Person choosing between lump sum payment and structured settlement periodic payments concept illustration

Structured Settlement Pros and Cons Guide

Content

Picture this: You've just settled a personal injury case. The defendant's attorney slides two documents across the table. One offers $500,000 today. The other promises $3,200 every month for the next twenty years. You have 72 hours to choose.

Most people freeze at this moment. They're still processing medical treatments, dealing with insurance adjusters, and trying to figure out how they'll pay next month's rent. Now they're supposed to make a financial decision that'll shape the next two decades?

Here's what nobody tells you during settlement talks: both options can be right. Or catastrophically wrong. It depends entirely on your situation—your age, your bills, whether you've ever balanced a checkbook, and a dozen other factors your lawyer probably hasn't asked about.

What Makes Structured Settlements Different from Lump-Sum Payments

Think of a structured settlement as converting your settlement into a personal pension plan. Instead of one massive check, you get scheduled payments. Maybe $2,500 monthly for fifteen years. Or $5,000 quarterly for life. Perhaps a mix—$100,000 now, then $1,800 monthly starting next year.

The Periodic Payment Settlement Act of 1982 created the legal foundation for these arrangements. Back then, Congress noticed that people were blowing through settlements within months, then ending up on government assistance. So they built in tax incentives to encourage periodic payments instead of lump sums.

Here's how it actually works: The defendant's insurance carrier buys an annuity from a life insurance company. That annuity funds your payments. Once purchased, it's set in stone. You can't call up the insurance company in five years and ask to switch things around.

Who ends up with these arrangements? Usually people with serious, permanent injuries. A construction worker who fell three stories and can't work anymore. A child injured in a car accident whose parents want the money protected until adulthood. Someone with traumatic brain injury who needs guaranteed income for care. Workers' comp cases frequently settle this way. So do wrongful death claims and medical malpractice awards.

What doesn't qualify? Employment lawsuits, punitive damages, sexual harassment settlements. The tax benefits only kick in for physical injuries or sickness. Everything else gets taxed like regular income.

The Core Advantages of Choosing a Structured Settlement

Guaranteed Income Stream and Financial Security

Let's say you're 38 years old. You've worked warehouse jobs your whole life. Now you can't lift anything over ten pounds due to a back injury. You've never made more than $35,000 annually.

Someone offers you $650,000 cash. How long would it last you?

Be honest. Could you make that money stretch for forty years? Would you invest it wisely? Or would your brother-in-law convince you to fund his "guaranteed" business opportunity? Would you upgrade to a nicer apartment, buy a decent car for once, help your mom with her mortgage?

A structured settlement at $2,800 monthly removes these temptations. It shows up every month whether the stock market crashes, housing prices tank, or cryptocurrency becomes worthless. The insurance company carries all investment risk. Even if their underlying investments implode, your check arrives on schedule.

This matters intensely when you're living on settlement income. When that monthly payment represents your only reliable money source, its predictability becomes more valuable than any potential investment returns.

Tax Benefits That Protect Your Settlement

Author: Olivia Carmichael;

