Settlement documents, IRS tax forms, calculator, and scales of justice on a professional desk — structured settlement tax deduction concept

Structured Settlement Tax Deductions Guide for Recipients and Payers

Content

Tax confusion around structured settlements? You're not alone. Here's what catches most people off guard: recipients typically don't pay a dime in taxes on injury settlements, while payers—defendants and insurance companies—navigate a maze of rules about what they can actually write off.

This disconnect creates problems. Settlement recipients sometimes report tax-free payments as income (and pay unnecessary taxes). Defendants structure deals incorrectly and lose legitimate deductions. Both sides make documentation mistakes that invite IRS scrutiny five years down the road.

The stakes are high. We're talking about the difference between keeping your entire settlement versus surrendering 30-40% to taxes. For payers, it's about claiming $100,000+ in deductions versus leaving money on the table or facing penalties for improper claims.

Are Structured Settlement Payments Tax-Deductible?

Here's where things split completely depending on your role.

For Settlement Recipients

Most people receiving structured settlements won't claim any deductions. Why? They're not paying taxes in the first place.

IRC Section 104(a)(2) excludes payments for physical injuries and sickness from your taxable income. This means every dollar you receive goes straight into your pocket—no tax withholding, no April 15th reckoning.

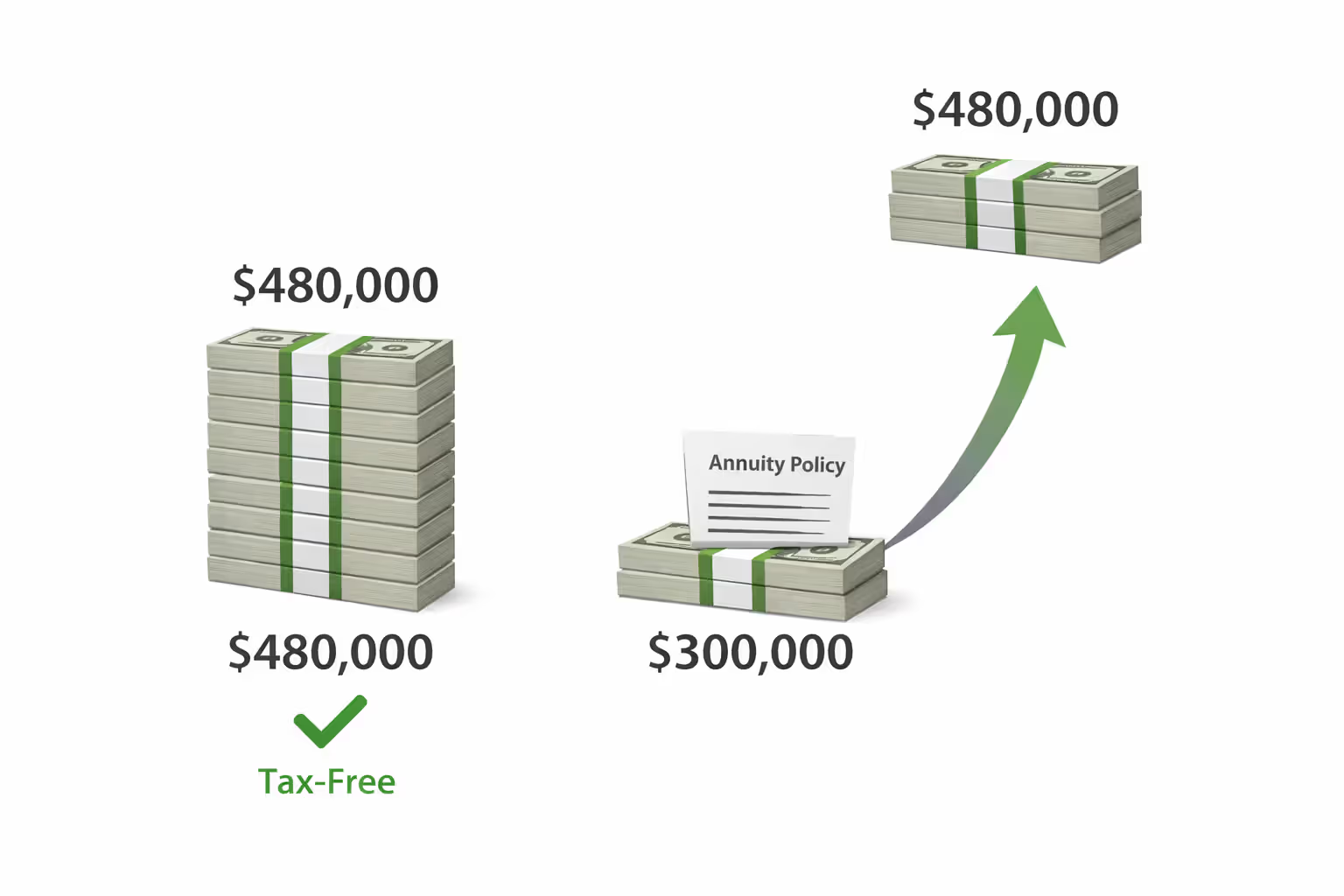

The exclusion sweeps broadly. Take a settlement structured to pay $2,000 monthly over 20 years. Total payments: $480,000. But the insurance company only deposited $300,000 into an annuity to fund those payments. That $180,000 difference? It represents growth inside the annuity, and you pay zero taxes on it. The IRS doesn't want to see it on your return. There's nothing to deduct because you're reporting nothing.

Author: Christopher Vaughn;

Source: avayabcm.com

