Stack of legal settlement documents on a desk with a calculator, pen, and glasses, one line highlighted with a red marker showing payment figures

How to Calculate Structured Settlement Interest Rates for Your Payout

Content

Your settlement paperwork arrived yesterday. Three hundred pages of legal language, payment schedules, and insurance company letterhead. You've flipped through it twice looking for one simple number: the interest rate.

It's not there.

Settlement agreements don't work like your savings account statement. There's no bold "3.75% APY" printed at the top. The rate is buried inside the math—hidden in the relationship between what you could've taken as cash today versus what you'll receive in monthly checks over the next twenty years.

I've seen people sign settlements worth $500,000 without realizing the implied rate was barely 2.4%. Others negotiated their way to 4.1% on similar deals. Over two decades, that 1.7% difference translates to $87,000 in real value. Same injury, same defendant, wildly different outcomes.

Most lawyers won't walk you through this calculation. They're great at maximizing your total settlement amount, but the interest rate mechanics? That falls into a knowledge gap between legal expertise and financial planning.

Here's what you actually need to know.

What Determines Your Structured Settlement Interest Rate

Let's start with basics. You're getting $400,000 to settle your case. Two options sit in front of you:

- Option A: $400,000 cash, wired to your account next week

- Option B: $2,000 every month for 25 years (that's $600,000 total)

Option B looks like $200,000 extra. It's not. That difference represents the time value of money—compensation for waiting years to access funds you could've had immediately. Think of it as interest working backward.

Multiple variables shape what insurance companies offer:

The broader interest rate climate drives everything. Right now, with 10-year Treasuries paying around 4%, settlement rates cluster between 2.5% and 4.5%. Back in 2020 when Treasuries dropped to 1%? Settlement rates bottomed out at 1.8% to 3.2%. Insurance carriers fund your future payments by buying bonds today. When bond yields fall, so do settlement rates. The connection is direct.

Your age matters more than you'd expect. A 30-year-old accepting lifetime payments might see rates a full percentage point lower than a 60-year-old with identical terms. Why? The insurance company assumes they're paying that 30-year-old for fifty-plus years versus maybe twenty for the 60-year-old. Longer payout periods mean lower rates.

Payment timing creates leverage. Tell the insurance company you don't need money for ten years, and suddenly your rate jumps. I've seen deferred settlements offer 1.5% to 2% higher rates than immediate payment structures. The insurer gets a decade to invest your premium before cutting the first check. That runway has value, and they'll share some of it with you.

Not all insurance companies price identically. Shop your settlement among five qualified carriers, and you'll get five different quotes. One offers $1,850 monthly, another $2,020 for the same premium. That spread represents a 0.8% rate difference. Your attorney should be shopping this aggressively, but many don't. Ask them specifically which carriers they've contacted.

How Insurance Companies Calculate Structured Settlement Rates

Author: Christopher Vaughn;

Source: avayabcm.com

Forget the idea that insurers simply apply a fixed interest rate to your settlement. The actual process involves layering several financial components into what actuaries call "annuity settlement rate factors."

Treasury and corporate bond yields form the foundation layer. When structuring your payout, the carrier buys a portfolio of highly-rated bonds with maturity dates matching your payment schedule. You're getting paid for thirty years? They're building a bond ladder—maybe twenty different bonds maturing at staggered intervals across three decades. What they pay for those bonds directly determines what they can offer you.

January provides a useful snapshot. Ten-year Treasuries were yielding 4.2%. Structured settlements that month implied rates between 3.1% and 4.0%, depending on structure specifics. That gap—roughly 1.1% on the wide end—represents the insurer's costs and profit.

Actuarial tables enter the picture for lifetime structures. Insurance companies rely on mortality data (the Annuity 2000 Mortality Table is common, though newer versions exist) to project payment duration. A 45-year-old man has maybe 35 years of statistical life expectancy. But statistics don't matter if you're the guy who lives to 98. The insurer must price for that possibility.

