Top view of a desk with IRS tax forms 1099, structured settlement documents, calculator, pen, and laptop showing a spreadsheet

Structured Settlement Tax Documents to Keep for IRS Compliance

Content

Getting structured settlement money each month feels like a win—until tax season rolls around and you're staring at a pile of confusing paperwork. Here's what makes this tricky: you're not dealing with a simple W-2 from an employer. These payments stretch across years, sometimes decades, and the tax rules change based on why you got the settlement in the first place.

Many people just assume their payments are completely tax-free. Sometimes that's correct. Other times? Dead wrong. The difference comes down to your specific settlement terms, and proving your tax treatment requires the right documentation. Miss a key form or misunderstand what you need to save, and you might accidentally create a tax problem where none existed—or worse, ignore a legitimate tax obligation until the IRS comes knocking.

Which Structured Settlement Documents Have Tax Implications?

Tax treatment hinges on one question: what were you compensated for? The IRS draws a sharp line between physical injuries—which get favorable treatment—and everything else.

Break your leg in a car crash? Payments from that settlement typically flow to you tax-free under Internal Revenue Code Section 104(a)(2). Same goes for medical malpractice that caused physical harm or workers' compensation for a job-related injury. Physical means physical. The law is surprisingly literal here.

But let's say your settlement included $200,000 for medical bills and lost income, plus another $50,000 in punitive damages because the defendant was drunk. That $50,000 portion? Fully taxable as regular income. Or maybe you settled an employment discrimination case. Those payments face taxes (except for any portion covering actual medical expenses you incurred because of the discrimination).

Your settlement agreement becomes your most important piece of paper. This document needs to spell out exactly what each dollar compensates. Imagine an agreement that says "Defendant agrees to pay $300,000 to settle all claims." No breakdown, no specifics. The IRS can look at that vague language and decide the entire amount is taxable. Courts have backed them up on this repeatedly.

Another document worth its weight in gold: your qualified assignment agreement. This transfers payment responsibility from the defendant to a specialized annuity company. The IRS has strict requirements for these assignments. If the paperwork doesn't meet those rules, your supposedly tax-free settlement becomes taxable. Keep this document somewhere secure—a fireproof safe or bank safety deposit box works well.

Author: Andrew Halvorsen;

Source: avayabcm.com

At closing, you should receive a letter from the annuity issuer. This letter confirms which portions of your payments qualify as tax-free. Some attorneys forget to request this confirmation, so recipients never get it. If you closed your case without receiving this letter, call the annuity company tomorrow and ask them to issue one.

| What You Settled | How It's Taxed | IRS Forms You'll Get | Other Papers to Keep |

| Car accident injury (physical harm) | No taxes due | You won't get any 1099 | Settlement papers, medical bills proving injury |

| Workers' comp claim | No taxes due | You won't get any 1099 | State award letter, claim documents |

| Wrongful death (actual damages) | No taxes due | You won't get any 1099 | Death certificate, settlement contract |

| Punitive damages portion | Pay regular income tax | 1099-MISC arrives in January | Settlement showing which part is punitive |

| Job discrimination case | Pay taxes (except medical portions) | 1099-MISC, possibly W-2 | Settlement breakdown, legal bills |

| Interest on late payments | Pay taxes on 100% of interest | 1099-INT arrives in January | Payment schedule, interest calculation |

