Top-down view of a desk with two documents comparing a single large cash stack versus a row of smaller equal cash stacks, pen and calculator between them

How Structured Settlement Payments Work Over Time

Content

Picture this: You've just settled your personal injury case for $500,000. The insurance adjuster slides two options across the table. Take the full amount today, or accept $2,500 every month for the next twenty years. Which sounds better?

Most people's first instinct? Grab that check and run. But here's what actually happens: Within sixty months, about 70% of lump-sum recipients have burned through everything, according to National Structured Settlements Trade Association data. Meanwhile, those who chose monthly payments still have income arriving like clockwork.

Structured settlement payments spread your legal award across time instead of dumping it all at once. They're not exotic financial instruments—just a different way to receive money you've already won. But the mechanics behind them matter more than you'd think.

What Are Structured Settlements and How Do They Differ from Lump-Sum Payouts?

Here's what actually happens when you choose structured payments: The defendant's insurance company doesn't write you monthly checks forever. Instead, they purchase an annuity contract from a life insurance company—think MetLife or Prudential—and that annuity issuer takes over payment duties. You're out of the picture as far as the defendant is concerned. Done. Finished. They've fulfilled their obligation.

The annuity guarantees specific amounts on specific dates. Maybe $3,000 lands in your account on the 15th of every month. Maybe you get $40,000 each January for fifteen years. Some folks design elaborate schedules: smaller payments now, larger ones when the kids hit college age, a big chunk at retirement. The customization options are wild.

Contrast this with taking everything upfront. You've got $500,000 sitting in your checking account Tuesday morning. Feels great, right? Until your brother-in-law needs a "small business loan." Your car breaks down—might as well buy new. That kitchen remodel you've been postponing? Why not? Six months later, you're looking at $280,000 and wondering where it went.

Author: Christopher Vaughn;

Source: avayabcm.com

I'm not suggesting everyone mismanages lump sums. Plenty of people invest wisely and stretch their settlements for decades. But courts see enough disasters that they actually require structured settlements for minors and legally incapacitated adults in most jurisdictions. Can't blow money you don't have access to yet.

The tax angle matters too. Lump sums from physical injury cases are tax-free initially—but the moment you invest that money, you're paying taxes on any gains. Structured settlements grow tax-free inside the annuity. That difference compounds dramatically over twenty or thirty years.

When do structures make the most sense? Permanent disabilities where you'll never work again. Ongoing medical needs that'll stretch for decades. Cases involving kids who need support until adulthood. Elderly plaintiffs worried about outliving their money. Basically, situations where losing the settlement money would be catastrophic.

The Anatomy of a Settlement Payment Stream: How Periodic Payments Are Calculated

Nobody just makes up your payment amounts. There's actual math happening, even if lawyers don't always explain it clearly. Think of it like reverse-engineering a pension—insurance actuaries figure out how much money today will generate your desired payments tomorrow.

Factors That Determine Your Payment Amount

Your age matters enormously. A 30-year-old structuring lifetime payments gets smaller monthly amounts than a 70-year-old with the same settlement size. Why? The younger person's payments might need to stretch across fifty years instead of fifteen. Insurance companies use mortality tables—basically educated guesses about life expectancy—to run these calculations.

Here's something that surprises people: The insurance company doesn't take your full $750,000 settlement and slowly distribute it. They invest less upfront (maybe $580,000) in ultra-conservative bonds and real estate, then use investment returns to bridge the gap between what they're holding and what they owe you. That difference represents their profit margin and the time-value of money.

Interest rates affect everything. When rates are high, insurers can fund your payments with less capital because their investments earn more. During low-rate periods like 2020-2021, the same payment stream costs them significantly more upfront. This influences negotiations—defendants sometimes push harder for structures when rates are favorable because annuities cost them less.

Your medical situation drives customization. Need $5,000 monthly for ongoing treatments? No problem. Want to defer larger payments until you've exhausted your Medicare coverage? Doable. Parents often structure increasing payments that match kids' developmental stages—more money when daycare ends, another bump at middle school, a big increase for college years.