This longevity risk gets baked into your rate as a cost. They shave off somewhere between 0.3% and 0.8% compared to fixed-period payments to cover the chance you outlive their projections by decades.

Administrative overhead and profit margins take another bite. Setting up annuities, maintaining payment systems for thirty years, holding regulatory capital reserves—these aren't free. Nor is the profit the insurance company expects to earn. Together, these factors consume another 0.5% to 1.2% of the rate spread between what bonds yield and what you receive.

Let's compare what different guaranteed investments actually pay:

| Investment Type | What It Pays | Tax Situation | Safety Net | Getting Your Money Back |

| Structured settlements | 2.8% to 4.2% | Zero taxes on injury settlements | State backup funds cover up to $250k if insurer fails | Nearly impossible—courts rarely approve sales |

| Treasury bonds (10-year) | 3.8% to 4.5% | Federal taxes yes, state taxes no | US government guarantee | Sell anytime during market hours |

| Bank CDs (5-year) | 2.5% to 4.8% | Taxed as regular income | FDIC protects $250k per bank | Penalties for early withdrawal |

| A-rated corporate bonds | 4.5% to 5.8% | Taxed as regular income | Only as safe as the company | Secondary market available |

| Municipal bonds | 2.8% to 4.0% | Usually exempt from federal and state taxes | Depends on issuer | Secondary market available |

Personal injury settlements grow tax-free under Section 104(a)(2) of the tax code. This creates hidden value that raw percentages don't capture. A 3.5% tax-free return equals roughly 5.4% taxable if you're in the 35% combined bracket. Suddenly that "low" settlement rate looks competitive.

Understanding Discount Rates in Settlement Buyouts

Five years pass. You're receiving your $2,000 monthly checks like clockwork. Then your car dies, your roof needs replacing, and your kid needs braces. All in the same month. You start Googling "sell my structured settlement."

Welcome to the discount rate world—which operates completely differently from your original settlement rate.

Factoring companies (the businesses that buy settlement payment streams) apply discount rates between 9% and 18% when calculating what they'll pay for your future money. Your settlement implied a 3.8% rate when you accepted it, but that number becomes irrelevant in the secondary market.

Here's the math: You're receiving $2,000 monthly for the next ten years. That's 120 payments totaling $240,000 face value. A factoring company offers $140,000 cash today. They're applying roughly a 12% discount rate—meaning they value your future payments at 12% less per year than nominal value to cover their costs, risk, and profit.

How these companies determine discount rates:

Their cost of capital sets the floor. If they're borrowing money at 7% to buy structured settlements, they need to earn more than 7% to justify the business. Most add 3% to 8% on top to cover operating costs, risk (if you die early, they lose future payments), and profit margin.

Market competition matters enormously. In areas with multiple buyers competing, discount rates might compress to 9% to 11%. Smaller settlements under $50,000 in less competitive markets? I've seen 16% to 18% rates routinely.

Payment timing affects pricing significantly. Buying payments starting next month carries less risk than payments beginning five years out. Near-term payments typically get 9% to 10% discounts. Deferred payments might face 14% to 16% haircuts.

Warning signs of predatory pricing:

Anything above 18% discount rates screams problem, especially for settlements backed by A-rated insurers with essentially zero default risk. Watch for:

- Companies refusing to disclose their discount rate in writing

- "Offer expires in 48 hours" pressure tactics

- Offers significantly below market without clear explanation

- Different discount rates applied to various payment chunks without justification

- Marketing that specifically targets vulnerable people (recent accident victims, people in financial crisis)

The secondary market cleaned up considerably after states tightened regulations in the 2000s, but you'll still find bad actors. Any legitimate buyer should transparently disclose their discount rate and show you the present value calculation so you can verify it independently. If they won't put the discount rate on paper, walk away immediately. Competitive bids for quality settlements should land between 9% and 13% in today's market. Anything crossing 15% deserves serious scrutiny and comparison shopping with at least three other buyers

— John Smith

Step-by-Step: Modeling Your Settlement's True Interest Rate

Calculating your settlement's implied rate requires working backward from the payment schedule—reverse-engineering the math. This section walks through the actual process.

