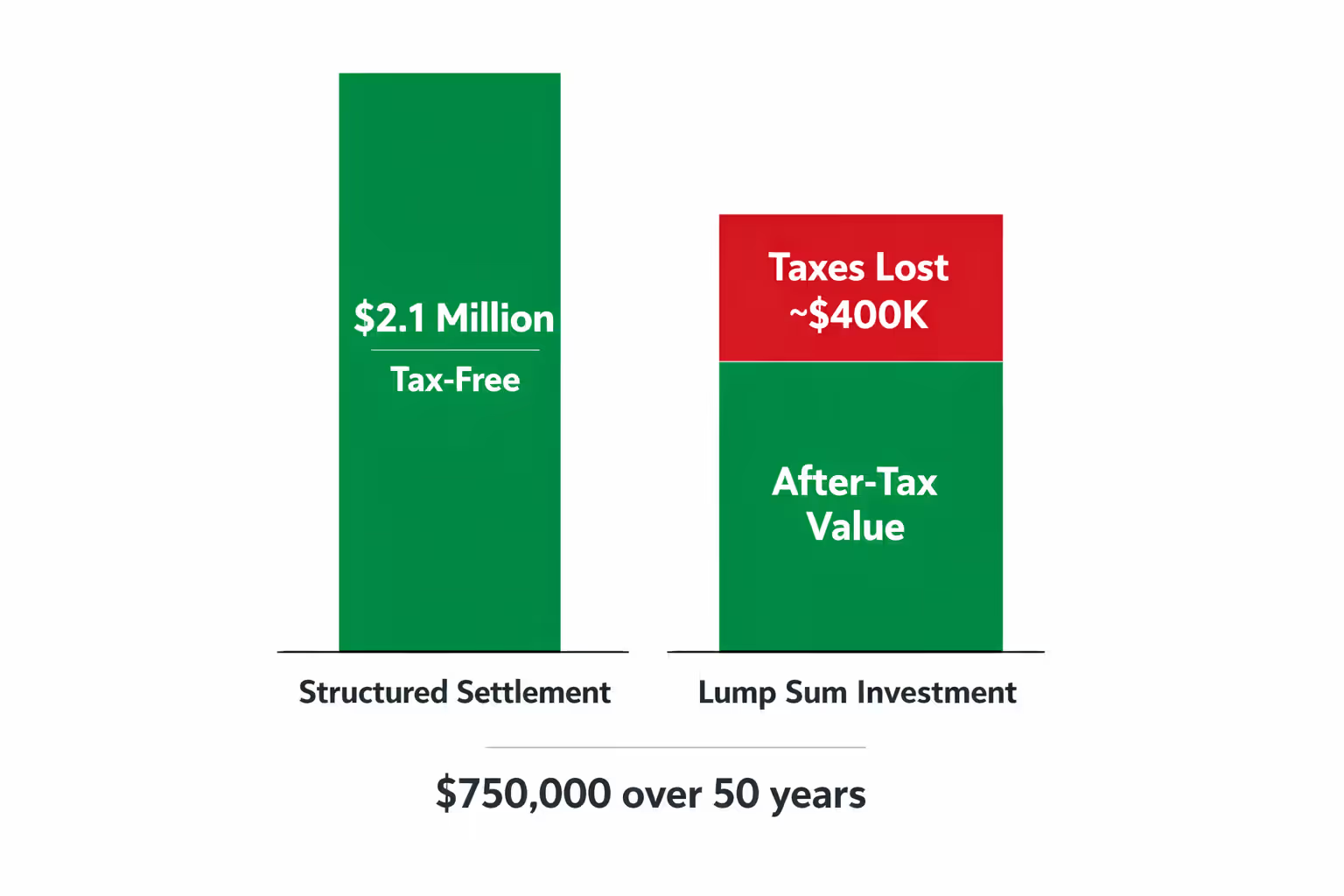

Consider a 35-year-old receiving a $750,000 settlement. If structured to pay $3,500 monthly for life, the annuity might ultimately distribute $2.1 million over 50 years. In a qualified settlement, all $2.1 million arrives tax-free. That same $750,000 invested in a taxable brokerage account would generate annual tax bills on dividends, interest, and capital gains—potentially reducing the after-tax value by $400,000 or more over the same period.