Now, settlements for non-physical claims work completely differently. Let's say you won an age discrimination case against your former employer. Those periodic payments arrive as fully taxable ordinary income. Every payment increases your tax bill, just like a paycheck would. The growth element gets taxed as interest income. And here's the kicker—you don't get to "deduct" receiving this money. It simply adds to your gross income for the year.

For Settlement Payers (Defendants and Insurers)

Defendants approach this from the opposite direction. Can they write off what they're paying out?

For businesses, usually yes. A trucking company settles a crash case for $500,000. That's an ordinary business expense under IRC Section 162—same category as equipment repairs or employee salaries. The structured format doesn't eliminate this deduction, though it affects timing.

Here's a real-world example: A manufacturing plant settles a workplace injury case. They use a qualified assignment (more on this shortly) and pay $400,000 upfront to an assignment company. The assignment company then makes payments to the injured worker over 15 years. The manufacturer typically deducts that full $400,000 in the year they paid it. Done.

Author: Christopher Vaughn;

Source: avayabcm.com

Individual defendants face tighter restrictions. Got sued personally for a fender bender? You can't deduct the settlement payment. The IRS treats this as a personal expense—like buying groceries or paying your electric bill. No business activity means no business deduction.

The qualified assignment structure under IRC Section 130 adds complexity worth understanding. When defendants transfer their payment obligation to a specialized assignment company, they accelerate their deduction while preserving tax-free status for recipients. The assignment company purchases an annuity to fund the payments and owns the obligation going forward. This three-party arrangement delivers tax benefits to everyone—if structured correctly.

IRS Rules Governing Structured Settlement Tax Treatment

Two big dividing lines determine how the IRS treats your settlement: what kind of injury we're talking about, and whether the payment structure meets specific technical requirements.

