Person reviewing structured settlement payment documents and financial schedules at an office desk with calculator and laptop

How to Choose the Right Structured Settlement Payment Options for You

Content

Here's what most people don't realize about structured settlements: you're not stuck with a one-size-fits-all payment plan. Whether you settled a car accident case, a workplace injury claim, or a medical malpractice lawsuit, you've got real choices about when and how you'll receive that money.

Maybe you need cash now for medical bills stacking up on your kitchen counter. Or perhaps you'd rather build a retirement fund that grows tax-free for the next twenty years. Some folks split the difference—taking enough today to get back on their feet, then setting up monthly checks to replace the wages they'll never earn again.

Your settlement might be worth $300,000, $1 million, or more. Either way, the payment schedule you nail down today determines whether that money actually supports you through the rough patches ahead or runs out when you need it most.

What Are Structured Settlements and How Do Payments Work?

Think of a structured settlement as a legally binding promise to pay you money over time instead of handing you one massive check. When someone injures you (or kills a family member), their insurance company can purchase an annuity from a life insurance carrier. That annuity becomes responsible for cutting you checks according to whatever schedule everyone agreed to.

The whole concept took off in 1982. Congress stepped in with tax legislation that made these periodic payments incredibly attractive—we're talking zero federal taxes on personal injury money, even the growth portion. Before that, most injury victims just took lump sums and dealt with the tax consequences.

Here's the basic machinery: Let's say you won a $500,000 settlement. The defendant's insurer pays maybe $400,000 to a highly rated life insurance company like MetLife or New York Life. They set up an annuity in your name. From that point forward, the life insurer—not the person who hurt you—sends your payments. The defendant walks away, obligation fulfilled.

You'll see these arrangements constantly in certain case types. Personal injury claims, especially catastrophic ones involving brain damage or paralysis. Medical malpractice settlements where someone's looking at a lifetime of treatments. Wrongful death cases where kids lost a parent. Workers' comp claims that left someone permanently disabled. Courts particularly like structuring settlements for minors (who can't manage large sums) and people with cognitive impairments.

State laws vary on the details, but federal protections are solid. IRC Section 104(a)(2) shields your personal injury payments from federal income tax—every penny stays in your pocket. The Periodic Payment Settlement Act from 1982 established these tax rules. Most states adopted the Structured Settlement Protection Act too, which says you can't just sell your future payments to some factoring company without a judge signing off first.

Types of Structured Settlement Payment Schedules You Can Choose

What makes structured settlement payout options genuinely useful is customization. You're not choosing between Option A and Option B. You're designing a payment flow that matches your actual life.

Immediate vs. Deferred Payment Structures

Immediate structures start pumping out money within 30-60 days of settlement. Picture this: You settled three months ago. Your back surgeries are covered, but rent's due, the mortgage is two months behind, and you haven't worked since the accident. You structure the settlement for $2,800 monthly starting next month. That's immediate.

Author: Olivia Carmichael;