The core concept is simple: Would you rather have $100 right now or $100 five years from now? Obviously now, right? Not just inflation concerns—you could invest that $100 and have maybe $125 in five years. The interest rate that makes you indifferent between money today and money later becomes your implied settlement rate.

Present value calculations, stripped to basics:

For a single future payment, the formula looks like this: PV = FV / (1 + r)^n

PV is present value (what it's worth today), FV is future value (the payment amount), r is the interest rate, and n equals years.

Structured settlements with monthly payments for twenty years? You calculate present value for each of those 240 payments individually, then add them up. When that total equals the lump sum you gave up, you've found your implied rate.

Walking through a real example:

Say you accepted a structured settlement instead of $300,000 cash. Your settlement pays $1,500 monthly for twenty years—240 total payments adding up to $360,000 nominal.

Finding the implied annual rate:

- You calculate present value of all 240 payments at different interest rates until PV hits $300,000

- Try 2% annually (that's 0.167% monthly): PV comes to approximately $294,000

- Try 3% annually (0.25% monthly): PV drops to roughly $272,000

- Try 2.5% annually: PV calculates to about $283,000

- Keep iterating until you land on approximately 2.2% annually

Your $300,000 grew to $360,000 over twenty years at an effective 2.2% annual rate. That's your answer.

Tools that actually work for these calculations:

Financial calculators like the HP 12C or Texas Instruments BA II Plus can solve for interest rates when you input payment streams. Most attorneys and settlement planners already own these.

Online calculators exist free at sites like Calculator.net or Investor.gov. You plug in payment amounts, frequency, and duration, then adjust interest rate until present value matches your lump sum alternative.

