Split image showing tax-free structured settlement payments on the left versus taxed lump sum from selling settlement on the right with IRS Form 1040

Structured Settlement Tax Implications Before Selling

Content

Your monthly structured settlement checks show up like clockwork—completely tax-free. No 1099 forms. No reporting headaches. Just money in your account that the IRS can't touch.

Then life happens. Maybe the car breaks down beyond repair, or medical bills pile up faster than you can handle. You start thinking: what if I could get all that future money right now?

Here's where thousands of settlement holders hit a painful surprise. That tax-free status? It doesn't follow your money into a lump-sum sale. The purchasing company cuts you a check, everything seems fine, and then tax season arrives with a bill that makes your stomach drop.

Selling future payments isn't just about accepting whatever discount rate the buyer offers. You're fundamentally changing how the IRS treats your money—from protected compensation to taxable income. Your tax bracket might jump. Your eligibility for credits could vanish. And you'll definitely owe Uncle Sam a chunk of that lump sum.

We're going to walk through exactly what happens to your tax situation when you sell. Not vague warnings, but specific consequences with real numbers.

How Structured Settlements Are Taxed vs. How Sales Are Taxed

The IRS treats your regular structured payments completely differently from the lump sum you'd get by selling them. Understanding this split is critical before you sign anything.

Original Settlement Tax Treatment Under IRC Section 104(a)(2)

When Congress wrote Section 104(a)(2) of the Internal Revenue Code, they created a special carve-out for personal injury victims. The law says damages you receive for physical injuries or sickness don't count as gross income—whether you get them all at once or spread over time as periodic payments.

This protection covers your structured settlement's core payments. You got hurt, you sued (or settled), and now you receive compensation. The IRS recognizes that taxing injury victims on money meant to replace lost wages or pay for medical care would be fundamentally unfair.

But here's a detail most people miss: this tax-free treatment only covers the settlement amount itself. Let's say your annuity generates investment returns beyond what was originally promised in your settlement agreement. Those extra earnings? Potentially taxable. Modern structured settlements typically use qualified assignments that prevent this issue, but some older arrangements from the 1990s and early 2000s created tax complications when the annuity performed better than expected.

The policy makes sense when you think about it. Someone rear-ends you, you suffer genuine injuries, and the settlement compensates you for medical bills and lost wages. Why should the government take a cut of that compensation?

What Changes When You Sell Future Payments

Selling transforms everything. You're no longer receiving compensation for your injuries—you're conducting a business transaction.

Think of it this way: you own a valuable asset (the right to receive future tax-free payments). When you sell that asset to a purchasing company, you generate income from the sale. The IRS doesn't care that the underlying payments would have been tax-free. You're selling an income stream, and that sale itself produces taxable income.

This principle holds regardless of how you structure the deal. Selling five years of payments? Taxable. Selling every remaining payment? Taxable. Selling alternate payments and keeping others? Those you sell still generate taxable income.

The tax-free protection attached to your personal injury settlement stays with those specific payments. It doesn't transfer to secondary transactions where you're essentially liquidating an asset for cash. You're not receiving injury compensation anymore—you're receiving payment for selling something valuable you own.

Federal Tax Consequences When You Sell Structured Settlement Payments

This is where the real financial pain hits most sellers. The federal government wants its share of your lump sum, and the tax treatment is less favorable than many people expect.

Ordinary Income vs. Capital Gains Treatment

When you sell stocks you've held for over a year, you pay long-term capital gains tax—maxing out at 20% for most investments. Nice, right? You might expect similar treatment when selling structured settlement payments you've held for years.

The IRS doesn't see it that way. They classify proceeds from these sales as ordinary income, which faces much steeper rates. Ordinary income rates start at 10% for low earners and climb to 37% for high-income taxpayers. The difference between a 20% capital gains rate and a 37% ordinary income rate means potentially giving up nearly twice as much to taxes.

Tax professionals have challenged this classification in court, arguing that the right to future payments qualifies as a capital asset. The logic seems sound—you're selling something you've owned, not receiving salary or business income. But courts have consistently rejected these arguments. The prevailing legal interpretation treats the sale as accelerated ordinary income that you would have eventually received anyway, just compressed into one tax year instead of spread across many.

This classification also means you can't benefit from qualified dividend rates or other preferential treatments that apply to investment income. The proceeds get taxed at whatever your marginal rate happens to be based on your total income.