Source: avayabcm.com

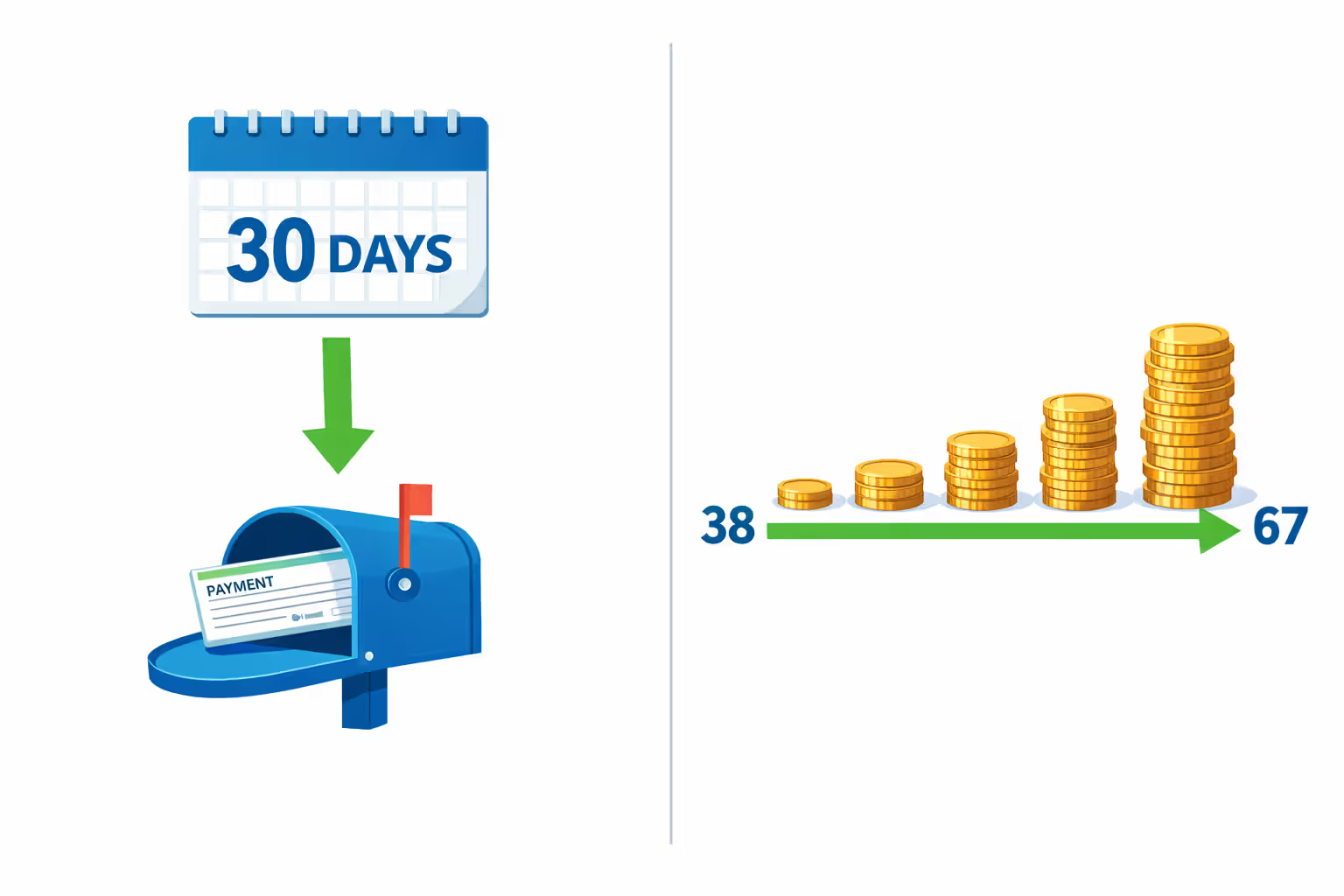

Deferred structures work backwards. You tell the insurance company, "Don't send me anything for ten years." Why would anyone do that? Because that money grows tax-free while it waits, and the payments end up much larger when they finally start.

Real example: A 38-year-old construction worker takes $250,000 from a workplace accident. He could start receiving $1,100 monthly right away. Instead, he defers everything until age 67—he's still working, doesn't need the cash yet. At retirement, those deferred payments kick in at $2,400 monthly for life. Same settlement dollars, but the deferral period more than doubled his monthly income.

The catch? You're broke during the waiting period, at least as far as settlement money goes. If you defer for 15 years but lose your job in year five, that settlement won't help you.

Fixed Periodic Payments

The simplest structure: same amount, same schedule, no surprises. You get $3,200 on the first of every month for the next 18 years. Period.

People love the predictability. You can plan everything—rent, car payments, groceries, utilities. Banks love it too when you're applying for a mortgage. "Yes, I have guaranteed income of $3,200 monthly for the next 18 years, here's the court order proving it." That's powerful.

But here's the problem nobody thinks about in year one: inflation eats fixed payments alive. That $3,200 monthly feels solid today. In 2035, after 3% annual inflation compounds for a decade? You're looking at the equivalent of $2,380 in today's dollars. By 2043, it's down to $1,970 in purchasing power. Your rent didn't get cheaper—your payment just buys less.

Lump-Sum Payments Combined with Annuities

Most sophisticated settlement recipients use hybrid structures. Take some cash upfront, set up monthly payments for the rest.