Physical Injury vs. Non-Physical Injury Claims

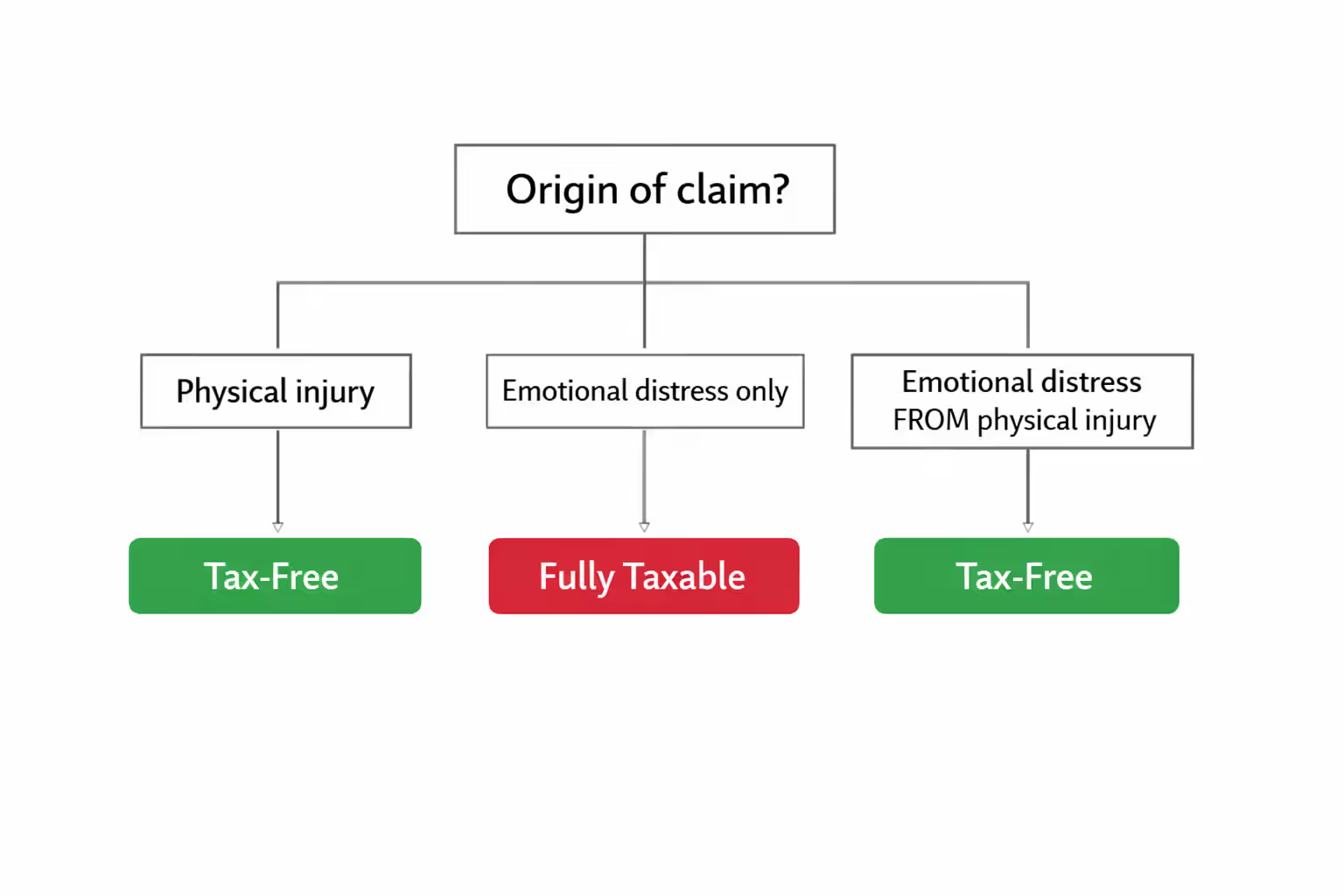

The "physical injury" requirement creates a bright line that controls everything downstream.

Physical injuries mean observable, diagnosable medical conditions. Broken bones qualify. Lacerations qualify. Burns, traumatic brain injuries, disk herniations, torn ligaments—all qualify. Your doctor can see them, measure them, document them in medical records.

Emotional distress typically doesn't qualify, even when it manifests physically. Stress headaches from workplace harassment? Taxable settlement. Insomnia from defamation? Taxable. Stomach ulcers from employment discrimination? Still taxable—unless they stem from an underlying physical injury.

Here's where it gets tricky. Say you're in a car accident that breaks your leg and gives you PTSD from the trauma. The entire settlement—covering both the leg and the psychological injury—stays tax-free because the emotional harm flows from a physical injury. But an employee who develops anxiety attacks from sexual harassment receives a fully taxable award, even if that anxiety later triggers a heart condition. The emotional distress came first, before any physical manifestation.