Fixed vs. Indexed Payment Structures

Most structures lock in exact amounts. You'll receive precisely $2,847.33 every month for the next eighteen years. Never a penny more, never less (unless you sell some payments, which we'll discuss later). This makes budgeting simple but completely ignores inflation.

That $2,847 buys a lot less groceries in year fifteen than year one. Indexed structures address this by building in annual increases—typically 2-4% raises each year. You start with smaller payments, maybe $2,200 monthly, but by year ten you're collecting $3,100. Your purchasing power holds steadier across decades.

Some settlements blend approaches creatively. Fixed payments for seven years, then a permanent increase to a higher fixed amount. Others include periodic lump sums alongside regular payments—say $1,800 monthly plus $30,000 every five years for major expenses like vehicle replacement. Your attorney and a structured settlement consultant will sketch options during negotiations.

Author: Christopher Vaughn;

Source: avayabcm.com

Common Structured Settlement Payout Structures Explained

There's no such thing as a "standard" structured settlement—every arrangement reflects someone's unique circumstances. But certain patterns appear frequently enough that they're worth understanding before your attorney starts throwing options at you.

Monthly payments mirror paychecks. Money arrives on the same date each month, usually via direct deposit. Most people choose this for replacing lost wages or covering household expenses. The predictability helps enormously if you're disabled and can't work—you know exactly what's hitting your account on the 1st or 15th. Downside? That fixed amount loses purchasing power unless you've structured in annual raises.

Annual payments work when you've got other income sources but need periodic boosts. Maybe you returned to work part-time after your injury, earning $35,000 yearly. An additional $50,000 arriving each December would substantially improve your situation without overwhelming you with monthly cash you don't really need. Annual structures often deliver higher total payouts than monthly arrangements because the insurer holds your money longer and earns more returns.