Example: $425,000 settlement for a woman paralyzed in a pedestrian accident. She takes $85,000 immediately—renovates her bathroom for wheelchair access, buys an adaptive van, pays off credit cards she maxed out during six months of unemployment. The remaining $340,000 funds an annuity paying $2,100 monthly for 25 years.

This hybrid approach handles reality better than pure structures. Yes, you've got long-term needs. You've also got immediate problems that won't wait for monthly checks to accumulate.

Courts sometimes restrict upfront amounts, particularly for minors or people with diminished capacity. A judge might approve $30,000 upfront from a $400,000 settlement for a brain-injured plaintiff but deny a request for $200,000 up front. They're protecting people from themselves.

Increasing Payment Schedules (Inflation Protection)

Want to maintain purchasing power? Build annual increases into your payment schedule. You might start at $1,800 monthly with 3% annual bumps. Next year it's $1,854. Year three: $1,910. Year ten: $2,348. Year twenty: $3,071.

You're essentially purchasing inflation insurance. Yes, you're starting lower than you would with fixed payments—that's the trade-off. A fixed structure might offer $2,200 monthly from the same settlement. But in year 15, your increasing payments have caught up and surpassed the fixed amount, and they keep climbing.

The math works best for younger recipients with decades ahead. A 28-year-old structuring payments for 40 years needs inflation protection. A 67-year-old setting up ten years of income? Inflation matters less—fixed payments might make more sense.