Source: avayabcm.com

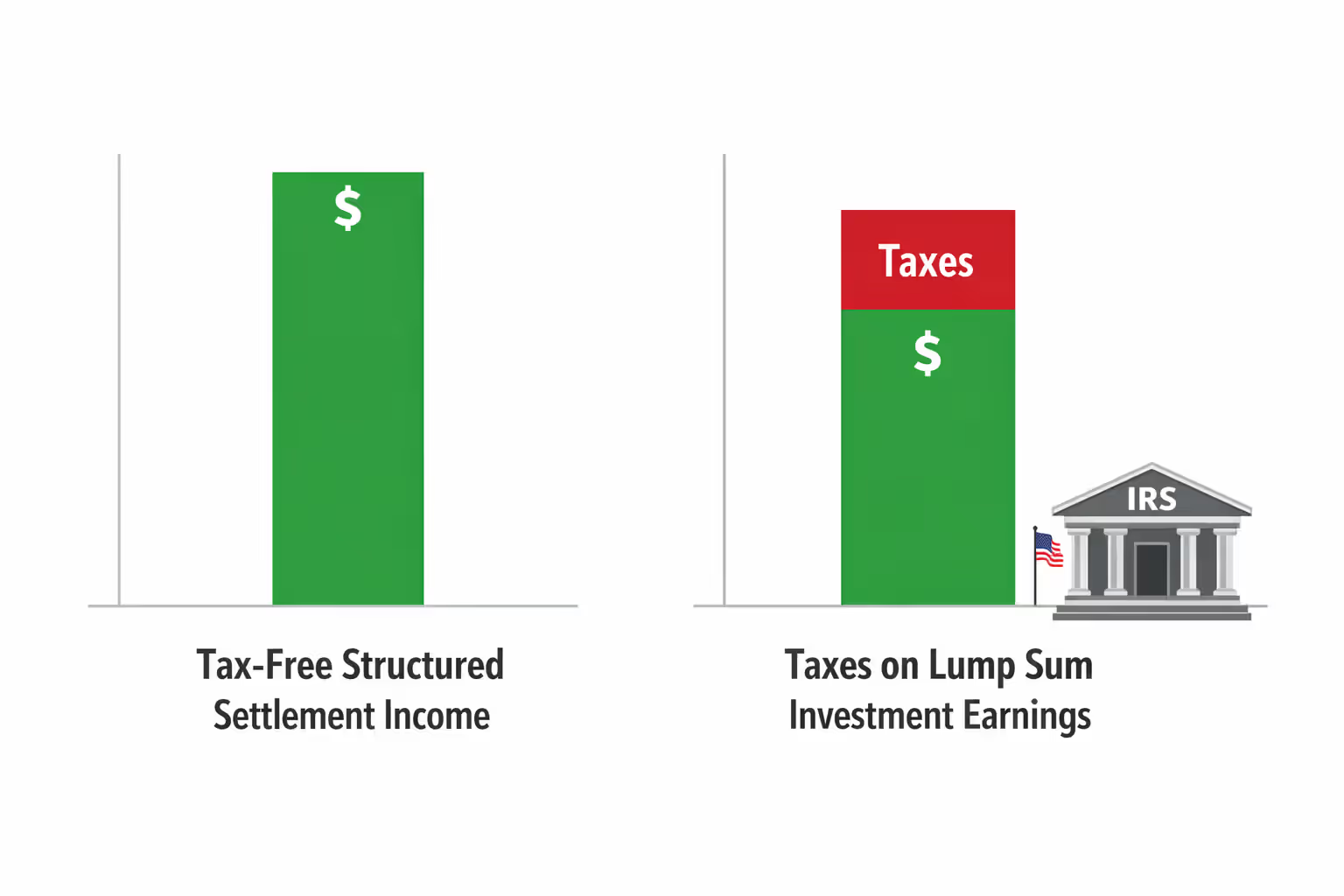

Personal injury structured settlement payments? Zero federal income tax. Zero state income tax in most places. The growth inside the annuity? Tax-free.

Now compare that to taking the lump sum. You invest $400,000 in a balanced portfolio. It earns 6% annually. You're paying capital gains taxes on stock profits. Income taxes on bond interest and dividends. Over twenty years, you'll surrender roughly $140,000 to $210,000 in taxes, depending on your bracket and where you live.

A structured settlement sidesteps this entirely. Every dollar that would've gone to the IRS stays in your pocket instead.

Quick example: Maria receives an $800,000 settlement at age 42. She takes the lump sum, invests conservatively, earns average returns. By age 62, she's paid about $195,000 in various taxes on investment income. Her friend Carlos took identical settlement money as structured payments. Tax bill? Zero.

The caveat: this only applies to physical injury cases. Emotional distress without physical symptoms? Taxable. Employment discrimination? Taxable. Even punitive damages tacked onto a physical injury case get taxed as ordinary income.

Protection from Poor Spending Decisions

Remember when you were 22 and blew your tax refund on stuff you can't even remember now? Imagine doing that with $500,000.

It happens constantly. Researchers who study lottery winners and inheritance recipients found that most people drain large lump sums within three to five years. Not through malice or stupidity—through a thousand small decisions that seem reasonable at the time.

Your cousin needs $15,000 to avoid foreclosure. Your daughter wants to go to a private college. That investment opportunity seems solid. The car you're driving is genuinely unsafe. Your girlfriend thinks you should buy a house together. Within eighteen months, $200,000 has evaporated, and you're not entirely sure where it went.