Core Tax Forms Required for Settlement Annuity Reporting

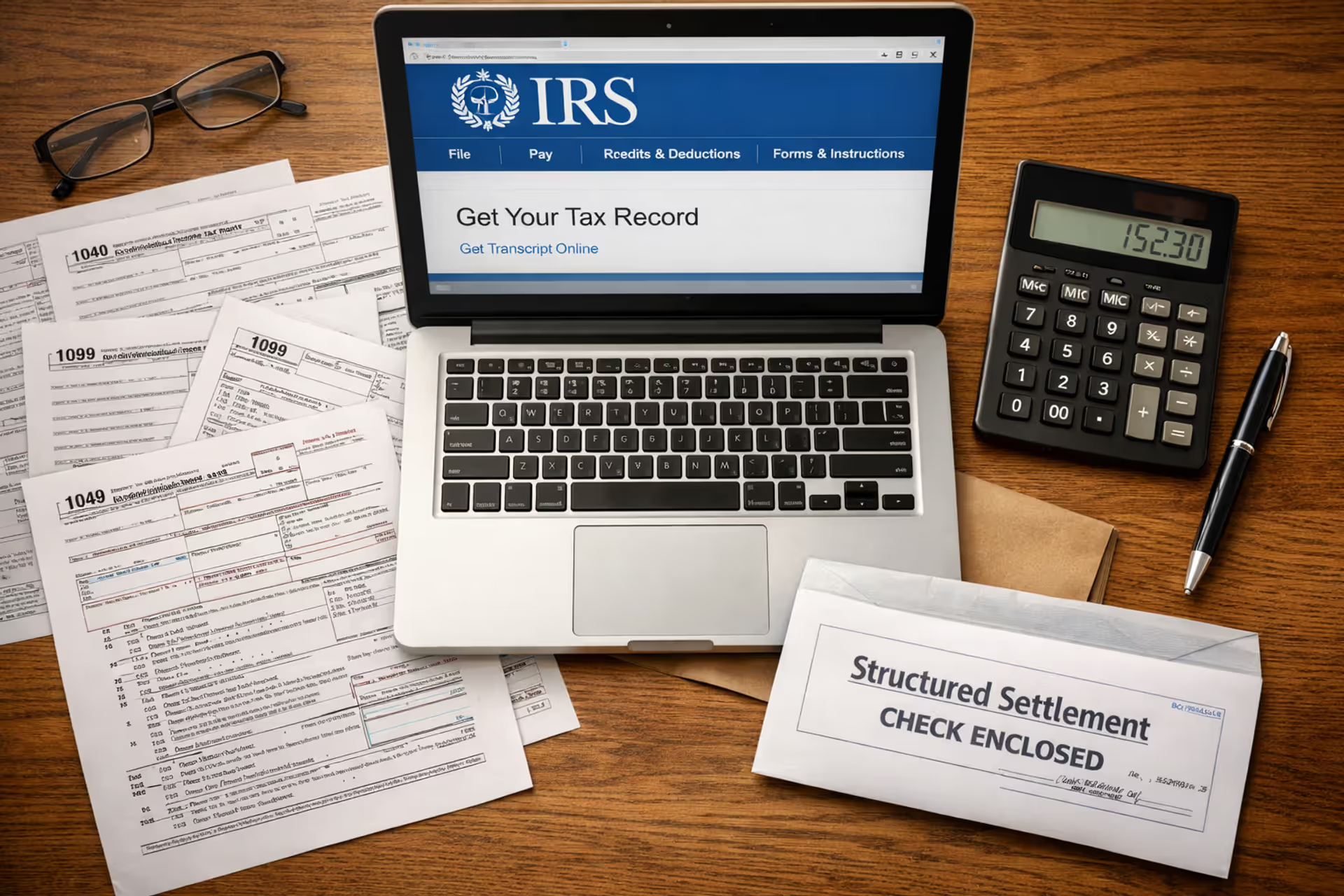

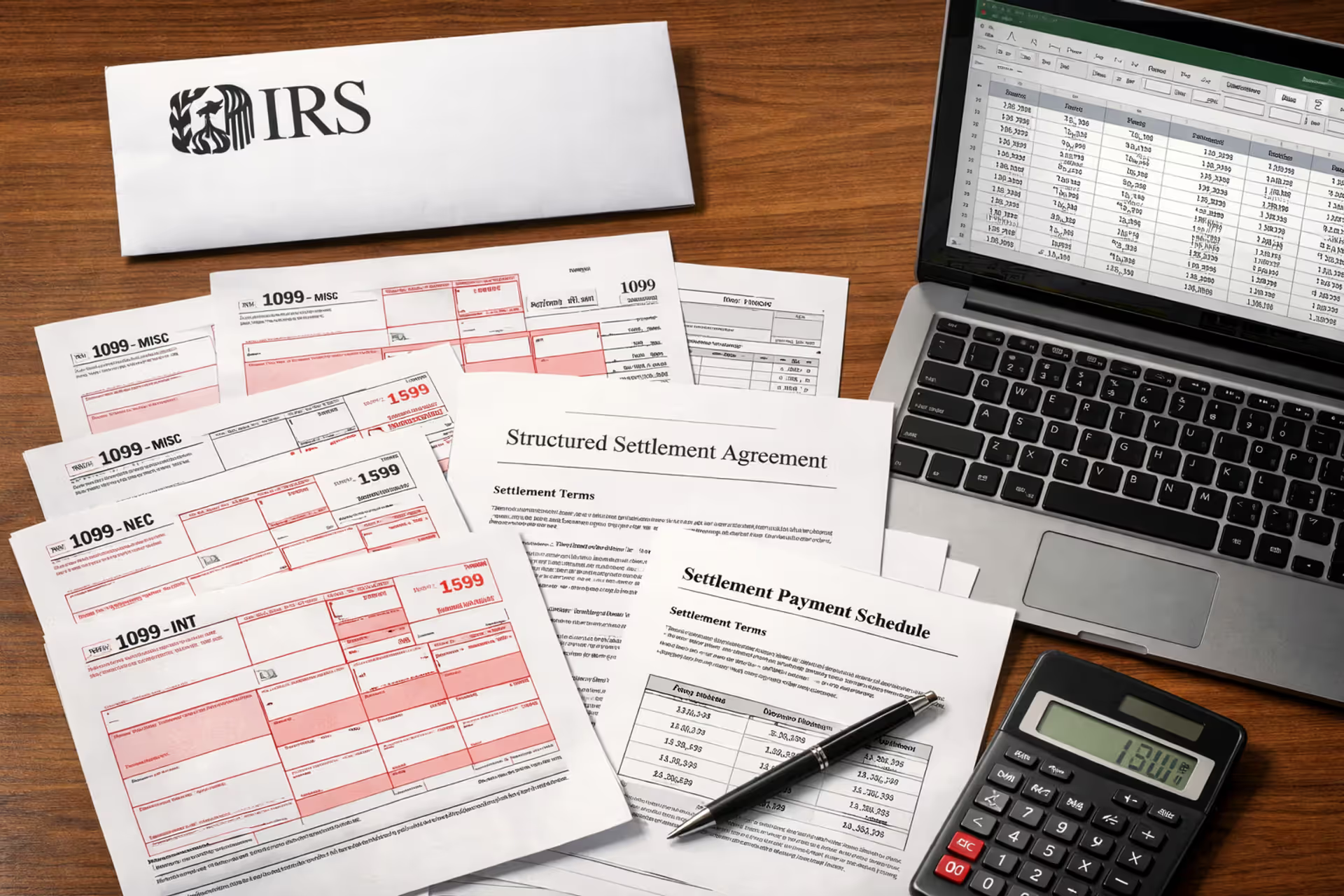

Form 1099-MISC and 1099-INT for Periodic Payments

When January rolls around, you might receive a 1099-MISC if any piece of your settlement faces taxation. Look at Box 3—that's where "Other Income" gets reported. Punitive damages go here. Employment settlements go here. Emotional distress awards (unrelated to physical injury) go here.

Now here's where it gets confusing. Let's say you settled your case in 2022, but the defendant didn't actually pay until March 2023. You might be owed interest for those months of delay. That interest? Always taxable, even when the underlying settlement isn't. You'll see this on Form 1099-INT, Box 1.

Some people get both forms in the same year. Their main payments are tax-free (so no 1099 for those), but they earned $180 in interest on delayed payments (so they get a 1099-INT for just that interest). Others receive only a 1099-MISC because their entire settlement was taxable from the start.

The IRS made changes starting in 2024. Some income that used to appear on 1099-MISC now shows up on Form 1099-NEC instead—specifically for non-employee compensation. If your settlement included back wages or similar payments, expect a 1099-NEC. Same tax treatment, different form name. Just the IRS keeping everyone on their toes.

Form W-9 and Payee Information Requirements

Before your first payment arrives, the annuity company will send you Form W-9. They need your Social Security number and confirmation that you're not subject to backup withholding. Seems simple enough, right?