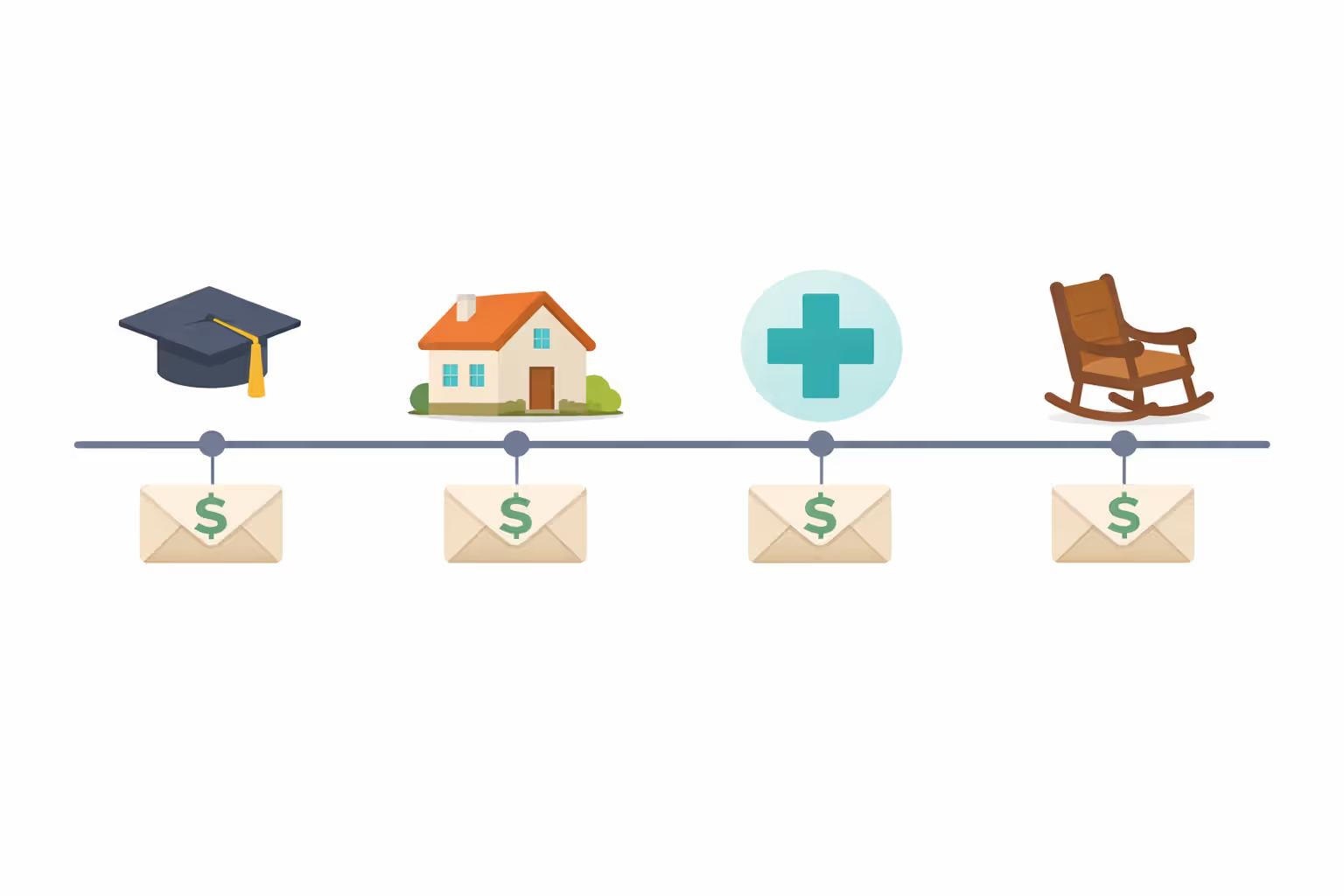

Customizing Your Settlement Payout to Match Life Events

Generic payment schedules ignore how life actually works. Smart settlement planning maps payments to your real timeline.

Take education costs. Let's say you're settling a case for your 12-year-old daughter who was permanently injured. You know she'll start college at 18. Structure lump-sum payments: $35,000 when she turns 18, another $35,000 at 19, 20, and 21. Four years, $140,000 total for tuition. You're not hoping you saved enough from monthly payments—the money arrives exactly when the bursar's office wants it.

Or retirement engineering. You're 43, permanently disabled, receiving $2,400 monthly in disability benefits until age 65. You structure the settlement for modest $1,600 monthly payments now (supplementing disability), then $5,200 monthly starting at 65 when disability ends. Your total income actually increases at retirement instead of dropping off a cliff.

Medical planning gets creative. Someone with a degenerative condition structures payments that grow as care needs intensify: $1,500 monthly for years 1-5, $2,500 for years 6-10, $4,000 for years 11-20. They're matching payment amounts to anticipated care costs.

Housing needs fit too. A 31-year-old recipient defers most payments for four years while continuing to work. In year four, he takes a $175,000 lump sum for a house down payment, then monthly payments begin to cover the mortgage.

The key isn't complexity for its own sake. It's honesty about what's coming. Sit down with a financial planner and actually think through the next 20-30 years. When do kids hit college age? When's your mortgage balloon payment due? When might you need a wheelchair-accessible vehicle? Build the payment schedule around those actual events, not some insurance company's template.

Author: Olivia Carmichael;

Source: avayabcm.com

Lump-Sum vs. Periodic Payments: Which Option Saves You More?

This question starts more fights between settlement recipients and their advisors than anything else. "Just give me the money now, I'll handle it." Maybe. But probably not.

Tax treatment makes periodic payments ridiculously attractive. Every dollar from a personal injury structured settlement is tax-free. Take $600,000 over 20 years, pay zero federal income tax. Compare that to grabbing a $450,000 lump sum, investing it, and paying taxes on $35,000 in annual investment income. You're handing the IRS $7,000-10,000 yearly on money that would've been completely tax-free in a structure.

But investment opportunity is the counterargument. If you're a sophisticated investor (truly sophisticated, not "I bought some Bitcoin once"), you might generate 8-9% average annual returns. The structured settlement might only build in 4-5% growth. On paper, you come out ahead managing the money yourself.

Here's what actually happens, though: Most people blow through lump sums frighteningly fast. The National Endowment for Financial Education reports that 70% of people who receive large windfalls lose it within a few years. Family members pressure you for loans. Scammers target you. You upgrade your lifestyle. Five years later, the money's gone.

Periodic payments prevent that disaster. You can't spend December's payment in January—it hasn't arrived yet. You can't blow next year's payments on a boat—you don't have access. This forced discipline saves people from their worst impulses.