Author: Olivia Carmichael;

Source: avayabcm.com

Non-qualified structured settlements follow different rules. These typically involve punitive damages, interest portions of settlements, or employment-related claims. While you can still structure these payments over time, only the return of principal remains tax-free. The growth portion gets taxed as ordinary income when received. A $200,000 punitive damage award structured over ten years might have $120,000 representing principal (tax-free) and $80,000 representing earnings (fully taxable at your ordinary income rate).

The assignment company matters significantly for tax treatment. In a qualified assignment, the defendant transfers the obligation to make periodic payments to a highly-rated assignment company, which purchases an annuity to fund those payments. This structure ensures the payments remain outside your constructive receipt—you never have the option to take a lump sum, which preserves the tax exclusion. Improper assignments or retaining control over the funds can destroy the tax benefits entirely.

Common Tax Planning Mistakes That Cost Settlement Recipients Thousands

Selling Payment Rights Without Understanding Tax Consequences

The structured settlement secondary market allows recipients to sell future payment rights for immediate cash. While sometimes necessary, most sellers don't realize this transaction converts tax-free money into partially taxable proceeds.

When you sell payment rights, the IRS treats the transaction as the sale of a capital asset. You pay capital gains tax on the difference between your "basis" (typically zero, since you paid nothing for the structured settlement) and the sale proceeds. If you sell $100,000 in future payments for $65,000 today, you'll owe long-term capital gains tax on the full $65,000—potentially $9,750 at the 15% federal rate, plus state taxes.

Worse yet, the discount rates in the secondary market typically range from 9% to 18% annually. Selling ten years of $1,000 monthly payments ($120,000 total) might net you only $60,000-$75,000 today. You've sacrificed $45,000-$60,000 in value and triggered a tax bill on money that would have arrived completely tax-free.

The math rarely works unless you face a genuine emergency. Before selling, exhaust other options: home equity lines of credit, personal loans, payment plans with creditors, or borrowing from retirement accounts. These alternatives often cost less than the combined discount and tax hit from selling structured payments.

Improper Beneficiary Designations

Structured settlements require careful beneficiary planning to avoid unnecessary estate taxes and ensure smooth transfers. Many recipients simply name their spouse or children without considering the tax implications.

If you die with remaining guaranteed payments, those payments transfer to your designated beneficiaries and continue to flow tax-free—but only if properly designated in the original settlement documents. Failing to name beneficiaries means the commuted value (lump sum equivalent) gets paid to your estate, where it becomes subject to estate taxes if your estate exceeds the federal exemption threshold ($12.92 million in 2023, but potentially much lower in future years).

Naming minor children directly creates problems too. Courts typically require guardianship proceedings and supervised accounts until the child reaches 18 or 21, adding legal costs and restrictions. Better options include establishing trusts to receive payments, naming adult trustees, or using custodial accounts under the Uniform Transfers to Minors Act.

Some recipients name beneficiaries but never update them after life changes. Your ex-spouse probably shouldn't remain the beneficiary after divorce. Adult children may need different allocations as their financial situations evolve. Review beneficiary designations every three to five years and after major life events.

Author: Olivia Carmichael;

Source: avayabcm.com

Mixing Qualified and Non-Qualified Funds

Settlements often include both compensatory damages (tax-free) and punitive damages or interest (taxable). Proper allocation in the settlement agreement determines your tax treatment for decades.

The mistake happens when attorneys or settlement planners fail to clearly separate these components. A $600,000 settlement might include $500,000 for physical injuries (qualified) and $100,000 in punitive damages (non-qualified). If the settlement agreement lumps everything together without explicit allocation, the IRS may argue that a portion of every payment represents taxable income.

Proper documentation requires specific language: "Of the total settlement amount, $500,000 represents compensation for physical injuries and physical sickness under IRC Section 104(a)(2), and $100,000 represents punitive damages taxable under IRC Section 61." Each component should fund separate structured settlements with distinct payment schedules and clear tax reporting.