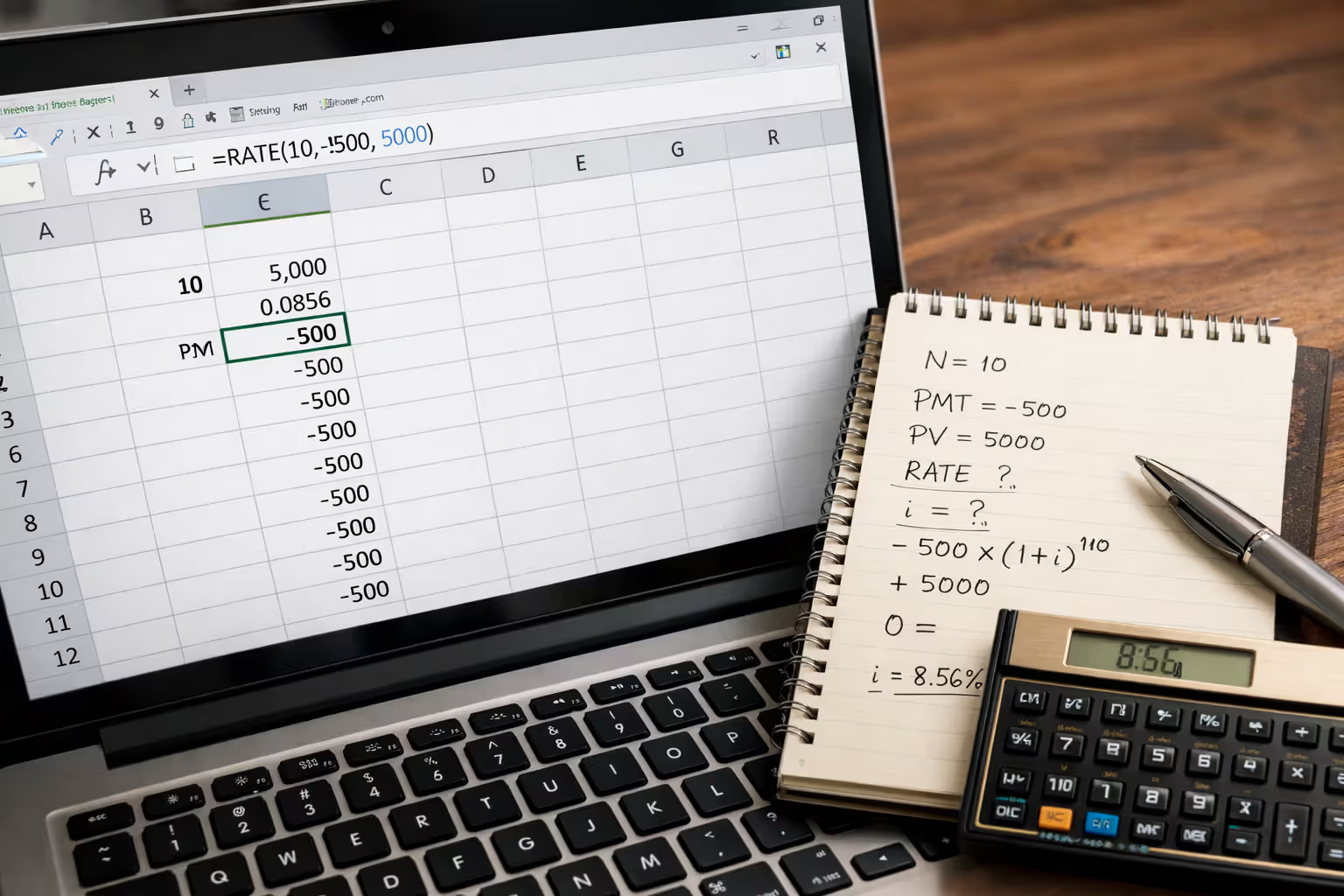

Excel or Google Sheets have built-in functions that handle this. The RATE function calculates implied interest: =RATE(number_of_payments, payment_amount, -lump_sum_alternative, 0) returns your periodic rate. Multiply by payment frequency for annual rate.

Professional software like Settlement Genius or StructCalc (used by settlement planners) provides sophisticated calculations accounting for payment timing variations and life contingencies. These typically cost $200 to $800 yearly, so probably overkill unless you're analyzing settlements professionally.

Common Mistakes When Evaluating Settlement Interest Rates

Comparing fundamentally different investment types: I constantly see people compare structured settlement rates to stock market historical returns. "Why would I take 3.5% when the S&P 500 averages 10%?" they ask.

Because they're not remotely comparable investments. Your settlement pays 3.5% guaranteed for twenty-five years regardless of market crashes, recessions, or your own financial mistakes. That certainty carries enormous value, particularly for people who lack investment experience or discipline.

Better comparison? Stack settlements against other guaranteed fixed-income investments—Treasury bonds, fixed annuities, CDs. Once you factor in tax benefits, settlements often look quite competitive.

Forgetting about taxes entirely: Personal injury structured settlements grow completely tax-free under IRC Section 104(a)(2). This advantage compounds dramatically over time.

A 3% tax-free rate effectively equals about 4.6% taxable for someone in the 35% bracket, or 4.1% taxable in the 25% bracket.

I've watched people compare their 3% settlement rate to a 5% CD without recognizing they'll pay taxes on that CD interest every single year. After taxes, that 5% CD nets maybe 3.25%. Suddenly the structured settlement doesn't look so bad.

Underestimating inflation's bite: Fixed payment settlements lose purchasing power relentlessly. Your $2,000 monthly check feels comfortable today. In twenty years? Not so much.

At 3% annual inflation, $2,000 twenty years from now buys what roughly $1,100 buys today. That's nearly half the purchasing power gone.

Author: Christopher Vaughn;

Source: avayabcm.com

Some people assume the higher nominal total ($360,000 over twenty years versus $300,000 lump sum) protects them from inflation. It doesn't—not unless your implied interest rate exceeds the inflation rate. With settlement rates around 2% to 3% and historical inflation averaging 3%, many settlements actually lose ground in real terms.