Structured settlements eliminate this risk. Can't blow money you don't have access to. When you're receiving $2,400 monthly, you're not buying a $65,000 truck. You're forced to live within the payment schedule, which—for many people—prevents financial catastrophe.

Particularly valuable if you've never handled significant money before. A 26-year-old who's worked fast food and retail jobs suddenly receives $700,000? That person has zero experience managing six figures. The structured settlement creates training wheels that might save them from themselves.

Customizable Payment Schedules

This isn't one-size-fits-all. You can design payment structures matching your life.

Need higher payments during your kids' college years? Structure it that way. Want increasing payments as you age to offset inflation? You can negotiate that. Prefer level payments for simplicity? That works too.

Real example: Jason, age 35, structured his $900,000 settlement as $1,500 monthly for living expenses, plus $30,000 every September for eight years to cover his son's college costs, plus $2,500 monthly starting at age 60 for retirement. His settlement works like a customized financial plan.

Or consider Emma, who has a degenerative condition. She arranged escalating payments—$1,800 monthly now, increasing to $2,500 at age 45, then $3,500 at age 55—anticipating higher care costs over time.

This customization disappears the moment you take the lump sum. Once that money hits your bank account, there's no structure beyond what you impose through discipline.

The Major Drawbacks You Should Consider

Limited Access to Your Money When Emergencies Arise

Life throws curveballs. Your teenager needs emergency dental surgery—$8,000. Your furnace dies in January—$6,500 for replacement. You lose your part-time job and need to cover gaps—$4,000.

With a structured settlement paying you $2,000 monthly, where does that money come from?

It doesn't. You're stuck. The settlement money exists, but it's locked away in future payments you can't touch. Unlike a savings account or brokerage account, you can't withdraw extra funds when emergencies hit.

This liquidity crisis creates genuine hardship. A 49-year-old getting $1,600 monthly manages regular bills fine but has no way to handle a $12,000 emergency without borrowing money at credit card rates or worse.

Some desperate people turn to "factoring companies"—businesses that buy future payments at predatory rates. They'll offer you $35,000 cash today for $70,000 in future payments. That's essentially a 100% interest rate. Even though courts must approve these sales in most states, judges typically rubber-stamp them if you claim financial need.

Once you've sold those payments, they're gone forever. No backsies. The money you needed for retirement or medical care just got cut in half.

Inflation Risk Over Long Payment Periods

Author: Olivia Carmichael;

Source: avayabcm.com

Three thousand dollars monthly sounds comfortable in 2026. What about 2044?

If inflation runs 3% annually—below the historical average—your $3,000 payment buys what $1,660 buys today after twenty years. Same payment amount. Everything costs more.

This problem intensifies with longer payment periods. A 28-year-old structuring payments over forty years faces enormous inflation risk. That fixed monthly amount that covers expenses at age 30 might barely pay utilities at age 60.

You can negotiate cost-of-living adjustments into structured settlements. But they're expensive. Adding COLA provisions typically reduces your initial payment by 20-30%. So instead of $3,000 monthly with no adjustments, you might get $2,200 monthly with 2% annual increases. Over decades, the COLA version pays more total dollars—but you sacrifice substantial income in the early years when you might need it most.

Most settlement recipients skip the COLA because they need higher immediate payments. Then they discover twenty years later that their fixed income doesn't stretch like it used to. By then, there's no remedy.

Loss of Investment Opportunity

Take that $450,000 lump sum. Work with a competent advisor. Invest in a diversified portfolio. Average 7% returns annually over twenty-five years.

You'd accumulate roughly $2.4 million.

Take the same $450,000 as structured payments over twenty-five years. Total payments: maybe $750,000.

That's the opportunity cost. The investment growth you forfeit by choosing guaranteed payments.

Now here's reality: most people don't achieve those returns. They panic during market crashes and sell low. They chase hot stocks and buy high. They pay excessive fees. They make emotional decisions. Research shows actual investor returns typically fall 3-4 percentage points below market returns due to behavioral mistakes.

So that theoretical 7% return? Most people actually earn 3-4%. Suddenly the structured settlement doesn't look as expensive.

But if you're financially disciplined, work with quality advisors, and can resist panic during downturns, you might legitimately achieve better returns than the structured settlement provides. That's real money left on the table.