Pre-judgment interest presents another trap. Interest that accrues before the judgment or settlement always counts as taxable income, even in physical injury cases. If your case took five years to settle and accumulated $50,000 in pre-judgment interest, that $50,000 is fully taxable regardless of how you structure it. Settlement agreements should explicitly identify interest components to avoid accidentally treating taxable money as tax-free.

Five Strategic Methods to Optimize Your Settlement Tax Position

Strategic structured settlement tax planning methods extend far beyond simply accepting the defendant's initial offer. These five approaches can substantially increase your after-tax wealth.

Method 1: Front-Loading or Back-Loading Payment Schedules

Your tax bracket changes throughout life. High earners in their peak working years (ages 45-60) benefit from back-loaded structures that defer larger payments until retirement when their bracket drops. Someone earning $180,000 annually might structure smaller payments now and larger payments beginning at age 65, when employment income stops and they drop from the 32% federal bracket to 12% or 22%. While the structured settlement payments themselves remain tax-free, this timing reduces the taxation of other income sources and preserves eligibility for various tax credits and deductions that phase out at higher income levels.

Conversely, younger recipients not yet in their peak earning years might front-load payments. A 25-year-old earning $45,000 annually could take larger payments now for education or home purchase, then reduce payments during their 40s and 50s when career income peaks. This smooths lifetime income and maximizes the relative value of tax-free payments during lower-earning periods.

Method 2: Incorporating Lump Sum Payments at Strategic Intervals

Pure annuity structures provide steady income but lack flexibility for major expenses. Hybrid structures include periodic lump sums alongside regular payments—perhaps $2,000 monthly plus $50,000 every five years.

Time these lump sums for anticipated needs: college tuition payments, mortgage payoffs, business startup capital, or retirement account funding. A $30,000 lump sum at age 59½ allows you to maximize IRA contributions for several years, effectively converting tax-free settlement money into tax-deferred retirement savings that grows further.

Some recipients structure lump sums to coincide with required minimum distributions (RMDs) from retirement accounts beginning at age 73. This tax-free income can offset the tax hit from RMDs, reducing your effective tax rate on retirement account withdrawals.

Author: Olivia Carmichael;

Source: avayabcm.com

Method 3: Qualified Assignment Benefits and Cost Basis Optimization

Qualified assignments transfer the payment obligation from the defendant to a highly-rated assignment company. This removes the payments from your constructive receipt and ensures tax-free treatment, but it also provides another benefit: creditor protection.

In most states, properly structured settlement payments enjoy significant protection from creditors, lawsuits, and bankruptcy proceedings. This protection exceeds what you'd receive from simply investing a lump sum, even in otherwise protected accounts. For professionals in high-liability occupations (physicians, business owners, landlords), this asset protection element adds substantial value beyond pure tax benefits.

The assignment also eliminates counterparty risk. You're no longer dependent on the defendant's financial stability. The assignment company and its annuity carrier—typically rated AA or better—now guarantee your payments. This credit quality upgrade matters enormously for large settlements paid over decades.

Method 4: Coordinating with Existing Tax-Advantaged Accounts

Structured settlement payments free up other income for tax-advantaged investing. If your settlement provides $30,000 annually, you might redirect $30,000 of employment income into 401(k) contributions, Health Savings Accounts, or backdoor Roth conversions.

This coordination effectively multiplies your tax benefits. The structured settlement income arrives tax-free, while maxing out retirement contributions reduces your taxable employment income and builds additional tax-deferred wealth. A married couple with $150,000 in employment income and $40,000 in annual structured settlement payments could potentially contribute $22,500 to a 401(k), $7,750 to HSAs, and $13,000 to IRAs, reducing taxable income to roughly $106,750 while maintaining their lifestyle with settlement payments.

For business owners, structured settlement income can support aggressive retirement plan contributions—defined benefit plans, cash balance plans, or Solo 401(k)s—that might otherwise strain cash flow. The guaranteed tax-free income provides a stable base that enables more aggressive tax-deferred savings from business income.

Method 5: Multi-Generational Planning with Guaranteed Periods

Structured settlements can include guaranteed payment periods that extend beyond your life expectancy—for example, life payments with 30 years guaranteed. If you die after 15 years, payments continue to beneficiaries for another 15 years, still completely tax-free.