Overlooking guaranteed payment provisions: Most structured settlements include continuation provisions—if you die before payments end, your beneficiaries receive the balance. This death benefit protection carries value that simple interest calculations miss entirely.

You're receiving $2,000 monthly for twenty years. You die after year five. Your beneficiaries get the remaining fifteen years of payments, often as a lump sum present value. This guarantee costs the insurance company money, which shaves your implied rate slightly but provides significant estate planning value.

When to Accept or Negotiate Your Settlement Rate Offer

Benchmarking against current market conditions requires knowing Treasury yields and typical spreads. General rule: settlement implied rates should fall within 0.5% to 1.5% below current 10-year Treasury yields for immediate payments, or 0.2% to 1.0% below for deferred structures.

If 10-year Treasuries yield 4.3% and your immediate payment settlement implies 2.5%, that 1.8% spread is unusually wide. You've got room to negotiate or shop other insurers. A 3.5% implied rate with the same Treasury yield (0.8% spread) falls within normal parameters.

Check current Treasury yields at TreasuryDirect.gov. Calculate your settlement's implied rate using the methods above. Spreads exceeding 1.5% for immediate payments or 1.2% for deferred payments deserve questions.

Where you have negotiation leverage:

Before signing settlement documents, you hold maximum leverage. After signing? Rates are locked permanently. Your attorney or settlement planner should obtain competitive quotes from at least three insurers rated A or better by A.M. Best. Competition drives better pricing.

Settlement size matters. A $1 million settlement represents meaningful premium volume—insurers will sharpen their pencils. Settlements under $100,000 often get less competitive rates because administrative costs eat up larger percentages.

Payment timing flexibility creates opportunities. If you can defer payment start dates by two to five years, insurers frequently improve rates by 0.3% to 0.7%. They get extra time to invest your premium before making the first payment.

Author: Christopher Vaughn;

Source: avayabcm.com

Alternative structures that boost effective returns:

Cost-of-living adjustments (COLAs) combat inflation but reduce initial payments. A 3% annual COLA might cut your first payment by 20% to 30%, but subsequent payments grow each year, maintaining purchasing power better than fixed amounts.

Balloon payments or step-up structures concentrate more money in later years when the insurer has had longer to invest. Maybe $1,000 monthly for ten years, then $3,000 monthly for the next ten years. This structure often produces 0.2% to 0.5% higher implied rates than level payments.

Hybrid approaches combining guaranteed periods with lifetime payments can optimize rates. Instead of pure lifetime payments (lower rates due to longevity risk), structure twenty years guaranteed with lifetime continuation afterward. This frequently improves rates for the guaranteed period while maintaining lifetime security.

Frequently Asked Questions About Settlement Interest Rates

Structured settlement interest rates operate in a specialized corner where insurance pricing, tax law, and long-term security intersect. The embedded rate in your settlement—though never explicitly stated anywhere—determines whether you're receiving fair value for surrendering immediate access to a lump sum.

Most people receiving settlements never calculate their implied rate. They trust attorneys and settlement planners negotiated effectively. Often that trust is warranted. But understanding the settlement annuity interest explanation yourself provides confidence and occasionally reveals improvement opportunities before signing.

The critical insight: evaluate structured settlement rates not against stock market returns or high-yield investments, but against other guaranteed fixed-income alternatives. When you account for tax advantages, guaranteed payment features, and protection from investment mistakes, a 3.5% tax-free structured settlement rate frequently delivers more value than a 5% taxable CD or bond—despite the lower nominal number.

If you're currently evaluating a structured settlement offer, calculate the implied rate using these methods, benchmark it against current Treasury yields, and confirm your attorney obtained competitive quotes from multiple insurers. Those steps alone can improve your settlement value by tens of thousands of dollars over its lifetime.