Author: Danielle Morgan;

Source: avayabcm.com

Discount Rate Impact on Your Tax Bill

Let's work through a common scenario. You agree to sell $100,000 worth of future payments. The purchasing company offers you $60,000 today. That $40,000 gap represents the discount—their profit and the time value of money.

Here's the killer: you owe taxes on the entire $60,000 you receive, not on some calculated profit. Many sellers think they can subtract the $40,000 "loss" and only pay tax on the difference. Doesn't work that way.

Your cost basis in those structured settlement payments is zero. You didn't buy them—you received them as legal compensation. With a zero basis, every dollar you get from the sale becomes taxable income. If you receive $60,000, you owe federal income tax on $60,000. Period.

This differs fundamentally from selling a house or stock. When you sell your house for $400,000, you subtract what you paid for it (let's say $300,000) and only owe tax on the $100,000 gain. You had a cost basis because you purchased the property.

You never purchased your structured settlement. No basis equals no subtraction. The full amount is taxable.

Occasionally, complex situations arise where you might have some basis—perhaps you previously reported part of the settlement as income, or the settlement included both tax-free injury compensation and taxable punitive damages. These edge cases require a CPA who specializes in structured settlements to untangle the tax math properly.

| What You're Receiving | Does the IRS Tax It? | What Rate? | How to Report It |

| Your regular monthly settlement checks | No—protected under injury exclusion | Nothing owed | You don't report these at all |

| Cash from selling future payments | Yes—counts as ordinary income | Anywhere from 10% to 37% depending on your bracket | You'll get Form 1099-MISC or 1099-NEC; include on Form 1040 |

| Selling just some of your payments | Yes—same treatment as selling all | Same progressive rates apply | Report it the year you receive the money |

| Interest your annuity earns above the settlement amount | Usually yes—unless properly structured | Regular income rates | Form 1099-INT if it applies |

State-Level Tax Rules for Settlement Sales

Federal taxes hurt enough. Then your state probably wants a piece too.

Most states with income tax simply follow the federal treatment. They define taxable income using the federal definition as their starting point, then apply their own rates. If the IRS considers your settlement sale as ordinary income, your state probably does too.

The pain really adds up in high-tax states. California's top rate hits 13.3%. New York maxes out at 10.9%. Minnesota reaches 9.85%. When you combine these state rates with federal rates, you could be handing over 45-50% of your lump sum to various tax authorities.

Nine states offer relief by imposing no income tax at all: Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming. If you live in one of these states, you'll still owe federal tax but you'll dodge the state bite. New Hampshire taxes dividends and interest but not wages or ordinary income, so settlement sales escape taxation there too.

A few states have explored special provisions for hardship sales—allowing reduced taxation if you can prove genuine financial emergency forced the sale. These provisions remain rare and require extensive documentation. Don't count on them when planning a sale.

Here's an interesting planning point: the state where you live when the sale closes generally determines your state tax liability. Not where you originally got injured, not where the settlement was finalized, not where the purchasing company operates. Your current residence controls.

This creates a potential planning opportunity if you're already considering relocation. Moving from California to Nevada before selling could save you over $13,000 in state tax on a $100,000 sale. Just make sure it's a genuine move—the IRS and state tax authorities scrutinize suspicious timing and might challenge a move that looks purely tax-motivated.

Author: Danielle Morgan;

Source: avayabcm.com

Common Tax Mistakes Settlement Sellers Make

Tax complexity breeds errors. Here are the mistakes that land settlement sellers in hot water most frequently.

Failing to Report the Transaction

Some sellers genuinely don't know they need to report the income. Others know but figure they'll take their chances since the original payments were tax-free.

Both approaches lead to the same bad outcome.

The purchasing company reports the payment to the IRS using Form 1099-MISC or 1099-NEC. The IRS computers match that form against your tax return. When they see a $60,000 payment reported to them but no corresponding income on your Form 1040, the system flags your return automatically.

You'll get a notice months or years later proposing additional tax, plus penalties and interest. The penalties stack up quickly—failure-to-file penalties hit 5% per month, failure-to-pay adds another 0.5% monthly. Interest compounds on top of everything.

"But the company never sent me a 1099!" doesn't work as a defense. You're legally required to report all income whether you receive a form or not. The purchasing company's administrative failure doesn't eliminate your obligation.

The statute of limitations normally gives the IRS three years to audit your return. But when you omit more than 25% of your gross income, that extends to six years. For fraudulent returns with intentional evasion, there's no time limit at all. A large unreported settlement sale could haunt you for years.