This creates a multi-generational tax-free income stream. A 50-year-old structuring $1 million with life payments and 40 years guaranteed might receive payments until age 85, then have 15 years of payments flow tax-free to children or grandchildren. The family receives perhaps $2.5 million total over 40 years with zero income tax at any point.

Compare this to leaving $1 million in a traditional IRA, which triggers income taxes for beneficiaries under the SECURE Act's 10-year distribution rule. Those beneficiaries might pay $250,000-$350,000 in taxes on inherited retirement accounts, while structured settlement beneficiaries pay nothing.

How Settlement Annuities Compare to Other Tax-Deferred Vehicles

Understanding where structured settlements fit in the broader landscape of tax-advantaged investing helps you make informed allocation decisions.

| Vehicle | Tax Treatment of Contributions | Tax Treatment of Growth | Tax Treatment of Distributions | Contribution Limits | Flexibility/Liquidity | Estate Tax Treatment |

| Structured Settlement | No deduction (after-tax) | Tax-free accumulation | Completely tax-free | No limits on qualified settlements | Very low—payments fixed | Tax-free to beneficiaries; included in estate value |

| Traditional IRA | Tax-deductible (if eligible) | Tax-deferred | Ordinary income tax | $6,500/year ($7,500 if 50+) | Moderate—10% penalty before 59½ | Ordinary income tax to beneficiaries |

| 401(k) | Tax-deductible | Tax-deferred | Ordinary income tax | $22,500/year ($30,000 if 50+) | Low—penalties and restrictions | Ordinary income tax to beneficiaries |

| Municipal Bonds | No deduction (after-tax) | Tax-free interest only | Tax-free interest; capital gains on sale | No limits | High—can sell anytime | Capital gains tax on appreciation |

| Commercial Annuities | No deduction (after-tax) | Tax-deferred | Ordinary income on gains | No limits | Low—surrender charges typical | Ordinary income tax on gains to beneficiaries |

The structured settlement's combination of tax-free growth and tax-free distributions makes it superior to traditional retirement accounts for recipients who qualify. A $500,000 settlement growing at 4% annually and distributed over 30 years delivers roughly $865,000 tax-free. That same $500,000 in a traditional IRA, even with identical 4% growth, might deliver only $600,000-$650,000 after accounting for ordinary income taxes on distributions.

Municipal bonds offer tax-free interest but typically yield 2-3% currently, far below the 4-5% rates available in structured settlement annuities. Munis also carry interest rate risk and default risk that structured settlements avoid. A $1 million municipal bond portfolio yielding 3% provides $30,000 annually, while a $1 million structured settlement might provide $45,000-$50,000 annually with equivalent safety and superior tax treatment.

Commercial annuities share some characteristics with structured settlements but lack the complete tax exemption. With commercial annuities, only the return of principal is tax-free; all growth is taxed as ordinary income when distributed. This makes them significantly less attractive than qualified structured settlements, though they remain useful for non-qualified settlement components.

The inflexibility of structured settlements represents their primary disadvantage. You cannot access principal, change payment schedules, or respond to emergencies without selling payments at steep discounts. This lack of liquidity demands careful planning—you need other liquid assets for unexpected expenses. Most advisors recommend maintaining 6-12 months of expenses in liquid savings even with a structured settlement providing steady income.

Coordinating Structured Settlements With Estate and Retirement Planning

Structured settlement financial tax planning requires integration with your broader wealth management strategy, particularly estate planning and retirement preparation.

Estate Tax Implications and Valuation

Structured settlements are included in your taxable estate at their commuted value—the lump sum required to fund remaining payments. A settlement paying $3,000 monthly for 20 more years might have a commuted value of $500,000-$550,000, depending on interest rates.

For estates exceeding the federal exemption ($12.92 million in 2023), this creates a 40% estate tax on the commuted value. However, payments to beneficiaries after your death continue to arrive tax-free from income tax perspective. This creates a planning opportunity: the estate pays estate tax once on the present value, but beneficiaries receive potentially much larger total payments completely free of income tax.