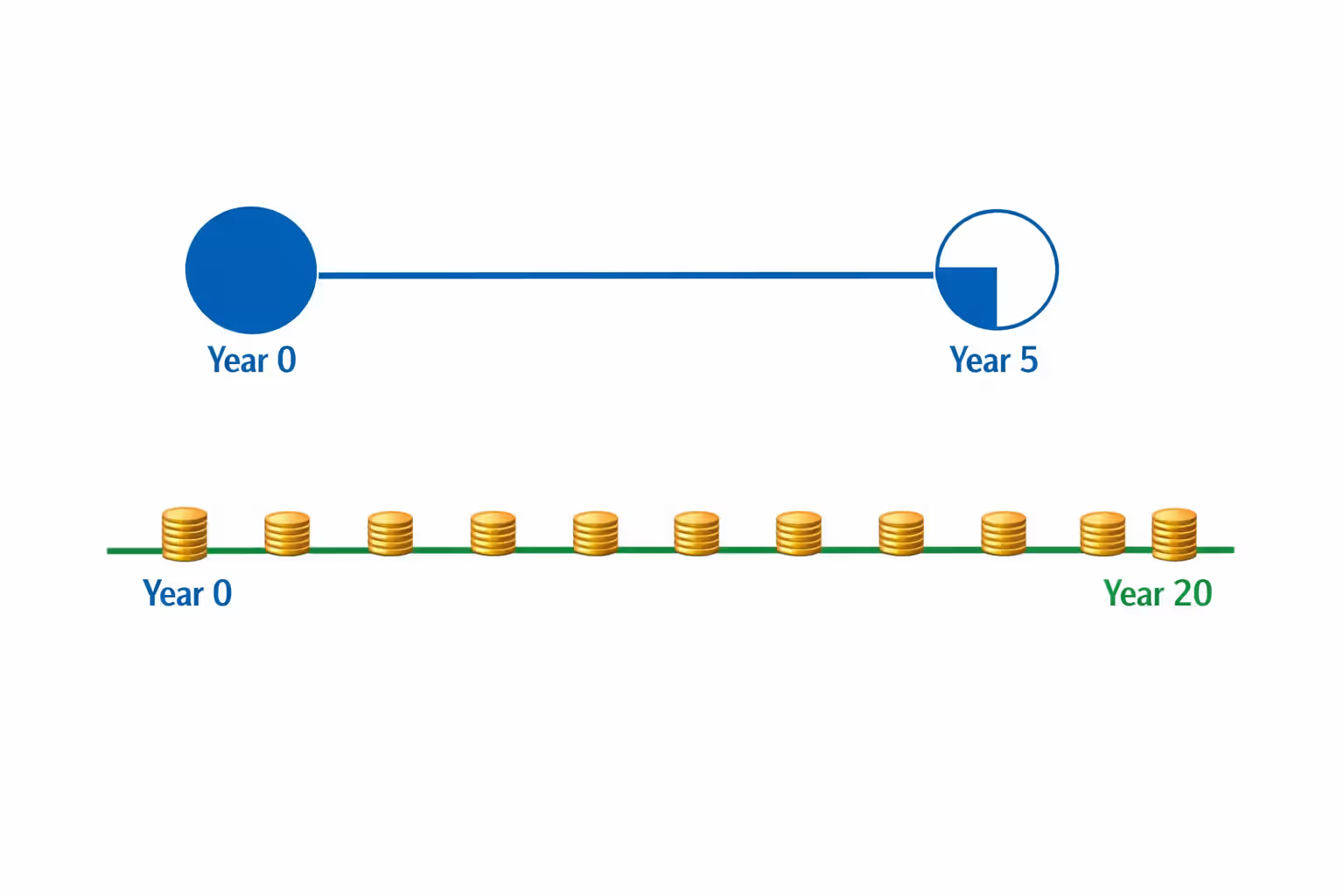

Deferred payments involve waiting—sometimes many years—before payments begin. A 35-year-old plaintiff might structure nothing until age 65, then receive $6,000 monthly for life. That thirty-year deferral allows enormous growth. The insurance company invests your settlement for three decades before paying out anything, resulting in much larger eventual payments than an immediate structure. This essentially creates a private pension.

Lump-sum hybrids split the difference. Take $150,000 immediately to cover medical bills and attorney fees, then receive $2,800 monthly thereafter. You're addressing urgent needs while maintaining long-term security. The catch? That upfront money loses the tax advantage if your settlement included taxable components, and you're reducing what's available for the structured portion.

Lifetime payments continue until you die—whether that's next year or fifty years from now. The insurance company gambles on your life expectancy using actuarial tables, but you win if you outlive projections. Many lifetime structures include "period certain" guarantees (payments continue at least twenty years even if you die sooner, with remaining funds going to beneficiaries). This prevents the insurance company from profiting if you're hit by a bus in year two.

Period-certain payments run for a fixed term regardless of what happens to you. Twenty years means exactly that. If you die in year eight, your estate or named beneficiaries collect the remaining twelve years of payments on the original schedule. This structure works well when you want to provide for specific dependents or know you'll face expenses for a defined period.

| Structure Type | How Often You're Paid | How Long It Lasts | Works Best When You Need | Why People Choose This | The Downsides |

| Monthly schedule | Every 30 days | One to three decades | Income replacement for living expenses | Matches normal bill cycles, easy budgeting | Inflation chips away at buying power, zero flexibility |

| Annual schedule | Once each year | Ten to forty years | Supplemental income boost, not primary support | Bigger total payout potential, simpler tracking | Eleven-month gaps require separate emergency savings |

| Deferred schedule | Starts after waiting period | Payments begin 5-40 years out | Retirement security, children's future needs | Waiting period allows massive growth | Zero income meanwhile, inflation during waiting period |

| Immediate-plus-periodic mix | Part now, rest over time | Depends on negotiation | Urgent bills now, security later | Solves immediate crisis, keeps future protection | Shrinks tax benefits, risks wasting the upfront cash |

| Lifetime schedule | Monthly until death | As long as you live | Permanent disability, lost career income | Impossible to outlive the money | Heirs get nothing unless guaranteed period included |

| Guaranteed-period schedule | Monthly or yearly | Exactly X years | Supporting dependents, known expense windows | Full payout guaranteed to you or heirs | Income stops when term ends even if you still need it |

How Annuity Settlement Payment Streams Are Funded and Guaranteed

Understanding where your money actually comes from matters more than most people realize. The defendant isn't mailing you checks. Their insurance company isn't either, despite what you might assume.

