Person reviewing structured settlement annuity documents with payment schedules and calculator on office desk

How a Structured Settlement Annuity Works After a Legal Settlement

Content

Most people freeze at this moment. The money is real now, but so is the pressure. Take everything today, or lock into a payment schedule you can't change?

This isn't a decision you can google your way through at midnight. Your financial reality for the next twenty or thirty years depends on understanding exactly what you're choosing—and what you're giving up.

What Is a Structured Settlement Annuity?

Think of a structured settlement annuity as converting your legal award into a personal pension plan. Rather than cashing out $500,000 immediately, you might receive $2,500 every month for twenty years. Or you could set up $50,000 payments landing exactly when your daughter starts college, then shifts to smaller monthly amounts afterward.

Here's what makes it an annuity instead of just a payment plan: the defendant (or more likely, their insurance company) purchases a specialized annuity contract from a highly-rated life insurance carrier. That annuity becomes the engine funding your payments. The insurance company invests the lump sum premium, then pays you according to the schedule everyone agreed to—regardless of market crashes, the defendant's bankruptcy, or any other financial chaos.

This structure took off after 1982, when Congress passed legislation exempting personal injury settlements from federal taxes under Internal Revenue Code Section 104(a)(2). Suddenly, defendants could settle cases for less (since tax-free payments are more valuable than taxable ones), and courts loved that claimants weren't blowing through settlements in eighteen months and ending up on Medicaid.

The data from the 1970s was brutal: roughly one-third of injury victims who took lump sums had spent everything within five years. Many couldn't afford their own ongoing medical care, even though that's exactly what the settlement was meant to cover.

Robert Mansfield, a CFP who's structured over 300 settlements, puts it this way: "I tell clients to forget about the money for a second. Think about your life at 40, at 55, at 70. What expenses hit when? A spinal injury at 35 means different financial pressure points across decades—medical equipment, vehicle modifications, maybe paying someone to mow your lawn eventually. The money should show up when the bills do."

Unlike retirement annuities your financial advisor might recommend, you can't cash these out. Can't borrow against them. Can't use them as loan collateral. That inflexibility is the whole point—and the main source of regret for people who underestimate future cash needs.

How Structured Settlement Annuities Work in Practice

The typical setup unfolds in three distinct phases, though the timeline varies wildly depending on whether you're settling before trial or after a jury verdict.