Here's the catch: if you don't return the W-9, or if the information doesn't match IRS records, federal law forces the company to withhold 24% from your taxable payments automatically. They have no discretion here. You'll eventually recover that money when you file your tax return and claim the withholding, but meanwhile you're short on cash unnecessarily.

Got married and changed your name? Moved to a different state? Discovered the annuity company has your Social Security number wrong by one digit? File an updated W-9 immediately. Most companies accept these by secure upload or fax—check your payment statements for instructions.

How to Organize Your Settlement Tax Records for IRS Compliance

The IRS typically looks back three years when auditing returns. But they can go back six years if they think you substantially underreported income. For structured settlements that last decades, keep everything for at least seven years after your final payment.

Set up one dedicated folder—physical, digital, or both. Label it with your case name and settlement date. Here's what belongs inside:

The foundation documents: Your settlement agreement, the qualified assignment paperwork, release forms you signed, and the court order approving everything. These prove the tax-free nature of your payments.

Every tax form you receive: Save each 1099-MISC, 1099-INT, or 1099-NEC. Even tiny amounts matter. That $23 interest payment seems insignificant until the IRS computer flags the discrepancy three years later.

Proof of actual receipt: Bank statements or direct deposit confirmations showing when money hit your account and how much. These verify that what you received matches what the 1099 forms report.

Letters from the annuity company: Anything confirming tax treatment, answering your questions, or notifying you about corporate mergers or ownership changes.

Legal bills and fee agreements: You paid your attorney to get this settlement. Recent tax law changes eliminated most deductions for legal fees, but save the invoices anyway. Laws change.

Going digital has advantages. You can search files instantly. Cloud backup protects against house fires. But phone photos often lack the quality you need for fine print. Use a proper scanner or at least a scanning app that corrects angles and improves contrast.

Name your files descriptively: "2025-01-12_1099INT_Metropolitan_Annuity.pdf" beats "Document1.pdf" when you're frantically searching for something three years later.

Author: Andrew Halvorsen;

Source: avayabcm.com

Create a spreadsheet tracking every payment: date received, dollar amount, how much (if any) was taxable, any withholding taken out. This master list becomes invaluable if you need to reconstruct missing records or answer IRS questions. Update it monthly while details are fresh.

Common Mistakes People Make with Structured Settlement Tax Paperwork

Thinking everything is automatically tax-free. This catches people who settled employment cases or received punitive damages. They ignore the 1099-MISC that arrives, don't report the income, and then face penalties when the IRS computer automatically catches the mismatch between the form and their return.

Tossing 1099s that show zero. Some annuity companies issue "informational" 1099 forms even for completely tax-free payments, with zeros in every box. Recipients figure it's a mistake and throw them away. Fast forward to an audit five years later—now they can't prove what those forms actually said. Save everything, zeros included.

Voluntarily reporting tax-free money. The flip side: people see $3,500 land in their checking account monthly and panic, thinking they must report it. They pay tax on money that was never taxable. The IRS won't stop you from overpaying. Getting that money back means filing amended returns, which creates months of delays and extra work.

Losing papers during major life events. Divorce, moving across the country, a parent's death—these shake up where documents get stored. One recipient kept his settlement paperwork in boxes at his mom's house. When she moved into assisted living, his sister cleaned out the garage and donated everything to charity without checking. He spent six months piecing together records from his lawyer, the court, and the annuity company.

Calling the wrong company for help. Your monthly checks come from an annuity company, but the defendant's insurance company arranged the purchase. When you need copies of old documents, calling the defendant's former attorney wastes everyone's time—they left the case years ago and have no access to current records.

Ignoring small interest amounts. Maybe your $500 monthly payment earned $12 in interest one year because payments arrived late. That $12 is taxable. Seems too small to bother reporting? The IRS computers catch every unreported 1099-INT automatically. The penalty and interest charges on $12 might exceed the original tax you owed by the time they're done with you.

Author: Andrew Halvorsen;

Source: avayabcm.com

Obtaining Missing or Replacement Tax Documents from Your Annuity Provider

Contact the structured settlement department specifically, not the general customer service number. Representatives in the settlement department understand your unique situation. Have your claim number, Social Security number, and settlement date ready before you call.