What really happens: The defendant's liability insurer purchases what's called a "qualified assignment" annuity from a specialized life insurance company. This transaction shifts the payment obligation completely off the defendant and their insurer. You're now dealing exclusively with the annuity issuer—companies like MetLife, Pacific Life, New York Life, Prudential, or MassMutual. These are the same massive insurers handling billions in retirement accounts and life insurance policies.

Only the most financially stable insurance companies participate in structured settlement annuities. We're talking about firms rated AA or higher by A.M. Best, Moody's, and Standard & Poor's. These ratings measure their ability to meet obligations even during economic catastrophes. During the 2008 financial crisis, structured settlement annuities continued paying without interruption despite the chaos.

The annuity contract is a legally binding promise to pay specific amounts on specific dates. Unlike your 401(k) that bounces up and down with the stock market, these obligations are fixed and guaranteed. The insurance company invests the premium (what they received to purchase your annuity) in extremely conservative instruments—mostly government bonds, high-grade corporate debt, and commercial real estate. Returns from these investments fund your payments plus their profit.

What if the insurance company goes belly-up? Every state maintains guaranty associations specifically to protect policyholders when insurers fail. These aren't insurance policies you buy—they're automatic protections funded by assessments on all insurance companies operating in each state. Coverage limits vary (typically $250,000 to $500,000 depending on your state), though this represents your payment stream's present value, not the total of all future payments.

Real talk: In the past forty years, structured settlement annuity defaults are essentially nonexistent. These companies have balance sheets exceeding half a trillion dollars and face regulatory scrutiny that makes banking oversight look casual. Your bigger risk is inflation eroding what your fixed payments can buy, not the insurer disappearing.

The tax benefits come from IRC Section 104(a)(2), which exempts physical injury settlements from taxation. Not just the initial amount—the growth too. If you took a lump sum and invested it, you'd pay taxes on investment gains. Structured settlements grow tax-free inside the annuity, creating significant long-term value that compounds over decades.

Expert Insight:

I've spent 35 years working with structured settlements as a certified financial planner, and clients always ask about safety. Here's the reality: I've never seen a structured settlement annuity fail to make payments. Not once. These arrangements are backed by insurance giants with assets exceeding $500 billion, state guaranty associations as a backup, and regulatory oversight that's frankly excessive. Your actual risk? Inflation eating your purchasing power over time, not the annuity company vanishing into thin air. That inflation risk is real and significant—just not the risk people worry about