The Setup Process: From Court Approval to First Payment

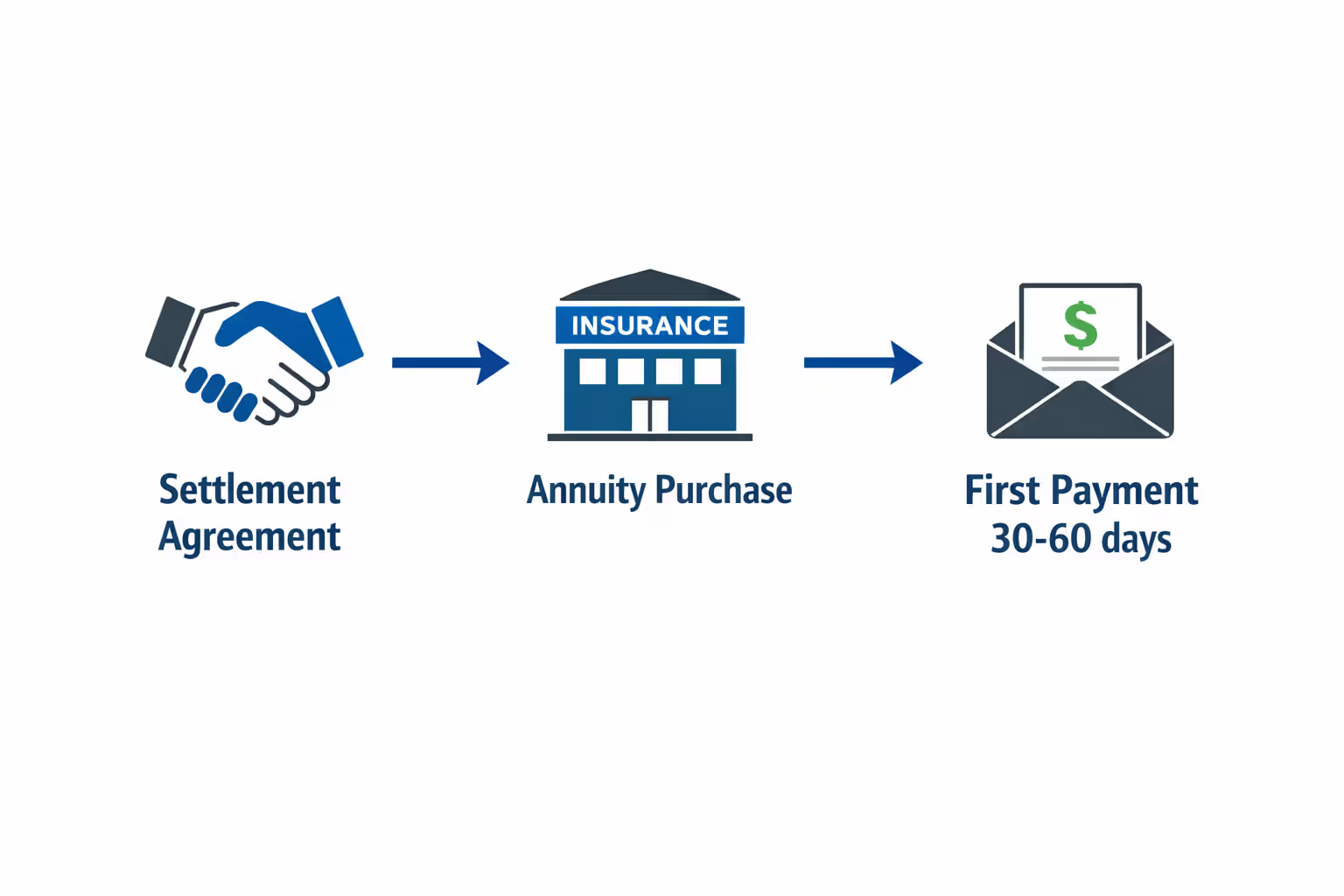

Let's say you've reached a settlement during mediation. Both sides agree your case is worth $750,000. Now comes the architecture phase.

Your attorney typically works with a structured settlement broker (often—and here's where it gets tricky—someone the defense insurer suggests). You specify everything: when payments start, how frequently they arrive, whether amounts stay flat or increase annually, what happens if you die before all payments arrive.

Maybe you need $150,000 immediately for medical bills and legal fees. The remaining $600,000 could become $3,200 monthly for eighteen years. Or perhaps you want smaller monthly payments plus $75,000 lumps every five years for major expenses. The customization options are nearly endless at this stage—and vanish completely once you sign.

After you approve the structure, the defendant buys an annuity from a life insurance company with solid ratings (typically A or better from AM Best). The contract names you as payee, but here's the crucial twist: ownership transfers to what's called a qualified assignment company. This assignment accomplishes two goals—it gets the defendant completely off the hook for future payments, and it preserves your tax-free status under federal law.

For minors and certain adult settlements, courts must approve the arrangement. A judge reviews whether the payment schedule makes sense for your situation. Expect 30-60 days from settlement agreement to first payment arrival. Longer if the court calendar is jammed.

Author: Danielle Morgan;

Source: avayabcm.com

Who Manages the Annuity (Qualified Assignment, Insurers)

You'll probably never talk to anyone at the insurance company issuing your annuity. The qualified assignment company sits between you and the insurer, having assumed the defendant's payment obligations.

Why this matters: if the original defendant files bankruptcy next year or dissolves entirely, your payments continue uninterrupted. The life insurance company—not the defendant—holds the money funding your payments.