Sexual harassment and discrimination cases illustrate this harsh reality. Despite causing genuine, documented harm, these settlements generate ordinary taxable income. A harassment victim who ends up hospitalized for stress-induced cardiac problems might exclude the portion directly related to the heart event, but everything compensating for emotional suffering gets taxed at regular rates.

| Settlement Category | Recipient's Tax Treatment | Can Payer Deduct? | Relevant Tax Code | Real-World Examples |

| Physical injury/sickness | Excluded completely from income | Business defendants: Yes; Individuals: Generally no | IRC 104(a)(2) | Auto crashes, medical malpractice, slip-and-fall injuries, defective product burns |

| Standalone emotional distress | Taxed as ordinary income | Business defendants: Yes; Individuals: Rarely | IRC 61 | Workplace harassment without physical injury, defamation, intentional infliction of emotional distress |

| Employment discrimination | Taxed as ordinary income | Business defendants: Yes (some limits apply) | IRC 61 | Termination for age/race/gender, retaliation, hostile work environment |

| Punitive damages (any case) | Always taxed as ordinary income | Business: Sometimes; Individuals: No | IRC 104(a)(2) specifically excludes | Any case awarding punitive damages |

| Lost earnings component | Taxed even within physical injury cases | Business: Yes; Individuals: No | IRC 104(a)(2) specifically excludes | Back pay, future wage capacity, lost business income |

Periodic Payment Requirements Under IRC 130

IRC Section 130 created qualified assignments—the mechanism letting defendants shift their payment obligations to third-party companies while preserving favorable tax treatment on both sides.

For an assignment to qualify, it must involve periodic payments for claims excludable under Section 104(a)(2). Translation: physical injury cases only. The assignment paperwork must prohibit acceleration, deferral, or increases except in narrow situations. The recipient can't control or access the underlying funding asset—typically an annuity the assignment company purchases.

Qualified assignments don't work for taxable settlements. You can absolutely structure employment discrimination payments or contract breach damages over time, but the special IRC Section 130 tax benefits don't apply. Recipients pay tax on payments as received. Payers deduct costs according to their regular accounting method (cash or accrual).

The "periodic payment" requirement means genuine installments, not creative delays. Payments need to occur at least once yearly, though monthly or quarterly schedules are standard. A settlement paying nothing for five years then one balloon payment? Doesn't qualify. A structure where the recipient can call the annuity company and demand different payment timing? Doesn't qualify either.

When Structured Settlement Deductions Apply: Eligibility Criteria

Who can actually claim deductions? The answer depends on who's paying, why they're paying, and how they've documented the arrangement.

Business Expense Deductions for Defendants

Businesses write off settlement costs when they arise from income-producing activities and meet the "ordinary and necessary" expense test. A restaurant settling a customer's food poisoning lawsuit? Deductible business expense. A manufacturer resolving product liability claims? Same thing.

Timing depends on your accounting method and payment structure. Cash-basis businesses deduct expenses when actually paid. If they fund a structured settlement through a qualified assignment, they typically deduct the entire assignment purchase price immediately. Accrual-basis businesses deduct when the liability becomes fixed and determinable—usually when everyone signs the settlement agreement—regardless of when cash changes hands.

C corporations hit a special restriction with punitive damages. IRC Section 162(g) blocks deductions for punitive damages paid following criminal conviction, guilty pleas, or settlements with government agencies. This rule targets corporate misconduct but creates gray areas. Punitive damages in purely private civil cases between businesses or individuals generally remain deductible, though recent tax law shifts have muddied these waters.

The qualified assignment structure under IRC Section 130 provides the cleanest path for business defendants to claim immediate deductions while preserving tax-free treatment for injury victims. But it only works when the underlying claim qualifies for Section 104(a)(2) exclusion—physical injury cases. Businesses settling employment claims or contract disputes need different strategies

— Sarah Chen

Self-employed individuals and partnerships deduct settlement costs on Schedule C or as partnership expenses, following the same ordinary-and-necessary standard. A self-employed contractor settling a customer's job-site injury deducts the cost. Personal settlements for individuals—regardless of wealth—generate no deduction.

Attorney Fee Deductions and Limitations

Attorney fees create a nasty secondary tax problem, especially for plaintiffs in taxable settlements. When your settlement gets taxed, the IRS initially treats the gross amount—including what your lawyer takes home—as income to you, even under contingency arrangements.

Physical injury cases dodge this bullet entirely. The whole settlement including attorney fees escapes taxation. But employment discrimination or other taxable claims? Brutal. You pay tax on the full settlement amount, then scramble to deduct attorney fees.