— Robert Chen

Reading Your Settlement Payment Schedule: What to Expect Over Time

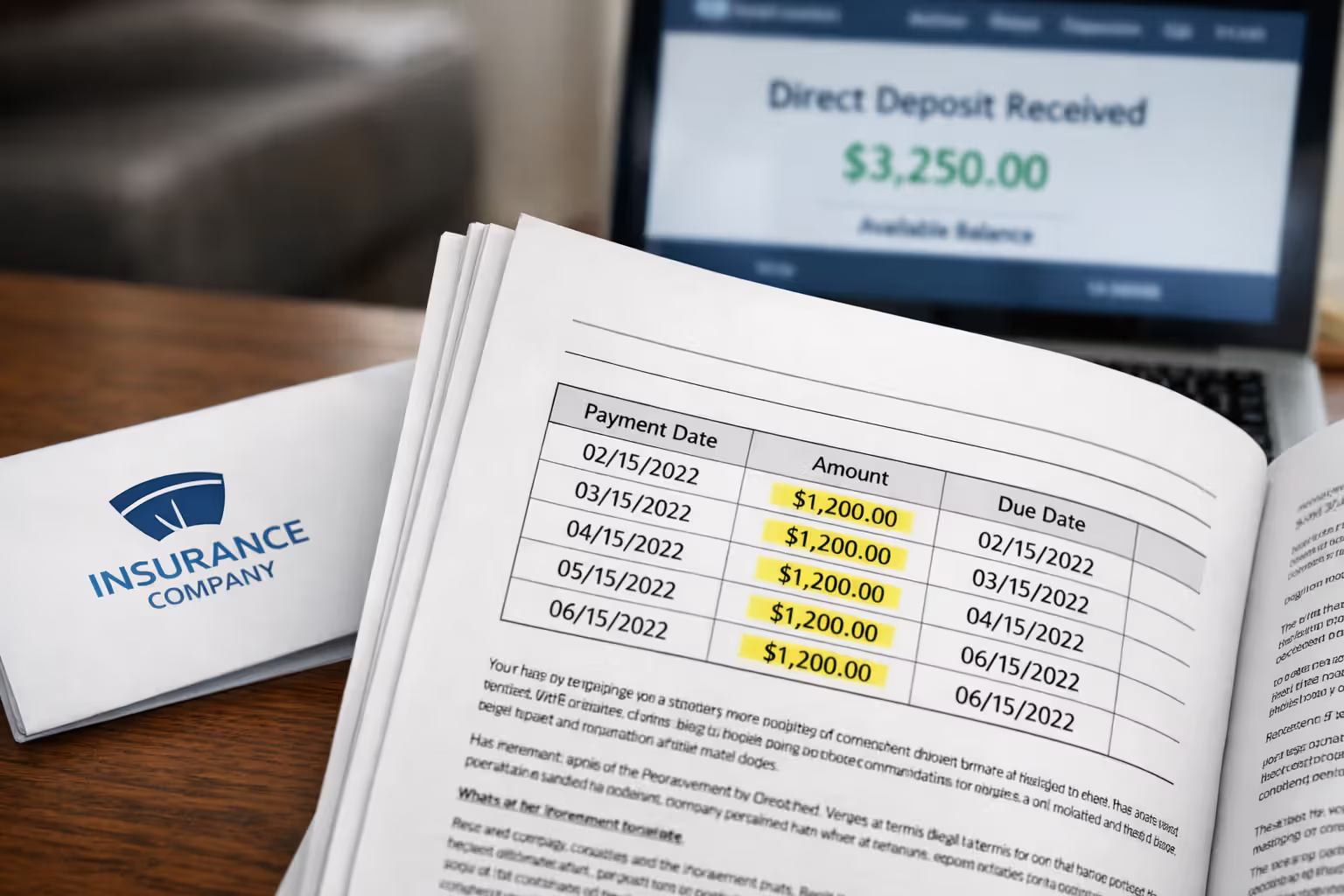

You'll receive a formal document—usually 8-15 pages—within weeks of your settlement finalizing. This isn't some casual summary. It's a binding legal contract detailing every payment you'll receive for the structure's entire duration, whether that's ten years or the rest of your life.

The document identifies everything: the annuity issuer's name, your policy number, your legal status as payee. Then comes the payment schedule itself, spelled out with zero ambiguity: "$2,847.33 on the 15th day of each month, commencing June 15, 2025, continuing for 240 consecutive months." If you've structured in annual increases, step-ups, or periodic lump sums, each appears with its exact timing and amount.

How you actually receive money varies. Most people choose direct deposit—funds hit your checking account automatically on the scheduled date, just like employment direct deposit. Some insurers offer prepaid cards that reload each payment period. Paper checks still exist but they're becoming rare because of mail delays and fraud concerns. You'll establish your preferred method during settlement, and it generally stays fixed unless you submit formal change requests.

Author: Christopher Vaughn;

Source: avayabcm.com

Tax reporting for qualified physical injury structures? There isn't any. You receive no 1099 forms. You don't report the payments on your tax return. They're completely tax-free—unlike annuities you purchase yourself, where growth gets taxed as ordinary income. Non-physical injury settlements (employment discrimination, breach of contract) do generate taxable income and require reporting, but that's different from personal injury structures.

Keep your settlement paperwork forever. Seriously—don't lose it. Those documents prove your payments' tax-free status if the IRS ever questions why you're depositing $3,000 monthly without reporting income. You'll also need them if you consider selling future payments, apply for benefits requiring asset disclosure, or deal with estate planning.