Financial security is about guarantees, not possibilities. Structured payments arrive whether the stock market crashes, you make terrible decisions, or you declare bankruptcy. They're protected from most creditors in most states. If you structure lifetime payments, you can't outlive your income. Lump sums offer zero guarantees—the money can vanish.

| What You're Comparing | Taking the Lump Sum | Setting Up Periodic Payments |

| How taxes work | Settlement itself is tax-free, but you'll pay taxes on whatever your investments earn | Not a penny goes to taxes, including built-in growth |

| Flexibility and access | It's your money—invest it, spend it, gift it, whatever you want | You're locked in; payments arrive on the predetermined schedule |

| Investment decisions | You make every call about where money goes and how it's managed | The life insurance company handles everything; you have no input |

| Spending risk level | Extremely high—most recipients burn through lump sums within five years | Minimal risk since you can only access each payment as it arrives |

| Creditor protections | State-dependent; creditors can often seize lump sums | Generally strong protections in most jurisdictions |

| Who benefits most | People with genuine investment expertise and specific opportunities requiring capital | Nearly everyone else—especially those needing reliable long-term income |

| Long-term security | Entirely up to your choices; make mistakes and it's gone forever | Locked in; payments continue on schedule regardless of your decisions |

Here's the truth most people don't want to hear: unless you've got a Series 65 license and a demonstrated track record managing six-figure portfolios, periodic payments serve you better. The tax benefits alone justify the choice. The creditor protections add another layer. The forced savings might save your financial life.

Lump sums make sense in narrow circumstances: you're opening a business and need startup capital; you're buying a house in a market where renting costs more than owning; you've got tax liens or judgments that'll seize periodic payments anyway. For everyone else? Take the guaranteed monthly income.

Common Mistakes When Selecting a Structured Settlement Payment Plan

People screw up structured settlement payment choices in predictable ways. Here are the biggest disasters to avoid.

Underestimating future expenses ruins more settlement plans than anything else. You're 32 years old, living alone, minimal expenses. You figure $2,400 monthly covers everything comfortably. Fast forward twelve years—you're married, two kids, mortgage, car payments, braces, sports fees, grocery bills that would've shocked your younger self. That $2,400 doesn't stretch anymore, but you're stuck with it for another 25 years.

Build cushion into your numbers. If you think you need $2,000 monthly, structure $2,800. You'll thank yourself later.

Inflation gets ignored until it's too late. You structured $3,500 monthly in 2025. Feels great. It's 2045, and thanks to inflation averaging 3% annually, your $3,500 buys what $1,930 bought in 2025. Your payment hasn't changed—a gallon of milk just costs $8 now. Twenty years of flat payments means twenty years of declining purchasing power.

Demand increasing payment structures or periodic lump-sum boosts if your settlement stretches beyond ten years. Inflation is guaranteed. Your payment structure should account for it.

Skipping professional financial advice to save a few bucks costs a fortune in poor decisions. "I don't need a financial planner, the insurance company explained everything." The insurance company works for the insurance company. They're not optimizing your settlement; they're minimizing their costs.

Pay a certified financial planner (CFP) with structured settlement experience $1,500 to model different scenarios. On a $400,000 settlement, that's 0.375% of your money—and it might add $100,000 in long-term value through better structuring.

Prioritizing immediate wants over long-term needs creates regret that lasts decades. You really want that $65,000 upfront for a new truck, nice vacation, some home improvements. So you take it, leaving only $1,400 monthly for the next 28 years. Five years later, the truck's depreciated 60%, the vacation is a fading memory, and you're stuck with inadequate monthly income until you're 70.

Settlement money exists to support you through decades of reduced earnings and increased expenses. Treat it that way, not like a lottery win.

Ignoring state-specific legal protections creates unnecessary vulnerability. Oklahoma offers stronger creditor protections for structured payments than Georgia. New York has stricter rules about selling payment rights than Nevada. Your payment structure should leverage whatever protections your state offers.

Forgetting about family in the payment structure leaves people you love with nothing. You structure lifetime payments—great for you, but if you die in year six, payments stop and your spouse gets zero. Period-certain provisions (20 years certain, 25 years certain) guarantee your beneficiaries receive payments for the stated period even if you die early. Refund features ensure beneficiaries get whatever you hadn't received yet. Don't structure a settlement without addressing what happens if you die.

Author: Olivia Carmichael;

Source: avayabcm.com

Can You Change Your Structured Settlement Payment Structure Later?

Life throws curveballs. Your medical condition worsens and you need expensive treatments not covered by insurance. You get divorced and owe a property settlement. A business opportunity comes along requiring $75,000 in startup capital. Can you modify your structured settlement payment alternatives to free up cash?