The Tax Cuts and Jobs Act (2017) eliminated miscellaneous itemized deductions—including attorney fees—for tax years 2018 through 2025. Congress carved out one narrow exception: employment claims and certain whistleblower awards can claim an above-the-line deduction on Schedule 1. This prevents you from paying tax on money that went straight to your attorney.

But the exception only covers unlawful discrimination claims, not every employment dispute. Wrongful termination for race, age, gender, disability, or other protected characteristics qualifies. Simple breach of your employment contract? Doesn't qualify. Plaintiffs in non-qualifying cases might pay tax on their attorney's 40% contingency share with zero offsetting deduction—a nightmare scenario that makes settlement negotiation critical.

Defendants writing off settlement costs also deduct their own legal fees as business expenses, assuming the same ordinary-and-necessary standard applies. Defense attorney fees in commercial litigation? Fully deductible. Personal legal fees for individual defendants? Typically not.

Common Mistakes That Disqualify Tax Benefits

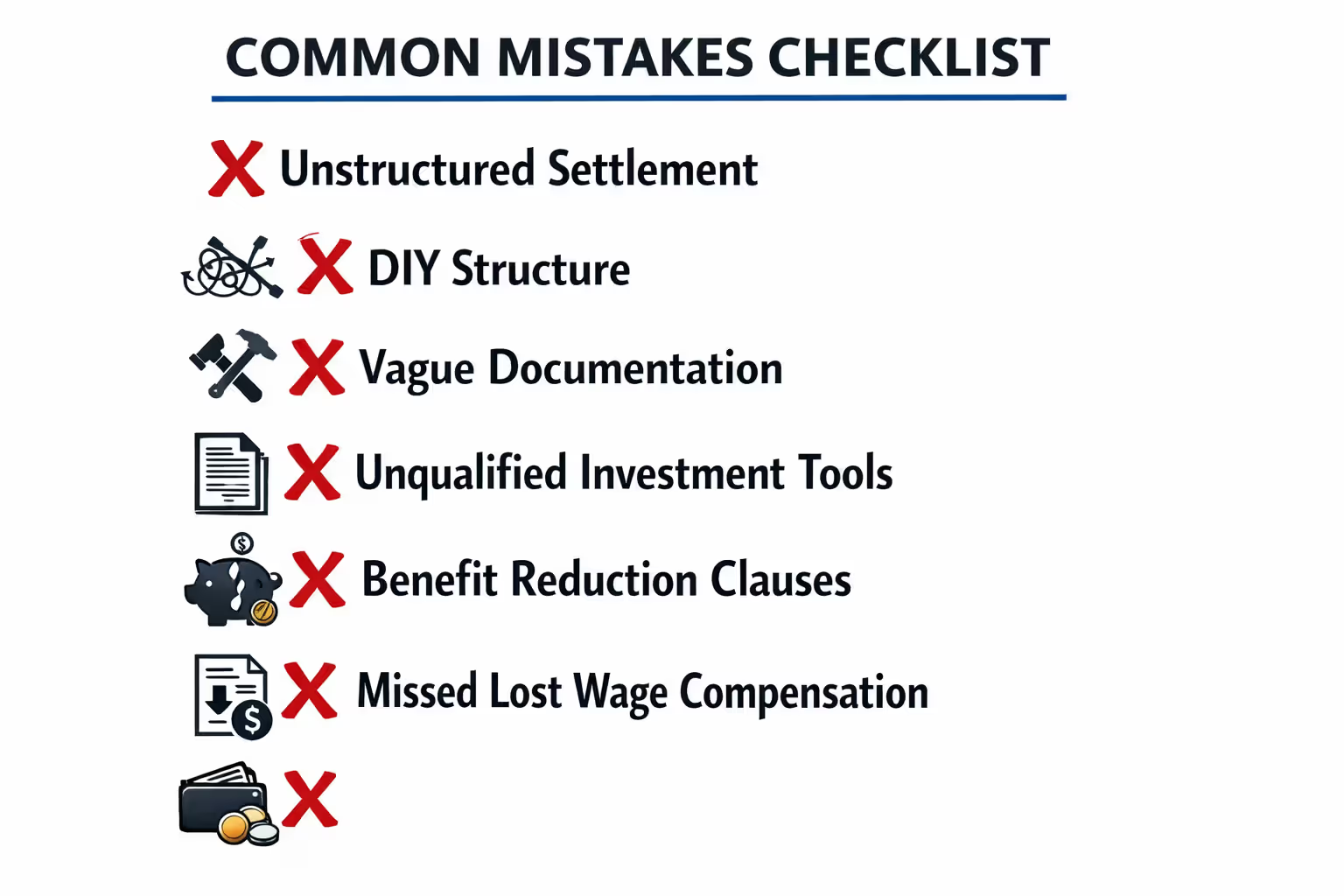

Small structural or documentation errors can torch tax advantages for everyone involved.