Some schedules include cost-of-living adjustments that change amounts annually. Your January payment might be $3,000, then next January it jumps to $3,090 based on a 3% scheduled increase. The contract shows these increases clearly, though actual amounts might adjust slightly if your structure ties to specific inflation indices like CPI-U.

Missed payments are incredibly rare but do happen—usually banking glitches or administrative errors. If money doesn't arrive within two business days of the scheduled date, contact the annuity issuer's structured settlement administration department immediately. They'll investigate and typically expedite payment once they've identified the problem. Unlike chasing down debtors who ignore you, annuity issuers have legal obligations and regulatory oversight ensuring compliance.

Can You Modify or Sell Your Structured Settlement Payment Stream?

Short answer: Modifying your existing payment schedule is almost impossible. Selling future payments for cash right now? That's legally allowed, though you'll need court approval in most states.

The inflexibility is intentional, not an oversight. Those tax advantages under IRC Section 104(a)(2) require payment terms to be locked at settlement. If you could fiddle with amounts or timing later, the IRS considers this "constructive receipt"—the ability to access funds makes them taxable even if you don't actually take them. Courts also view the rigidity as protecting plaintiffs from bad financial decisions or pressure from manipulative relatives.

Genuine modifications require extraordinary circumstances and usually need all original parties—defendant, insurers, courts—agreeing to changes. This might happen if you're permanently institutionalized and a guardian needs to redirect payments, or if obvious clerical errors in the original paperwork need fixing. Routine requests like "I want more money now" or "Can I pause payments for a year?" won't fly.

Selling payments works differently. A secondary market emerged in the 1990s allowing recipients to sell some or all future payments to companies paying immediate lump sums at a discount. You're owed $100,000 over the next five years? A purchasing company might offer $68,000 today. You get immediate cash; they collect the full $100,000 over time and pocket the $32,000 difference as profit.

Federal law and most state statutes require court approval for these transfers, designed to protect you from predatory terms. Judges must determine the transfer serves your "best interest" and doesn't result from coercion or manipulation. You'll attend a hearing, explain why you need the money, and demonstrate you understand what you're giving up. Courts reject transfers for frivolous purposes (vacation to Europe) but generally approve them for genuine hardships: preventing home foreclosure, paying for surgery, starting a legitimate business.

Discount rates vary wildly—you might receive anywhere from 50% to 85% of your payments' present value, depending on market conditions, payment timing, and the annuity issuer's financial rating. Payments from MetLife-backed annuities typically fetch better rates than those from obscure issuers because they're more valuable to buyers.

You can sell everything or just portions. Partial sales might transfer five years while retaining everything afterward, or sell every other payment while keeping the rest. This flexibility lets you raise capital without completely eliminating your income stream.

Author: Christopher Vaughn;

Source: avayabcm.com

Watch out for companies pressuring rushed decisions or offering rates below 60% of present value without clear justification. Get multiple quotes, consult an attorney, and calculate precisely what you're surrendering. The National Association of Settlement Purchasers maintains ethical standards for member companies, though not all buyers belong.

Frequently Asked Questions About Structured Settlement Payments

Structured settlement payments transform one-time legal awards into reliable income streams designed for long-term financial security. The payment schedules—whether monthly, annual, or customized around specific life events—provide predictability that lump sums can't match. Understanding the calculation methods, how annuity contracts fund these arrangements, and what state guaranty associations protect helps you make informed decisions when settlement offers arrive.

The fundamental trade-off is straightforward: You're sacrificing flexibility and immediate access to large sums in exchange for guaranteed, tax-free income lasting decades or even your entire lifetime. For many recipients—especially those with permanent disabilities, ongoing medical requirements, or concerns about managing substantial amounts—this exchange delivers financial security that lump-sum payments rarely provide.

Success depends on matching the payout structure to your actual circumstances rather than accepting generic templates, and recognizing that while these payments are exceptionally secure, they're also essentially inflexible once established. Whether you're currently negotiating a settlement, already receiving payments, or considering selling future payments for immediate cash, remember this: Structured settlements work best when they're designed around your real needs, not theoretical ones.