Pacific Life, MetLife, New York Life, and Prudential dominate the structured settlement annuity market. These companies maintain separate accounts for structured settlement obligations, adding another security layer beyond their general corporate assets.

Each year, you'll receive statements showing your remaining payment schedule. What you can't do: access the annuity's cash value, surrender it early, or borrow against it. These restrictions are permanently baked into the contract.

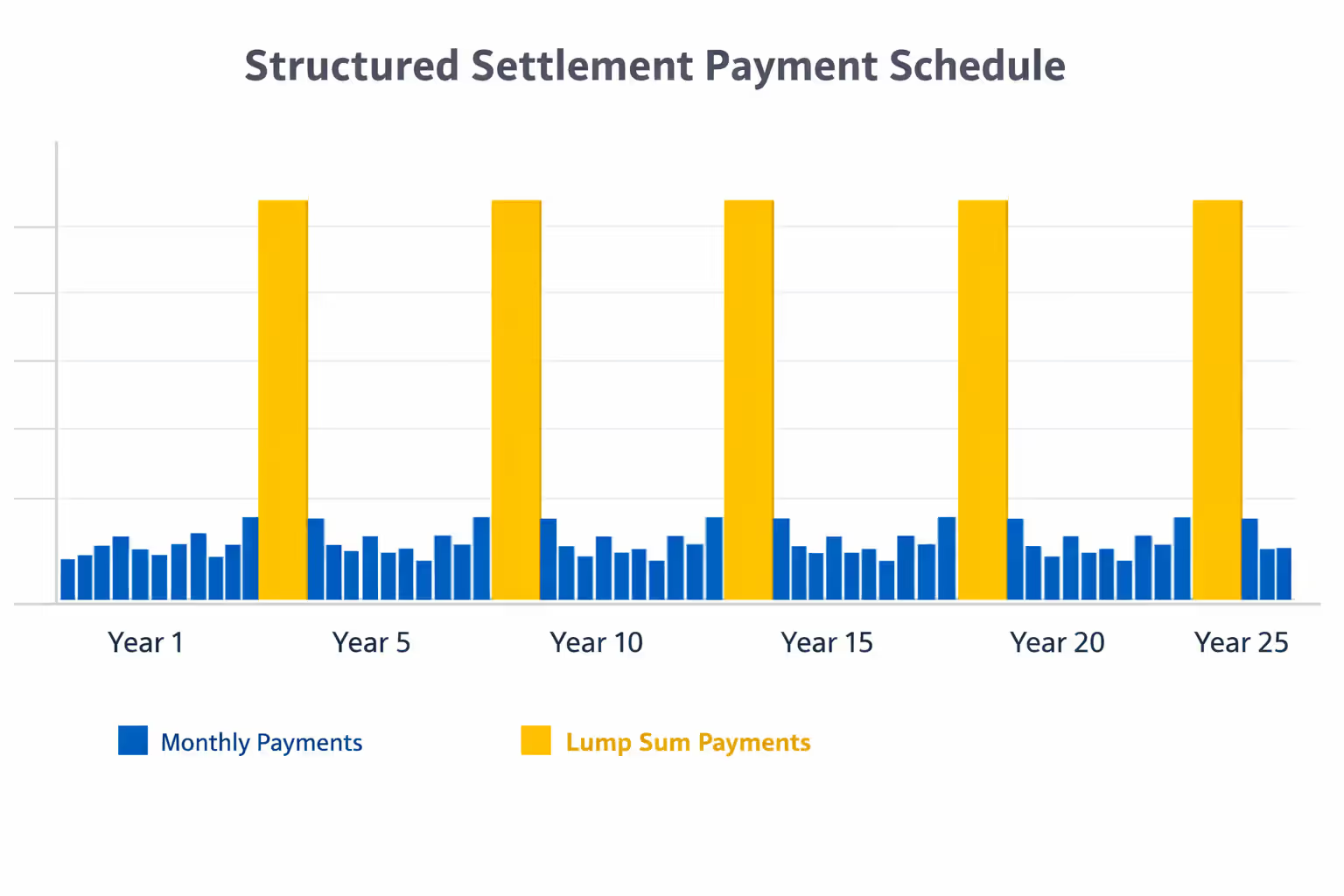

Payment Schedules and Customization Options

Modern structures offer surprisingly creative options during setup. Consider these real-world examples:

Inflation hedges: Annual payment increases of 2-4% offset purchasing power erosion over decades. Start at $2,500 monthly with 3% annual bumps, rather than flat $3,000 payments that feel smaller each year.

Strategic lump sums: $50,000 when your youngest child turns 18. $100,000 when you hit retirement age. $25,000 every five years for vehicle replacements and home maintenance.

Guaranteed payment periods: Payments continue to your designated beneficiaries if you die before the guarantee period ends—10, 20, or 30 years are common.

Lifetime payments: Monthly amounts continue until you die, regardless of whether that's next year or forty years from now. Works like a traditional pension.

Deferred structures: Payments begin five or ten years after settlement, allowing the annuity to grow before distributions start.

A well-designed structure for a 40-year-old receiving $800,000 might include $3,000 monthly for basic living costs, plus $75,000 arriving every five years for larger expenses, with all payments guaranteed for 25 years minimum. If she dies in year 12, her kids receive the remaining 13 years of payments.

Author: Danielle Morgan;

Source: avayabcm.com

Types of Structured Settlements That Use Annuities

These annuity arrangements show up most frequently in five legal resolution categories:

Personal injury settlements represent the majority—probably 70% or more. Car wrecks, slip-and-falls, defective product cases, dog attacks resulting in permanent scarring. Anything leaving you with ongoing medical needs or permanent disability. A 32-year-old construction worker who becomes paraplegic after a scaffold collapse needs reliable income for potentially another fifty years.

Workers' compensation cases often push structured settlements when permanent disability ends your career. Many state workers' comp systems actively encourage or even mandate structured payments for serious injuries. The tax treatment differs slightly from standard personal injury cases, but the annuity mechanics work identically.

Wrongful death claims provide for surviving family members. When a breadwinner dies due to someone else's negligence, settlements often include immediate funds for funeral costs and urgent debts, then monthly payments until the youngest child reaches adulthood, followed by a final lump sum for the surviving spouse's later years.

Medical malpractice awards mirror personal injury settlements in structure. Birth injuries, botched surgeries, delayed cancer diagnoses—cases causing permanent harm often result in payment schedules matching the victim's anticipated lifetime care requirements.

Lottery and gambling winnings sometimes use annuities, though these differ fundamentally from legal settlements. Lottery annuities are fully taxable, you can't assign or sell them (in most states), and the payment schedule is rigid—set by the lottery commission, not customized to your needs. When someone talks about "structured lottery winnings," they're describing something closer to an installment sale than a true structured settlement.

Environmental contamination settlements, class action proceeds, and certain employment discrimination cases occasionally incorporate structures, though far less commonly than the categories above.

Advantages and Disadvantages of Choosing an Annuity Structure

Neither lump sums nor structured payments win in every situation. The right choice depends on your specific circumstances—your financial experience, family situation, spending discipline, and future expense timeline.