Lumping everything together without allocation: Settlement agreements that combine physical injury damages, emotional distress, lost wages, and punitive damages into one number create tax disasters. The IRS demands reasonable allocation among taxable and non-taxable components. Without it, your entire settlement risks being treated as taxable. Settlement paperwork should break out specific dollar amounts for each damage category based on the actual facts.

DIY structured settlements: Defendants who skip qualified assignment companies and just promise to pay over time miss the tax benefits and create risks. The defendant stays on the hook, can't claim an immediate deduction for present value, and might accidentally trigger taxation for the recipient if the structure looks like a loan or deferred compensation. Only qualified assignment companies meeting IRC Section 130's technical requirements deliver the intended tax treatment.

Vague or missing documentation: The IRS won't take your word that a settlement involved physical injuries. You need medical records, complaint allegations, and crystal-clear settlement language documenting the physical injury foundation. Generic settlement agreements describing "all claims" without specifics invite IRS challenges three years later when memories have faded and witnesses have scattered.

Using non-qualified funding vehicles: Some defendants try funding with corporate bonds, mutual funds, real estate, or other investments instead of annuities. Bad idea. These arrangements may give recipients constructive receipt of the funding asset, triggering immediate taxation of the entire present value. Qualified assignments must use annuities from highly-rated life insurance companies meeting specific regulatory standards.

Payment modification clauses: Settlement agreements letting recipients accelerate payments, grab lump sums, or modify the schedule disqualify the structure. Once signed, payment terms must stay locked except for narrow exceptions like death benefits to named beneficiaries.

Forgetting the lost wages component: Even in physical injury cases, amounts compensating for lost earnings are taxable. A $500,000 settlement for a car accident that includes $100,000 for two years of missed work means $100,000 shows up as taxable ordinary income. Failing to report this slice invites penalties and interest.

Author: Christopher Vaughn;

Source: avayabcm.com

How Selling Your Structured Settlement Affects Tax Status

Sometimes structured settlement recipients need cash now and approach factoring companies that purchase future payments at steep discounts. These transactions carry tax implications beyond the obvious loss of income.

For physical injury settlements originally excluded under Section 104(a)(2), selling payment rights generally doesn't create taxable income. You're selling a capital asset—your right to future tax-free payments—and proceeds typically remain tax-free. You're not recognizing gain because your basis in the payment stream equals the payments' present value.