Not directly. Once the annuity contract is signed, that payment schedule is carved in stone. You can't call Pacific Life or MetLife and say, "Instead of $2,000 monthly, send me $50,000 this month and reduce future payments." The annuity company won't budge—the contract is irrevocable.

Author: Olivia Carmichael;

Source: avayabcm.com

Your option is selling payment rights to factoring companies. These outfits purchase your future payments at steep discounts, handing you a lump sum today. You're receiving $1,800 monthly for 18 more years ($388,800 total). A factoring company might offer $195,000 cash right now. You sign over your payment rights; they collect the $388,800 over time.

Before any sale goes through, you're heading to court. The Structured Settlement Protection Act (adopted by 47 states) requires judicial approval. You file a petition, the judge schedules a hearing, and you must prove the sale serves your best interest. You'll sign disclosures confirming you understand you're receiving far less than the payments' face value.

Judges reject plenty of these requests. If you're selling payments to buy a boat or take a vacation, expect denial. If you're selling to avoid foreclosure or cover cancer treatments insurance won't pay for, you've got better odds.

The costs are brutal. Factoring companies discount future payments 40-70% depending on how far out the payments extend. Sell $100,000 in payments arriving over the next 15 years, you might receive $45,000-55,000. The factoring company pockets the difference. They're not charities—they're buying your payments as investments.

State regulations create a confusing patchwork. California requires factoring companies to disclose the effective annual interest rate (which can exceed 20%). Florida mandates specific consumer warnings. Some states barely regulate these transactions at all.

Before selling anything, explore alternatives. Can you borrow against future payments? Some specialty lenders offer loans secured by your structured settlement income—you get cash without permanently surrendering payments. Interest rates aren't cheap (8-15% typically), but you keep your payment stream.

Can family help? Can you adjust your budget? Can you find other income sources? Selling settlement payments should be your last option, not your first move when money gets tight.

If selling is unavoidable, sell the minimum amount necessary. Don't sell 20 years of payments to get $80,000 when selling five years of payments gets you the $35,000 you actually need. Keep as much guaranteed income as possible.

Three questions tell you the answer. First: Do you have serious investment knowledge—not dabbling in stocks, but genuine expertise managing substantial portfolios? Second: Do you absolutely need a large sum immediately for something specific and essential? Third: Can you honestly say you've never made a major financial mistake and you're confident managing hundreds of thousands of dollars? If you answered no to any question, periodic payments are probably your better choice

— Rebecca Martinez

Frequently Asked Questions About Structured Settlement Payments

Getting your structured settlement payment structure right matters more than almost any other financial decision you'll make. This isn't choosing a checking account—it's designing the income stream that'll support you through retirement, medical treatments, raising kids, or whatever your future holds.

Start by taking an honest look at yourself. How are you with money? Have you managed large amounts successfully before, or does cash tend to disappear? Most people benefit enormously from periodic payments that provide guaranteed income, tax advantages, and protection from spending mistakes.

Consider hybrid approaches. Grab enough upfront to handle urgent needs—medical bills, home modifications, getting out of debt—then structure the rest as monthly income you can count on long-term.

Work with professionals who know this stuff cold. A good attorney and a CFP with structured settlement experience will model different scenarios, show you the real math, and help you understand what each choice means 10, 20, 30 years from now. They cost money. They're worth it.

Build in inflation protection if your payments stretch beyond a decade. Either increasing payment schedules or periodic lump-sum boosts every few years. Without inflation protection, you're watching your purchasing power erode year after year.

Match payment timing to actual life events. When do kids start college? When does your mortgage balloon? When might you need expensive medical equipment? Structure payments around these realities instead of accepting some insurance company's standard template.

Resist the temptation to maximize upfront cash at the expense of long-term security. Yes, $100,000 today sounds amazing. But if it means inadequate monthly income for the next 25 years, you'll regret that choice before the year's out.

Structure conservatively. Build in more monthly income than you think you need right now. Your future self—dealing with expenses you didn't anticipate today—will thank you for that cushion.

Remember: once you sign the annuity contract, changes are difficult, expensive, and require court approval. Get it right the first time. Your structured settlement exists to provide financial security after injury or loss. Choose a payment structure that genuinely delivers that security, and you're setting yourself up for stability regardless of what curveballs life throws next.