Married couples can use portability and marital deduction strategies to defer estate taxes until the second spouse dies. Naming your spouse as primary beneficiary with children as contingent beneficiaries allows the structured settlement to pass estate-tax-free to your spouse, preserving your estate tax exemption for other assets.

Some recipients use life insurance to cover potential estate taxes on structured settlements. A $500,000 structured settlement might generate $150,000 in estate taxes for a high-net-worth individual. A $150,000 life insurance policy held in an irrevocable life insurance trust (ILIT) could cover this tax, ensuring beneficiaries receive the full value of continuing payments.

Medicare and Medicaid Considerations

Structured settlement payments count as income for Medicare premium surcharges (IRMAA—Income-Related Monthly Adjustment Amount). If your modified adjusted gross income exceeds $97,000 (single) or $194,000 (married), you'll pay higher Medicare Part B and Part D premiums.

Wait—didn't we say structured settlements are tax-free? They are for income tax purposes, but IRMAA calculations use modified adjusted gross income, which includes tax-exempt income. A retiree with $50,000 in Social Security, $30,000 in IRA withdrawals, and $25,000 in structured settlement payments has MAGI of $105,000, triggering IRMAA surcharges of roughly $1,000-$2,000 annually.

Planning around IRMAA involves timing other income sources. You might delay IRA withdrawals, execute Roth conversions before Medicare eligibility at 65, or structure settlements with smaller payments during Medicare years if you're close to IRMAA thresholds.

Medicaid planning presents different challenges. Structured settlement income counts toward Medicaid eligibility limits for long-term care coverage. Most states set income limits around $2,700-$2,900 monthly for nursing home Medicaid. A structured settlement paying $3,500 monthly could disqualify you from Medicaid coverage, leaving you to pay $8,000-$12,000 monthly nursing home costs out-of-pocket until assets are depleted.

Medicaid Asset Protection Trusts (MAPTs) generally cannot hold structured settlements since you cannot transfer the payment stream. However, some states allow Qualified Income Trusts (QIT or "Miller Trusts") to receive structured settlement payments, spend down to the Medicaid limit, and preserve Medicaid eligibility. This requires specialized elder law advice well before long-term care needs arise.

Retirement Income Coordination

Structured settlements provide a tax-free income floor in retirement, allowing more aggressive strategies with other assets. If your settlement provides $40,000 annually, you might delay Social Security until age 70 (increasing benefits by 24-32%), knowing the settlement covers basic expenses during the delay.

The tax-free nature also enables Roth conversion strategies. Converting traditional IRA assets to Roth IRAs triggers ordinary income tax, but structured settlement income doesn't add to your tax bracket. A retiree with $35,000 in structured settlement payments could convert $50,000 from a traditional IRA to Roth while staying in the 12% or 22% bracket, whereas someone with $35,000 in taxable pension income would face higher brackets on the same conversion.

Required minimum distributions (RMDs) from retirement accounts beginning at age 73 can push retirees into higher brackets. Structured settlement income doesn't trigger RMDs and isn't added to the calculation, but the tax-free income can offset the tax burden from RMDs on other accounts. Strategic planning involves balancing structured settlement payment amounts with anticipated RMDs to minimize lifetime taxes.

Author: Olivia Carmichael;

Source: avayabcm.com

When to Hire a Structured Settlement Tax Advisor

Most settlement recipients benefit from professional tax guidance, but certain situations absolutely require specialized expertise.

Red Flags Requiring Professional Help

Settlements exceeding $500,000 justify professional tax planning given the potential savings. An advisor might identify strategies worth $50,000-$150,000 in lifetime tax savings, easily justifying fees of $3,000-$8,000.

Multiple income sources complicate planning. If you're receiving structured settlement payments, employment income, rental property income, and retirement account distributions simultaneously, coordinating these sources to minimize taxes requires sophisticated modeling that most general tax preparers cannot provide.

Business owners face additional complexity. Structured settlement income affects qualified business income deductions, retirement plan contribution limits, and estimated tax payment requirements. Specialized advisors understand these interactions and can optimize your overall tax position.