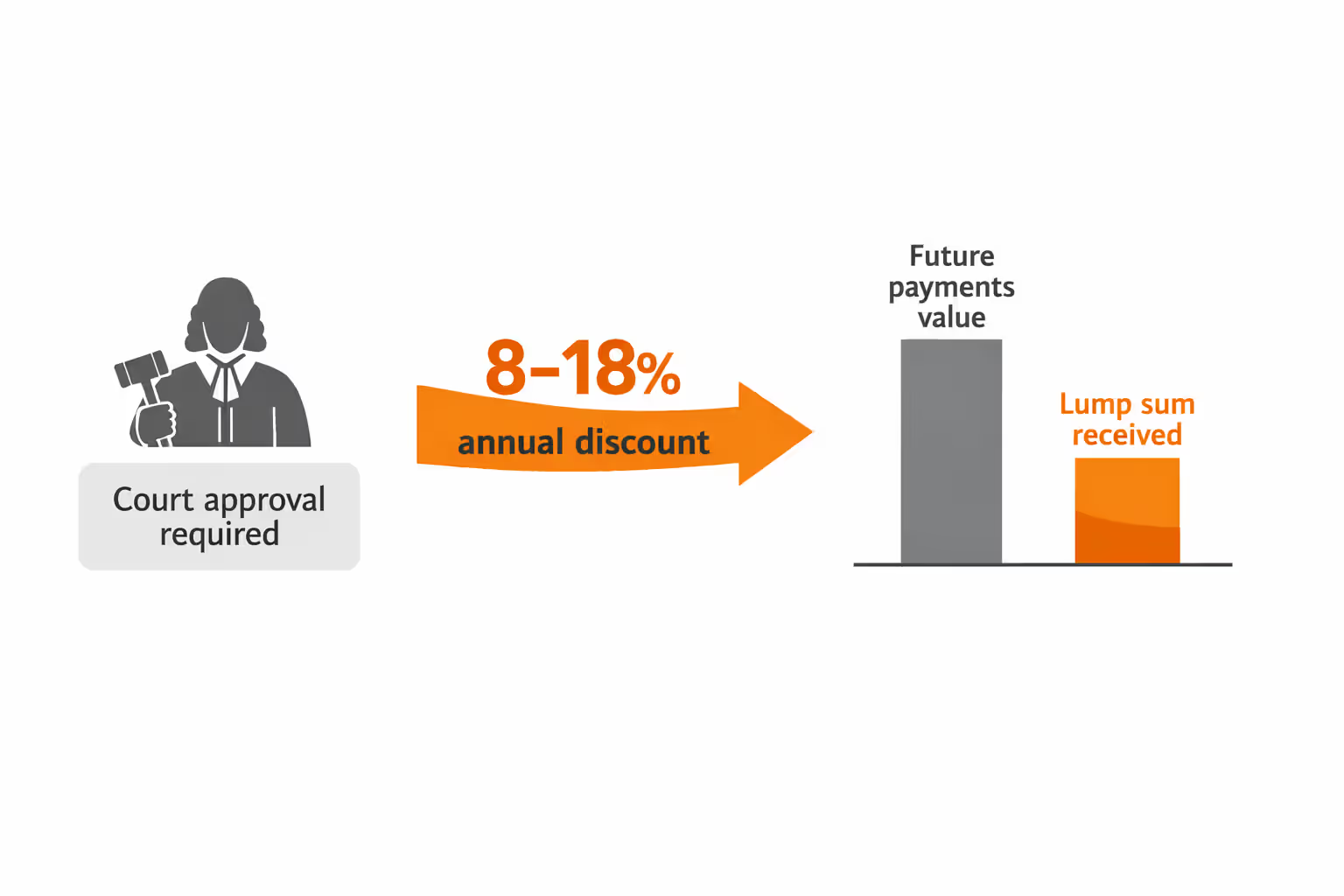

But IRC Section 5891 slaps a 40% excise tax on factoring companies buying structured settlement rights without court approval. This tax hits the factoring company, not you, but it dramatically shrinks the market. Reputable buyers won't touch your payments without going through court approval required by state structured settlement protection laws.

The court approval requirement exists to shield recipients from predatory deals. Judges examine whether the sale serves your best interest, whether the discount rate seems reasonable (typically 8-18% annually, which is aggressive), and whether you truly understand what you're giving up. This process adds weeks or months and legal costs, further reducing your net proceeds.

Selling taxable structured settlements—those from employment cases or other non-physical claims—triggers different tax treatment. These sales may generate capital gains or ordinary income depending on transaction structure. If you're receiving taxable periodic payments and sell future payment rights, the IRS might treat that lump sum as accelerated ordinary income rather than a capital transaction. Your entire tax bill arrives immediately instead of spreading across years.

State law piles on additional requirements. Most states restrict or ban structured settlement sales without court approval, regardless of federal tax treatment. Violating these statutes can void the transaction, leaving you without the lump sum but also without the future payments you thought you'd sold.

Author: Christopher Vaughn;

Source: avayabcm.com

Documentation Requirements for Claiming Settlement-Related Deductions

Proper documentation separates legitimate deductions from IRS audit disasters.

Settlement agreements: Your core document must describe with specificity what claims are being settled. Generic "all claims arising from the incident" language provides zero proof of physical injury. You need explicit references to bodily injuries, medical treatment received, physical symptoms documented, and ongoing physical limitations. For defendants claiming business deductions, the agreement should establish the business context and demonstrate why this expense qualifies as ordinary and necessary.