Comparing Your Two Options: Key Differences That Matter

| What You're Evaluating | Structured Settlement Annuity | Lump Sum Payment |

| Federal & State Taxes | Zero taxes on personal injury settlements under IRC 104(a)(2) | Settlement principal isn't taxed; all investment growth gets taxed annually |

| Income Predictability | Locked-in payments regardless of markets, personal choices, or economic conditions | No income guarantees whatsoever; entirely dependent on investment performance and spending choices |

| Ability to Modify | Impossible to alter payment schedule after signing; accessing funds requires selling at steep discount | Total control over every dollar; spend or invest however you choose whenever you want |

| Protection from Lawsuits | Most states shield payments from creditors; usually can't be garnished except for child support or tax liens | Fully vulnerable to creditors, lawsuits, divorces, and bankruptcy proceedings |

| Market Volatility Risk | Zero exposure; insurance company absorbs all investment risk | Complete market exposure; a 2008-style crash could cut your balance in half |

| Keeping Pace with Inflation | Can build in annual increases at setup; doing so reduces starting payment amounts | You can invest aggressively for growth potentially exceeding inflation; you can also lose money |

| Accessing Cash Quickly | Terrible liquidity; selling future payments costs 30-40% and needs court approval | Perfect liquidity; write a check or withdraw funds same day |

| Running Out of Money | Guaranteed income for life or specified term; mathematically impossible to deplete early | Can completely run out if you mismanage funds; no safety net |

The tax advantage deserves emphasis because people underestimate it. Invest $1 million at 5% annual returns and you'll earn $50,000 yearly—but owe federal and state taxes on that $50,000. At a combined 30% rate, you're netting $35,000. A structured settlement paying you $50,000 annually delivers the full amount tax-free forever. You'd need roughly 7% after-tax returns to match that—hard to achieve consistently without taking substantial risk.

Protection from overspending matters more than most people admit. Research on lottery winners, sudden inheritance recipients, and injury claimants shows the same pattern repeatedly: unexpected wealth vanishes fast. Relatives need loans. "Investment opportunities" appear. Lifestyle expenses creep upward. A structured settlement makes overspending impossible—can't spend what you can't touch.

The main drawback? Inflexibility. Lose your job, face unexpected medical emergencies, spot a great business opportunity—your structured settlement keeps chugging along on its predetermined schedule. You can sell future payments (covered below), but only at brutal cost and after court approval.

My clients who thrive with structures are the ones honest about their limitations. Never managed serious money before? Got family members who'll pressure you for 'loans'? Facing decades of medical expenses? The annuity removes temptation—you can't blow money you can't access. The clients who struggle are those who underestimate future cash needs or overestimate their willpower when relatives come asking for help

— Jennifer Schorn

Common Mistakes People Make When Setting Up Settlement Annuities

Four errors show up repeatedly, and all of them are permanent once you sign:

Accepting the first payment schedule proposed without customization. A 28-year-old woman settling a car accident case agreed to level monthly payments for thirty years. Simple. Clean. Three years later, she realized she'd need much larger payments when her two kids hit college age (12-15 years out) and could manage with smaller amounts beforehand. Too late—the structure couldn't be modified.

Smarter approach: Map your anticipated major expenses across decades. Kids' education costs. Home modifications for disability. Vehicle replacements. Retirement supplement. Then request lump sum payments timed to those specific needs instead of generic monthly amounts.

Author: Danielle Morgan;