The calculation hinges on honest self-assessment. Can you actually invest successfully? Or are you like most humans who make predictable behavioral mistakes when managing their own money?

Difficulty Changing Terms After Agreement

Sign the papers. Insurance company buys the annuity. Terms locked forever.

Then life happens. You get married. Have twins. Develop diabetes. Move across the country for a job opportunity. Get divorced. None of it matters—your payment schedule doesn't change.

This rigidity creates problems when the original structure poorly matches your needs. Maybe your lawyer rushed you into a standard structure without exploring alternatives. Maybe you didn't understand your own needs well enough. Maybe circumstances changed in unpredictable ways.

Tough luck. You're living with those decisions for decades.

A 35-year-old woman structured her settlement with level payments through age 70. Seemed reasonable. Then at 42, she developed rheumatoid arthritis requiring expensive biologics. Her fixed payments don't cover escalating medical costs. She needs higher payments now, lower later. Can't change it.

Unlike investment accounts where you can adjust your strategy, structured settlements offer zero flexibility after establishment. You're betting that decisions made today—possibly under stress, with incomplete information—will remain appropriate for twenty or thirty years. That's a risky bet.

How Structured Settlements Compare to Lump-Sum Payouts

| Feature | Structured Settlement | Single Lump Sum |

| Getting money when you need it | Very restricted—you receive only the scheduled amount regardless of circumstances | Unrestricted—withdraw whatever you need whenever you need it |

| Taxes on personal injury settlements | No federal or state income taxes on payments or growth | No taxes on the settlement itself, but you'll pay taxes on all investment earnings |

| Who decides where money gets invested | Insurance company controls all investment decisions through the annuity | You make all investment choices, for better or worse |

| Protection if you're sued or face creditors | Usually well-protected under state law—creditors often cannot touch future payments | Protection varies dramatically by state—creditors may seize funds to satisfy judgments |

| How rising prices affect your buying power | Your purchasing power steadily declines unless you negotiated inflation adjustments upfront | You can invest in assets that historically outpace inflation like stocks or real estate |

| How much money you ultimately receive | Fixed total determined at settlement—typically worth less in today's dollars than the lump sum | Depends entirely on investment performance—could be substantially more or considerably less |

| Ability to adapt to changing circumstances | Essentially zero—you're locked into the payment schedule permanently | Complete freedom to adjust your approach as life changes |

| Financial risk you're taking | Minimal—guaranteed payments backed by insurance company reserves and state guaranty funds | Depends on your investment choices and spending discipline—could lose significant value |

These settlement annuity tradeoffs reveal that neither choice beats the other in every scenario. Your circumstances determine which drawbacks matter most and which advantages you actually need.

Five Critical Factors That Should Drive Your Decision

Your current age and how long you'll likely live fundamentally change this calculation. A 27-year-old facing fifty-plus years of inflation faces entirely different risks than a 62-year-old planning for twenty years.

Younger recipients get hammered by inflation. That $2,800 monthly payment at age 30 becomes nearly worthless by age 70 without cost-of-living adjustments. But COLA provisions slash your initial payments substantially. A young person might need shorter payment periods or aggressive inflation protection.

Age also drives annuity pricing. A lifetime payment option for a 28-year-old costs the insurance company vastly more than the same option for a 65-year-old. So younger recipients receive smaller monthly payments for equivalent settlement amounts. The insurance company's calculating they'll be paying for fifty years instead of fifteen.

Your existing debts and financial obligations matter immediately. Carrying $90,000 in medical bills, $40,000 across credit cards, mortgage payments three months behind, and a car about to get repossessed?

You need cash now. Structured payments arriving at $2,500 monthly won't solve a crisis requiring $150,000 immediately. Creditors won't wait for your payments to accumulate. They'll sue, get judgments, garnish your wages, and wreck your credit.

In financial crisis mode, the lump sum becomes almost mandatory. You must resolve current obligations before worrying about long-term income security.

Conversely, walking into settlement negotiations debt-free with manageable expenses? The structured settlement's income guarantee becomes much more attractive. You can afford to prioritize stability over liquidity.

Your financial literacy and access to professional guidance determines whether you can responsibly handle a large lump sum. Requires brutal honesty.

Never maintained a budget? Don't understand the difference between stocks and bonds? History of impulsive purchases? Maybe structured payments save you from predictable mistakes.