Qualified assignment agreements: When using IRC Section 130 qualified assignments, you need both the release agreement and a separate assignment agreement. The assignment document transfers the defendant's payment obligation to the assignment company and must satisfy every statutory requirement: periodic payments only, no acceleration rights, qualified funding through approved annuities, and proper assignment company qualifications.

Forms for recipients: Most physical injury structured settlement recipients file nothing special because payments aren't taxable income. Don't report tax-free income. For taxable settlements, you'll receive Form 1099-MISC or 1099-NEC showing annual payment amounts. Include this on Schedule 1 as additional income, and claim allowable attorney fee deductions on Schedule 1, line 24 (assuming you have qualifying employment claims).

Forms for payers: Businesses writing off settlement costs report them as expenses on appropriate forms—Schedule C for sole proprietors, Form 1065 for partnerships, Form 1120 for C corporations, Form 1120-S for S corporations. Exceptionally large settlements might require disclosure on Form 8886 if they constitute reportable transactions. Payers making taxable periodic payments must issue Form 1099-MISC annually.

Medical records and supporting evidence: Maintain comprehensive medical documentation proving the physical injury nature of your claim. Hospital admission records, physician notes, diagnostic imaging reports, physical therapy evaluations, and treatment chronologies all substantiate tax-free status. The IRS can audit returns up to three years after filing (six years for substantial understatement, indefinitely for fraud), so keep these records permanently.

Annuity contracts and assignment documentation: Recipients should receive and preserve copies of the annuity contract funding their payments plus the qualified assignment agreement. These documents prove your structure meets IRS requirements and establish your basis in the payment stream if you eventually sell rights.

Attorney fee agreements and payment tracking: For taxable settlements where you're claiming attorney fee deductions, retain your contingency fee agreement and records documenting what your attorney actually received. Your deduction must match the amount included in your income and genuinely paid to counsel.

Frequently Asked Questions About Structured Settlement Tax Deductions

Structured settlement tax treatment delivers powerful benefits when executed properly but harsh penalties for mistakes. The physical injury exclusion under IRC Section 104(a)(2) provides complete tax relief for accident victims, medical malpractice plaintiffs, and similar claimants—a benefit worth protecting through meticulous settlement drafting and documentation.

Defendants and insurers benefit from qualified assignments delivering immediate deductions while maintaining tax-free status for recipients. These arrangements demand precision: properly qualified assignment companies, approved annuities, and bulletproof documentation. Cutting corners to trim costs typically backfires when the IRS challenges your structure during an audit three to six years later.

The unfavorable tax treatment of non-physical injury settlements—employment discrimination, emotional distress cases, contract disputes—demands different planning entirely. Recipients must factor in full taxation and restricted attorney fee deductions when evaluating settlement offers. A $200,000 physical injury settlement beats a $250,000 employment settlement once you account for taxes eating 30-40% of the larger number.

Before signing any structured settlement agreement, consult both legal counsel and a tax advisor who regularly handles IRC Sections 104, 130, and 5891 issues. Tax consequences are too significant and too permanent to rely on general advice or assumptions. Strategies that work brilliantly for physical injury cases fail catastrophically for employment claims. Structures benefiting defendants might harm recipients when improperly executed.

Maintain comprehensive documentation from settlement signing through the final payment decades later. Medical records, settlement agreements, qualified assignment paperwork, and annuity contracts protect your tax position during audits. The IRS won't accept your uncorroborated claim that a settlement involved physical injuries—you need contemporaneous evidence supporting the tax treatment you've taken.

If you're considering selling structured settlement payments, understand both tax and non-tax costs before proceeding. While physical injury payment sales generally preserve tax-free treatment, the steep discounting, court approval requirements, and state law restrictions make these transactions extraordinarily expensive. Explore alternatives like settlement-backed loans or payment modifications before committing to a sale that permanently eliminates future income security.

Structured settlements represent sophisticated financial and tax planning instruments. Used correctly with qualified professional guidance, they provide tax efficiency, payment security, and long-term financial stability. Used carelessly, they generate unexpected tax bills, disallowed deductions, and expensive IRS disputes that could have been avoided entirely.