Source: avayabcm.com

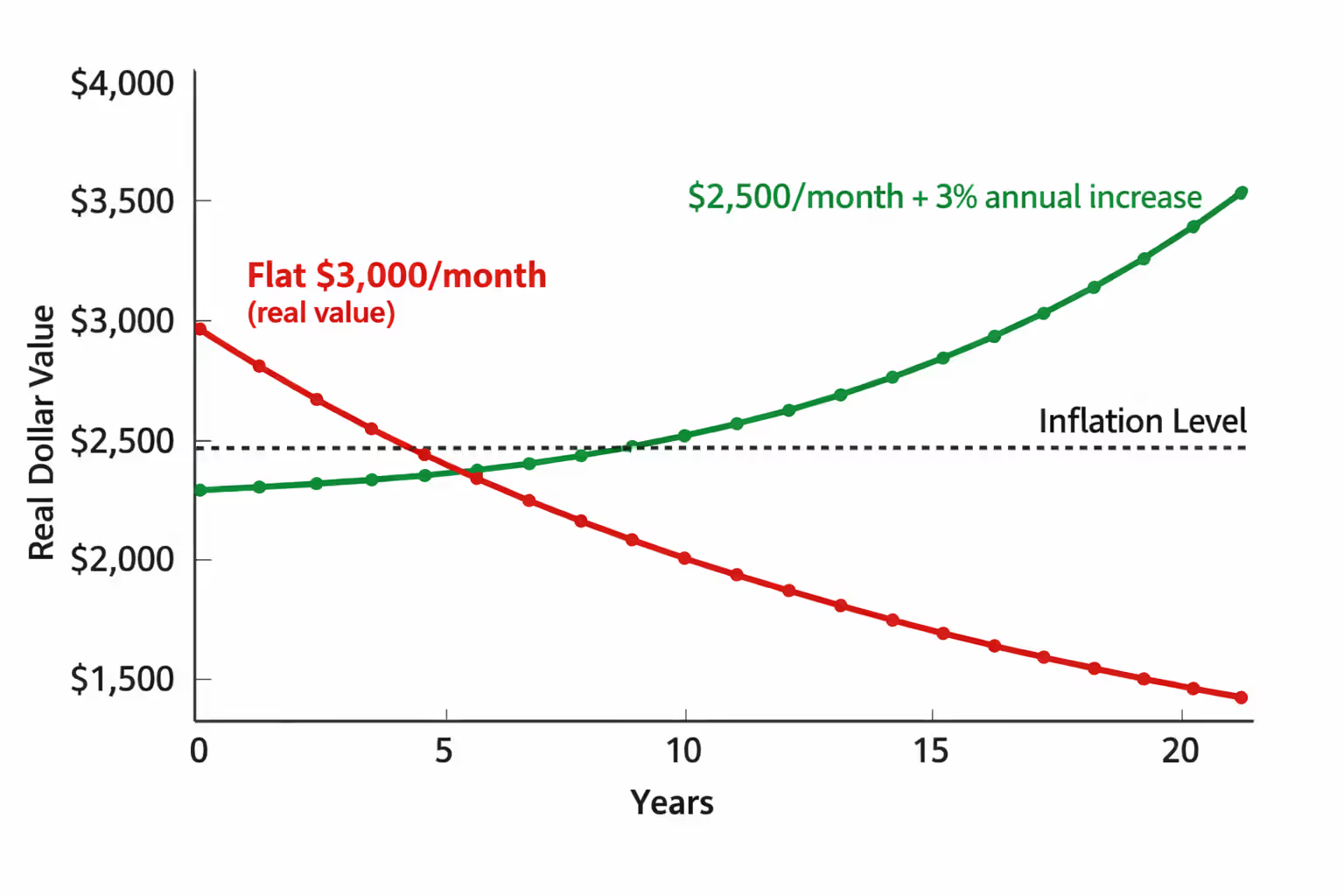

Ignoring inflation's impact over long payment periods. $3,000 monthly sounds adequate today. In twenty years? At just 3% annual inflation, that $3,000 buys what $1,650 buys now. Your rent, groceries, and utilities won't stay frozen at today's prices.

Smarter approach: Accept annual increases of 2-4%, even though this cuts your starting payment amount. A $2,500 monthly payment growing 3% annually provides better long-term security than flat $3,000 payments that become increasingly inadequate.

Forgetting about beneficiary designation paperwork. Die before receiving all scheduled payments? The remaining money passes to your designated beneficiaries—but only if you properly completed beneficiary forms after settlement. Without clear designations, payments might get stuck in probate for months, delaying distribution and potentially exposing the money to estate creditors.

Smarter approach: Complete beneficiary forms immediately after finalizing your settlement. Name both primary and contingent beneficiaries. Update these designations after marriages, divorces, births, and deaths.