Misunderstanding the Discount as a Deductible Loss

This error stems from logical-sounding reasoning. You sold $100,000 in payments for $60,000, losing $40,000 in the process. Shouldn't that loss offset some of your taxes?

The tax code says no. That $40,000 represents the buyer's profit margin and the time value of money—the cost of getting cash now instead of waiting years for the full amount. It's not a deductible loss on your side.

The confusion often comes from comparing settlement sales to stock transactions. If you bought stock for $100,000 and sold it for $60,000, you'd absolutely deduct that $40,000 loss. But you purchased that stock. You didn't purchase your structured settlement—you received it as compensation—which means you have no cost basis to work with.

Claiming this deduction on your return practically guarantees an audit. The IRS sees structured settlement sales regularly and knows exactly how the tax math works. They watch for this mistake.

The hardest thing in the world to understand is the income tax

— Albert Einstein

Not Accounting for Alternative Minimum Tax (AMT)

The Alternative Minimum Tax catches fewer people since 2018's tax reforms raised exemption amounts substantially. But it still lurks as a potential problem for settlement sellers in specific situations.

AMT functions as a parallel tax calculation. You figure your tax the regular way, then calculate it again under AMT rules, and pay whichever amount is higher. AMT adds back certain deductions and applies different rates, ostensibly to ensure wealthy taxpayers can't use loopholes to avoid tax entirely.

A large settlement sale can trigger AMT in two ways. First, the income spike itself might push you into AMT territory. Second, and more commonly, the interaction between the sale proceeds and other deductions creates problems. State and local tax deductions get limited under AMT. If you're already claiming large state tax deductions and then add a big lump sum from a settlement sale, the AMT calculation might produce a higher tax bill than the regular method.

Most people selling settlements under $100,000 won't hit AMT issues. But if you're selling a large structured settlement while also claiming significant itemized deductions, ask a tax professional to run the AMT calculation before you commit to the sale.

Author: Danielle Morgan;

Source: avayabcm.com

How to Calculate Your Tax Liability on a Structured Settlement Sale

You need actual numbers before you sign a purchase agreement. Here's how to estimate what you'll owe.

Start with the gross amount you're getting. The purchase agreement should state this clearly. Let's use $60,000 as our example. That's your taxable amount—not some net figure after phantom deductions.

Next, total up your other income for the year. W-2 wages, self-employment income, investment income, pension payments—everything. Suppose that comes to $55,000.

Add them together: $55,000 + $60,000 = $115,000 total taxable income (assuming standard deduction for simplicity).

Now apply the federal tax brackets. A single filer pays: - 10% on income up to $11,600 - 12% on income from $11,601 to $47,150

- 22% on income from $47,151 to $100,525 - 24% on income from $100,526 to $191,950 - Higher rates kick in above that

Your first $11,600 gets taxed at 10% = $1,160. The next chunk ($11,601 to $47,150) totals $35,549 taxed at 12% = $4,266. The portion from $47,151 to $100,525 equals $53,374 taxed at 22% = $11,742. Finally, the amount from $100,526 to $115,000 is $14,474 taxed at 24% = $3,474.

Total federal tax: approximately $20,642.

Now calculate what you would have owed without the settlement sale—just on your $55,000 regular income. Following the same bracket progression, that comes to roughly $6,168.

The difference ($20,642 - $6,168 = $14,474) represents the additional federal tax triggered by selling your structured settlement.

| What You're Selling | Dollar Amount | Tax Treatment Details |

| Total face value of payments over 10 years | $100,000 | Doesn't directly affect your tax calculation |

| Lump sum the buyer pays you | $60,000 | This entire amount counts as ordinary income |

| The discount (what you "lost") | $40,000 | You can't deduct this—it's not a tax loss |

| What gets added to your income | $60,000 | Combined with your other earnings for the year |

| Extra tax if it lands in the 24% bracket | $14,400 | Rough estimate if most falls in this bracket |

| Extra tax if it pushes you into 32% | $19,200 | Happens if you already had high income |

This example simplifies by assuming nice clean bracket boundaries. Real calculations get messier because your income typically spreads across multiple brackets. The first dollars from the sale might get taxed at 22%, the middle portion at 24%, and the top portion at 32% if your income reaches that high.

Don't forget state income tax. If you live in a state with a 5% income tax rate, add another $3,000 ($60,000 × 5%) to your total tax bill.