Estate values approaching the federal exemption threshold ($12.92 million in 2023) demand professional estate planning. The commuted value of your structured settlement affects whether you'll face estate taxes, and strategies like spousal transfers, charitable remainder trusts, or life insurance planning require expert guidance.

Medicare or Medicaid planning needs also warrant professional help. If you're within five years of Medicare eligibility or anticipate potential long-term care needs, an advisor specializing in elder law and settlement taxation can structure your affairs to minimize premium surcharges and preserve benefit eligibility.

What to Look For in an Advisor

Seek advisors with specific structured settlement experience, not just general tax knowledge. Relevant credentials include Certified Public Accountant (CPA) with high-net-worth client experience, Certified Financial Planner (CFP) with settlement specialization, or attorneys with both tax law and personal injury backgrounds.

Membership in the National Structured Settlement Trade Association (NSSTA) indicates specialized knowledge. Ask potential advisors how many structured settlement clients they've served and request references from clients with similar situations to yours.

Fee structure matters significantly. Fee-only advisors who charge hourly rates ($250-$500/hour) or flat project fees ($3,000-$10,000 for comprehensive planning) avoid conflicts of interest. Avoid advisors who earn commissions on selling your payment rights or who push you toward secondary market transactions—these arrangements create incentives contrary to your interests.

The advisor should coordinate with your existing team. Your settlement tax advisor needs to communicate with your personal injury attorney, estate planning attorney, and investment advisor to ensure all strategies align. Advisors who work in isolation often miss important interactions between different aspects of your financial life.

Cost Versus Benefit Analysis

A comprehensive structured settlement tax planning engagement typically costs $3,000-$8,000, depending on complexity. For a $300,000 settlement, this represents 1-2.5% of the settlement value. For a $2 million settlement, it's 0.15-0.4%.

The potential benefits far exceed these costs. Proper beneficiary designations might save $100,000 in estate taxes. Coordinating with retirement account strategies could reduce lifetime taxes by $75,000. Avoiding a single mistake—like selling payment rights without understanding tax consequences—could save $15,000-$30,000.

Even modest settlements benefit from at least a consultation. A two-hour consultation costing $600-$1,000 might identify opportunities or risks worth tens of thousands of dollars. Think of this as insurance against costly mistakes rather than an optional expense.

Frequently Asked Questions About Structured Settlement Taxation

Structured settlement tax planning represents one of the few remaining opportunities for completely tax-free investment growth and income in the United States tax code. The combination of IRC Section 104(a)(2) exclusions, tax-free compounding, and tax-free distributions creates economic value that far exceeds the nominal settlement amount—often by hundreds of thousands of dollars over a lifetime.

The key to maximizing these benefits lies in understanding the rules before finalizing your settlement. Once you sign the settlement agreement and the structured annuity is established, your options narrow dramatically. Work with experienced advisors who understand both the tax rules and the practical implications for your specific situation.

Avoid the common mistakes that cost settlement recipients thousands: selling payment rights without considering tax consequences, failing to properly designate beneficiaries, and mixing qualified and non-qualified settlement components without clear documentation. These errors can transform tax-free money into taxable income and eliminate much of the settlement's value.

Coordinate your structured settlement with your broader financial plan. Use the tax-free income to enable aggressive retirement savings, time payments to minimize Medicare surcharges, and structure guaranteed periods to create multi-generational tax-free income streams. The inflexibility of structured settlements demands careful planning, but the tax benefits justify the effort for most recipients.

For settlements exceeding $500,000, complex situations involving multiple income sources, or recipients approaching retirement or Medicare eligibility, professional guidance from a structured settlement tax advisor typically pays for itself many times over. The specialized knowledge required to optimize these arrangements exceeds what most general tax preparers possess.

Structured settlements aren't appropriate for everyone—they sacrifice liquidity and control in exchange for tax benefits and guaranteed income. But for recipients who can afford to lock in payment schedules and who value tax-free income security, few financial tools offer comparable advantages. Understanding the tax rules, avoiding common pitfalls, and coordinating with your overall financial strategy transforms a structured settlement from a simple payment stream into a powerful wealth-building tool that can provide tax-free income for decades.