Planning to work with a fee-only certified financial planner and actually follow their advice? That professional guidance dramatically improves lump sum outcomes. Good advisors typically charge around 1% annually. That fee buys investment management, tax planning, and behavioral coaching that might generate returns exceeding what structured settlements provide.

But if you're planning to manage everything yourself despite limited experience—because paying advisors seems wasteful—you're probably better off with structured payments. Most people overestimate their financial abilities and underestimate how behavioral biases sabotage investment returns.

Author: Olivia Carmichael;

Source: avayabcm.com

Your healthcare situation represents one of the most critical structured settlement decision factors. Ongoing medical conditions requiring regular treatment? Predictable monthly income ensures premiums, medications, therapy, and equipment costs get covered regardless of other financial pressures.

Need major surgery or expensive durable medical equipment immediately? Structured payments arriving slowly don't help. You need accessible funds now, not spread across years. Someone facing $175,000 in immediate surgical costs cannot wait for monthly payments to accumulate—they need the lump sum to pay surgeons and hospitals upfront.

Also consider future medical needs. Conditions that worsen over time might require escalating payments. Static conditions might need level income. Degenerative diseases argue for structured settlements with increasing payments. One-time corrective procedures argue for lump sums.

State laws where you live affect both options differently. Some states aggressively protect structured settlement payments from creditors. Others provide minimal protection. Your state's annuity guaranty association determines what happens if your insurance company fails.

Research your state's structured settlement protection statutes. Does your state require court approval before factoring companies can buy your payments? What coverage limits apply if the insurance carrier becomes insolvent? Are your payments exempt from bankruptcy proceedings?

States with strong consumer protections make structured settlements more secure. States with weak regulations increase risks for both options but particularly affect structured settlements since you can't easily exit them if problems arise.

Common Mistakes People Make When Evaluating Settlement Options

Underestimating what healthcare will cost you down the road destroys more financial plans than any other mistake. People assume their current medical status remains stable. It rarely does.

That manageable back injury at 33? Could require surgery, pain management, physical therapy costing $30,000 annually by age 48. The knee replacement you're delaying? Might become urgent. New conditions develop. Injuries create secondary problems. Bodies age.

Medical inflation consistently runs 5-7% yearly compared to overall inflation of 2-3%. If you're structuring payments without accounting for healthcare costs rising twice as fast as everything else, your fixed income becomes increasingly inadequate.

Particularly dangerous for younger recipients. A 29-year-old structuring payments through age 60 faces thirty years of medical cost increases that'll dramatically outpace their fixed income.

Ignoring what future payments are actually worth today leads people to choose structured settlements based on impressive-sounding totals. Insurance company offers $1.1 million paid over twenty-five years versus $580,000 lump sum today. That $1.1 million sounds massively better.

Except it's not.

Run a present value calculation at 5% discount rate. Those future payments are worth roughly $510,000 in today's dollars. The $580,000 lump sum is financially superior by $70,000 despite the lower nominal total.

Use present value calculators before comparing options. Plug in each payment with its timing. Use discount rates between 4-6% reflecting safe investment returns. Compare the present value to the lump sum offered. You'll frequently discover that structured settlements promising huge totals actually deliver less value than smaller lump sums.

Accepting the insurance company's first structure proposal without negotiating alternatives leaves money on the table. Most people don't realize these terms are completely negotiable.

Insurance companies prefer simple structures—level payments, standard schedules—because they're administratively easier and cheaper to fund. But you don't work for their convenience.

Want higher payments for ten years, then lower? Negotiate it. Need a large payment in year five for planned expenses? Request it. Prefer increasing payments to partially offset inflation? Insist on it.

Experienced settlement attorneys negotiate terms matching your anticipated needs rather than accepting whatever the defendant offers initially. This customization can create tens of thousands in additional value compared to standard structures.

Making this decision without professional guidance handicaps you during the most important financial choice you'll ever make. Settlement negotiations move quickly. Insurance companies employ people who structure settlements daily. You're doing it once, probably while stressed and recovering.

Trying to figure this out alone puts you at enormous disadvantage.

A qualified financial advisor models both options using your specific tax situation, investment assumptions, and spending needs. They run scenarios showing what happens if you live to 95 versus 75. What if you need long-term care? What if investment returns disappoint?