Also watch for indirect effects. Higher income can phase out tax credits like the Earned Income Tax Credit, child tax credit, or education credits. It might reduce your eligibility for premium tax credits if you buy health insurance through the marketplace. These secondary impacts can add thousands to the true cost of selling.

Tax Reduction Strategies and Timing Considerations

You can't eliminate the tax hit, but smart planning cuts it substantially. The key is using the progressive tax structure to your advantage.

Spreading Sales Across Multiple Tax Years

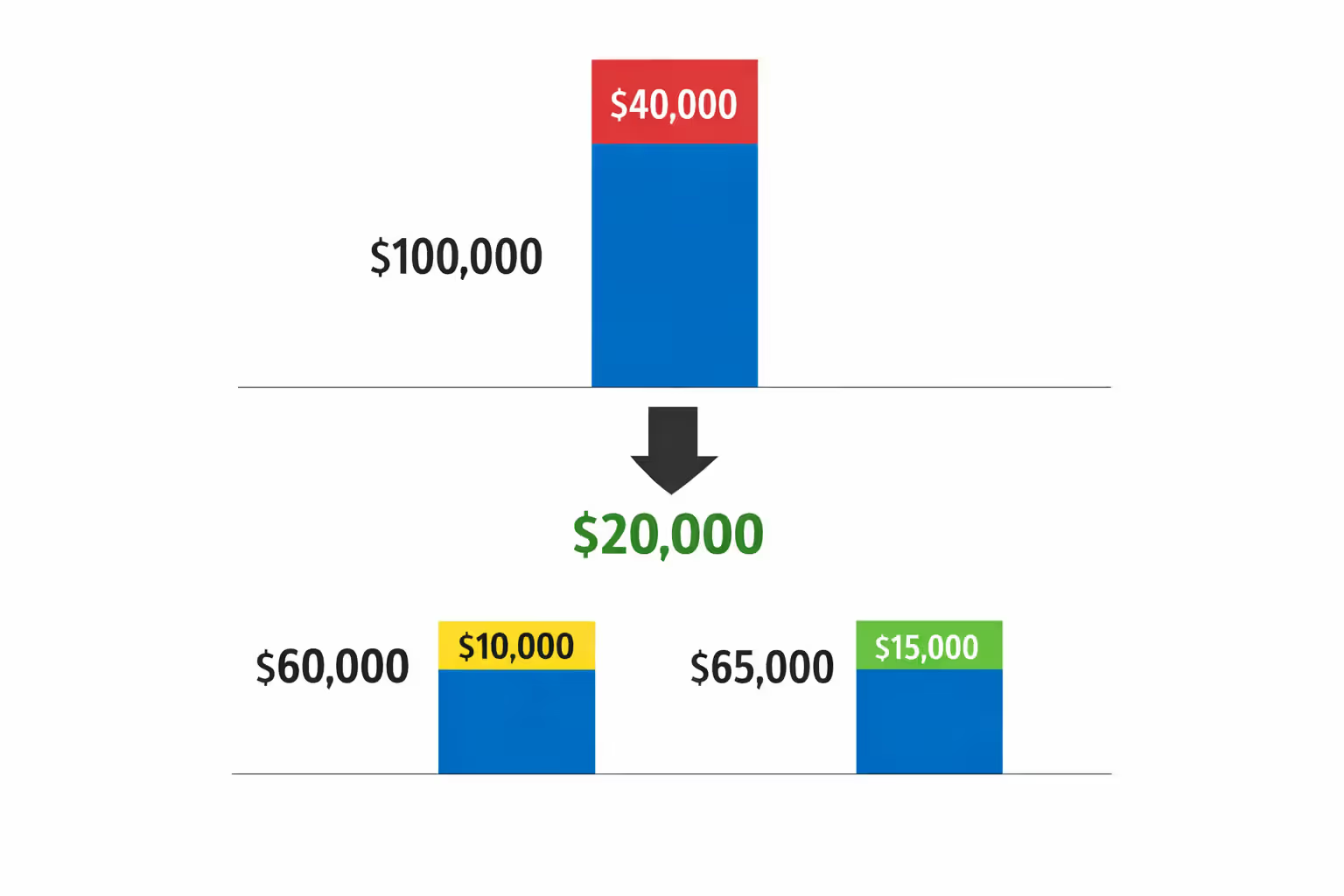

Instead of dumping all your future payments in one sale, what if you sold half this year and half next year?