Agreeing to unsuitable terms because you're exhausted and desperate to close the case. Settlement negotiations happen during incredibly stressful periods. You're tired of the lawsuit, need money now, and feel pressure to accept whatever's offered. Defense insurers prefer structures because they often cost the insurer less than equivalent lump sums (their actuaries use conservative assumptions that favor the insurance company).

Smarter approach: Consult an independent structured settlement expert—not one the defense insurer provides—before signing anything. A few days of additional review could improve your financial outcome for decades. Worth the wait.

Can You Change or Sell Your Structured Settlement Annuity?

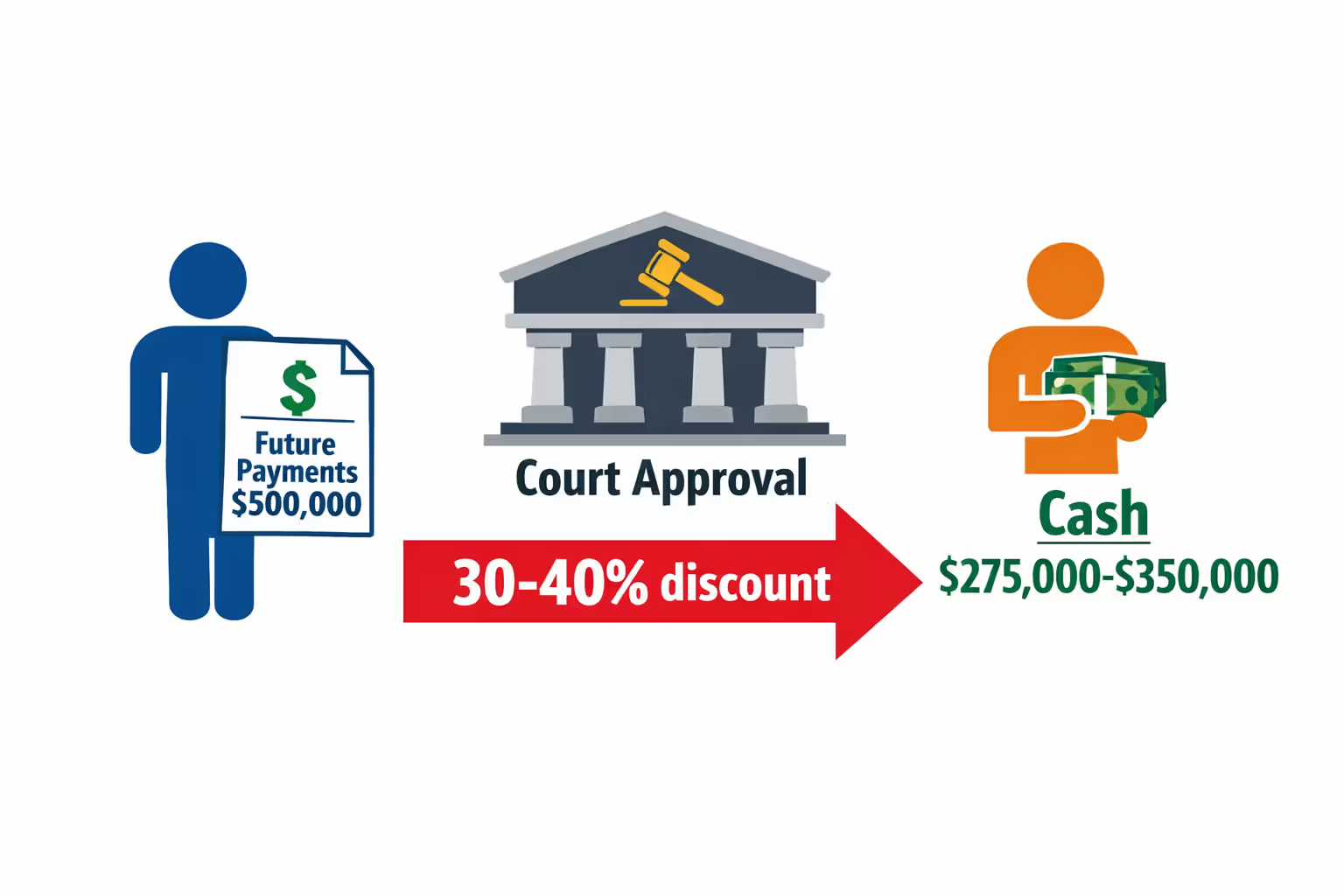

Life changes. That perfect payment schedule from five years ago might not work anymore. While you can't modify the annuity contract itself, you can sell some or all future payments to factoring companies specializing in purchasing structured settlement rights.

Federal and state laws regulate these transactions through Structured Settlement Protection Acts. Federal law requires court approval for any transfer of payment rights. Most states pile on additional requirements. These laws emerged during the 1990s after predatory factoring companies convinced desperate claimants to sell $100,000 in future payments for $15,000 in immediate cash.

How the selling process actually works starts with contacting a factoring company. You specify which payments you want to sell—maybe the next 60 monthly payments, or perhaps those three $50,000 lumps scheduled for years 8, 9, and 10. The company calculates what it'll pay based on payment amounts, timing, and its required rate of return (usually 9-18% annually, sometimes higher).

The factoring company prepares transfer agreements and disclosure statements showing exactly what you're selling, what you'll receive, and the effective discount rate. After both parties sign, the company petitions the court for approval.

Court approval isn't automatic. A judge holds a hearing to determine whether the transfer serves your best interests and whether you truly understand the terms. Judges examine your financial circumstances, why you need the money, whether you consulted independent advisors, and whether the discount rate is exploitative. Courts reject transfers they consider predatory or unnecessary—though most petitions that reach hearings do get approved.

Expect 45-90 days from initial agreement to receiving funds. Court filing fees, attorney costs, and administrative expenses reduce what you actually receive.