Settlement attorneys protect your legal interests and ensure agreements include appropriate safeguards. They've seen every way these deals go wrong and can prevent those outcomes.

These professionals typically cost $3,000-$8,000 combined. Trivial compared to lifetime financial impact of choosing poorly. Yet most people skip this step and decide based on gut feeling or whoever sounds most confident.

Author: Olivia Carmichael;

Source: avayabcm.com

Selling payment rights when you panic about money transforms a solid decision into financial disaster. People choose structured settlements for good reasons. Then emergencies arise. They panic. They Google "sell structured settlement payments." Suddenly they're in factoring company offices signing away their future.

These transactions typically cost 40-60 cents per dollar of payments you're selling. You receive $40,000 today for $80,000 in payments you'd receive over three years. While courts must approve sales in most states, judges usually approve them if you claim hardship.

Once completed, there's no undoing it. That money is gone. The income you needed for retirement or medical care just got slashed nearly in half.

Before selling payments, exhaust every alternative. Personal loans from banks or credit unions. Payment plans with creditors. Local assistance programs. Family loans. Bankruptcy if debts are overwhelming. Almost anything beats selling structured settlement rights at factoring company rates.

In my twenty-three years advising settlement recipients, the clients who benefit most from structured settlements share common traits: permanent disabilities requiring lifelong support, limited experience managing significant assets, or honest acknowledgment that they lack financial discipline. I've watched too many cases where someone insisted on the lump sum despite clear warning signs, then called three years later broke and desperate. When a client needs that money to last their lifetime and either lacks the skills or temperament to manage a large sum responsibly, the structured settlement's guaranteed income provides security that no investment portfolio can replicate, because it removes the human behavior element that destroys most financial plans

— Jennifer Martinez

Frequently Asked Questions About Structured Settlements

Certain situations make structured settlements the obviously superior choice. Catastrophic injuries requiring lifetime care create perfect scenarios—the guaranteed income ensures ongoing medical needs get funded regardless of economic conditions or personal financial management ability.

Someone paralyzed in an accident faces decades of care costs. Wheelchair maintenance, home modifications, personal care attendants, specialized medical equipment, ongoing therapy. These expenses don't stop if the stock market crashes or if the person makes poor investment choices. Structured settlements ensure money keeps arriving to fund necessary care.

Minors receiving settlements benefit enormously from structured arrangements. A 12-year-old receiving a $550,000 settlement faces catastrophic risks if given lump-sum access at 18. Structuring payments to begin at 25 or 30, gradually increasing over time, protects against youthful financial mistakes while preserving funds for education, housing, and long-term needs. Many states require court approval for minor settlements, and judges typically mandate structured payments for substantial awards.

People who've demonstrated poor financial management should seriously consider structured settlements. Previous bankruptcy? Struggled with gambling problems? History of impulsive major purchases? The forced discipline of periodic payments might prevent depleting the settlement within months.

Red flags suggesting lump sums might work better: significant existing debt requiring immediate resolution, strong financial literacy combined with access to quality advisors, relatively short life expectancy reducing long-term inflation concerns, and specific plans requiring substantial upfront capital that genuinely improve your situation (like purchasing an accessible home or specialized vehicle).

The decision ultimately requires brutal self-honesty. Will you actually manage a lump sum responsibly, or will it disappear within thirty months? Do you need flexibility to address unpredictable expenses, or do you value security of knowing income arrives regardless of circumstances? Can you realistically achieve investment returns exceeding what the structured settlement provides, or will behavioral mistakes torpedo your returns?

Neither option is universally better. Structured settlements trade flexibility and inflation protection for security and tax benefits. Lump sums offer control and growth potential but require discipline and competence to manage successfully.

The best choice depends on your specific circumstances—your age, health, existing obligations, money management abilities, and what you genuinely need this settlement to accomplish over your lifetime. Not what sounds appealing in the moment. Not what your cousin says you should do. What actually serves your long-term interests based on honest assessment of your capabilities and needs.

Take time modeling both options carefully with professional help before deciding. This choice affects your financial security for decades. Rushing it or choosing based on gut feeling rather than rigorous analysis creates regrets that last a lifetime. Use the structured settlement pros and cons outlined here to guide evaluation, but ultimately weigh these factors against your unique circumstances and honest assessment of your strengths and limitations.