Most companies provide duplicate 1099 forms within two weeks at no charge. Federal regulations require them to maintain these records for a minimum of four years. Older forms might take longer or involve a small fee—usually $25 to $50.

Company mergers complicate things. Your payments continue automatically when your annuity company gets acquired, but tracking down historical records gets messier. Check your most recent payment statement for the current company name. Call them and explain you need records from before the merger. They're legally obligated to maintain predecessor companies' files.

Sometimes record-keeping systems don't integrate smoothly after acquisitions. Your request might bounce between departments. Document every conversation: date, time, name of whoever you spoke with, what they promised. Be persistent. If phone calls go nowhere after two weeks, escalate to a supervisor or compliance officer.

For settlements over a decade old, the original company might not exist anymore as a separate entity. Try contacting your attorney if they're still practicing. Check your state insurance department's website—they maintain public records of every insurance company merger and can point you to the successor company.

Request documents in writing if phone calls fail. Send an email or certified letter creating a paper trail. Written requests often route to compliance departments with strict response deadlines, producing faster results than phone tag.

Author: Andrew Halvorsen;

Source: avayabcm.com

When You Need Professional Help with Settlement Tax Documentation

Some situations are too tangled for DIY approaches. If your settlement agreement doesn't clearly separate taxable from non-taxable portions, a tax attorney can review the wording and provide a written opinion on proper reporting. This opinion doesn't bind the IRS, but it demonstrates good-faith effort to comply, which matters during disputes.

I see the same pattern repeatedly in my practice. Attorneys negotiate excellent settlement amounts but overlook the tax documentation requirements. Clients come to me years later having filed incorrect returns because they didn't understand which portions were taxable. By then we're filing amended returns, requesting penalty abatement, and writing detailed explanations to the IRS. An hour of tax planning during settlement negotiations would have prevented thousands in professional fees down the road

— Michael Torres

Receive an IRS notice questioning your settlement income? Don't respond without professional guidance. These notices have tight deadlines—usually 30 days—and your response determines whether this resolves quickly or escalates into a full audit. A tax professional experienced with settlement documentation can draft responses that satisfy IRS concerns while protecting your rights.

Budget $300 to $500 for a CPA to review your documents and advise on proper reporting. Need representation during an audit? Expect $2,000 to $10,000 depending on complexity. Tax attorneys generally cost more than CPAs but provide attorney-client privilege, which becomes valuable if litigation seems possible.

Situations that warrant professional help:

- Your settlement agreement doesn't specify what you're being compensated for

- You got a 1099 form but believe your settlement qualifies as tax-free

- The IRS sent a notice claiming you underreported income

- Your settlement covered both physical injury and non-physical claims (defamation, emotional distress, lost reputation)

- You sold future settlement payments for a lump sum and don't know how to report that transaction

- The annuity company refuses to provide documentation or claims they've lost your records

Frequently Asked Questions About Structured Settlement Tax Documents

Managing structured settlement tax documents isn't fun. Nobody gets excited about filing systems. But proper documentation protects the financial security your settlement was meant to provide.

Build your system immediately after receiving your first payment. Create redundant backups: physical copies in a fireproof safe, scanned copies in cloud storage, and an additional set with a trusted family member or attorney. Redundancy prevents disaster when any single storage method fails.

Review records annually, preferably in January when new 1099 forms arrive. Verify amounts match your actual deposits. Confirm the annuity company has your current address and correct taxpayer ID number. Small discrepancies resolve easily now, not so much during an audit three years later.

Approaching retirement or working on estate planning? Discuss your structured settlement with your financial advisor. These payments continue for your lifetime (or a specified term), and proper documentation ensures your heirs can continue receiving benefits if you die. Your estate planning attorney needs copies of your settlement agreement and assignment to draft appropriate trust provisions.

The time invested in organizing your structured settlement tax paperwork delivers enormous peace of mind. You'll never scramble for documents during tax season. You'll never wonder whether you reported income correctly. You'll never face unexpected penalties because a crucial form went missing. That security is worth more than the few hours required to build a solid filing system.