The discount rates and costs involved make this expensive. Scheduled to receive $50,000 annually for the next ten years ($500,000 total)? Sell all remaining payments and you might receive $275,000-$350,000 depending on the discount rate applied. That $150,000-$225,000 difference represents time value of money plus the factoring company's profit.

Selling near-term payments costs less than selling distant ones. Selling $30,000 in payments due over the next twelve months might net you $26,000-$27,000 (roughly 10-15% discount). Selling $30,000 in payments due fifteen years from now? Maybe $8,000-$12,000 if you're lucky.

Author: Danielle Morgan;

Source: avayabcm.com

Some states prohibit or severely restrict selling structured settlement payments. Others require factoring companies to advise you to seek independent legal and financial counsel. The court hearing provides a final safeguard, but judges approve most petitions that reach them.

Frequently Asked Questions About Structured Settlement Annuities

A structured settlement annuity transforms your legal award into guaranteed, tax-exempt payments designed to deliver financial stability across years or decades. This approach works exceptionally well for claimants facing ongoing expenses, those without experience managing substantial sums, or anyone wanting protection from spending pressure and market volatility.

Choosing between structured payments and an immediate lump sum requires brutal honesty about your financial discipline, future needs, and comfort with risk. Structures offer unmatched security and tax advantages—but you sacrifice flexibility and quick access to cash. Customizing payment schedules to match anticipated expenses (medical care, children's education, retirement supplementation) maximizes the benefits while minimizing the frustrations.

Once you finalize the structure, changes are nearly impossible without selling payment rights at significant cost through court-supervised transactions. Careful planning during initial setup prevents expensive corrections later. Think hard about inflation protection, beneficiary designations, and realistic assessment of future cash needs before signing anything.

For claimants with permanent injuries, ongoing medical requirements, or dependents needing long-term financial support, structured settlement annuities deliver stability that lump sums rarely match. The certainty that money will be available when you need it—regardless of market crashes, poor investment decisions, or family spending pressure—often outweighs the frustration of limited access. Just make sure the payment schedule actually matches your life.