Say you need $120,000 total. Selling everything at once adds $120,000 to this year's income. If you're currently earning $50,000, your total income jumps to $170,000, pushing a large portion into the 32% bracket.

Alternative approach: sell enough payments this year to receive $60,000, then sell more next year for another $60,000. Each year, you add $60,000 to your $50,000 base income, totaling $110,000 annually. This keeps more of the settlement proceeds in the 24% bracket instead of the 32% bracket, saving you 8% on a significant chunk of money.

The math on a $60,000 amount falling in 32% versus 24% bracket saves you roughly $4,800. Not nothing.

This strategy requires flexibility—you need to not urgently require all the money immediately. You'll also need a purchasing company willing to structure multiple separate transactions, which might affect their discount rates. But if you can swing it, the tax savings make it worthwhile.

Important caveat: spreading sales doesn't reduce the per-dollar tax rate, it just prevents bracket creep. Every dollar still gets taxed eventually. You're playing defense against the progressive tax structure, not eliminating taxation.

Author: Danielle Morgan;

Source: avayabcm.com

Coordinating with Other Income Events

Timing a settlement sale requires zooming out to view your complete income picture.

Planning to retire mid-year? You'll only have six months of W-2 wages. Selling structured settlement payments in that half-year of retirement means the proceeds fill lower tax brackets that your partial-year wages left empty. Someone earning $80,000 annually who retires in June will only show $40,000 in wages for the year. Selling settlements later that year could generate $50,000 that mostly stays in the 22% bracket instead of jumping to 32%.

Between jobs? Taking a year off to handle family matters? Starting a business that hasn't generated income yet? These low-income years create opportunities to sell at reduced tax cost.

Flip side: avoid selling in years when you already have income spikes. Getting a big bonus at work? Selling your house for a large capital gain? Receiving an inheritance that includes traditional IRA distributions? Don't pile a settlement sale on top of those events. You'll guarantee that every dollar from the settlement gets taxed at your highest marginal rate.

Major medical expenses create another planning angle. You can deduct medical expenses exceeding 7.5% of your adjusted gross income. If you face $50,000 in medical bills and normally earn $60,000, you'd only deduct expenses above $4,500 (7.5% of $60,000). But if you sell settlement payments for $60,000 in the same year, your AGI jumps to $120,000, meaning expenses only count above $9,000. This actually hurts you by raising the threshold.

However, if the medical expenses are truly extraordinary—say $80,000—then the higher AGI from a settlement sale doesn't eliminate the deduction entirely, just reduces it. In rare cases with massive deductible medical costs, the deduction can offset some of the tax impact from the sale.

One critical point: don't let the tax tail wag the financial dog. If you're facing foreclosure, can't pay for critical medical treatment, or need money to prevent genuine catastrophe, the tax consequences become secondary. Pay the taxes and solve the crisis. But when you have breathing room and flexibility, strategic timing saves real money.

Frequently Asked Questions About Structured Settlement Sale Taxes

Selling structured settlement payments converts tax-protected income into taxable income. There's no way around this fundamental reality.

The entire lump sum you receive—not some net amount after subtracting the discount—gets taxed as ordinary income. Combined federal and state rates can approach 40-50% in high-tax states. You can't deduct the buyer's discount. The sale might bump you into higher tax brackets. Other tax benefits you currently receive might vanish when your income spikes.

These consequences don't automatically mean selling is wrong. Sometimes you need cash now, and paying taxes is simply the cost of accessing your money early. Medical emergencies, preventing foreclosure, avoiding bankruptcy—these genuine crises can justify selling despite the tax hit.

But you need accurate numbers before you commit. Don't just look at the gross lump sum. Calculate the after-tax amount you'll actually keep. Factor in both federal rates and your state's income tax. Consider whether selling across multiple tax years could save thousands by preventing bracket creep.

If you're selling more than $50,000, spending a few hundred dollars on a CPA familiar with structured settlements is money well spent. They can run precise calculations including AMT exposure, identify whether timing the sale differently would help, and make sure you understand the complete tax picture.

The court approval process required in most states examines whether the sale serves your best interests, but judges rarely dig deep into tax implications. That analysis falls on you. Do it thoroughly. Ask questions until you completely understand how much goes to taxes versus meeting your actual financial needs.

Run the numbers. Plan the timing strategically if you have flexibility. And make sure the after-tax proceeds actually solve the problem you're trying to address. Otherwise you'll hand over thousands to the IRS while still falling short of your goal.