Structured settlement agreement document on office desk with calculator and growing coin stacks representing periodic payments

How Structured Settlements Work From Negotiation to Payment

Content

When you settle a personal injury lawsuit, accepting a structured settlement means agreeing to receive compensation over time instead of in one lump sum. The process involves multiple parties, legal safeguards, and a specialized financial product called an annuity that guarantees your future payments. Understanding each phase—from initial negotiations through decades of payments—helps you make informed decisions and avoid costly mistakes.

What Happens During the Structured Settlement Negotiation

Structured settlement discussions typically begin after liability becomes clear but before final settlement terms are signed. Your attorney and the defendant's insurance company negotiate not just the total value, but whether payments should be immediate, delayed, or spread across years.

During a typical personal injury case, the defendant's liability insurer calculates their maximum exposure. Once both sides agree settlement makes sense, the insurer's claims adjuster often proposes a structured option alongside a lump sum offer. For example, they might offer $300,000 cash today or $450,000 paid over 20 years. The higher structured amount reflects the time value of money and the insurer's ability to fund future payments at a lower present cost.

The negotiation phase addresses several critical elements that cannot be changed later. You and your attorney decide the payment start date, frequency, duration, and whether you want any immediate cash. Some claimants need $50,000 immediately for medical bills and home modifications, then prefer monthly income afterward. Others choose to delay all payments for years, allowing the settlement to grow before distributions begin.

Your age, injury severity, ongoing medical needs, and financial sophistication all influence these discussions. A 30-year-old paralyzed in an accident might structure payments to replace lost wages until retirement age, then increase payments to cover long-term care. A minor's settlement almost always involves court-supervised structures that prevent access until age 18 or later.

Author: Andrew Halvorsen;

Source: avayabcm.com

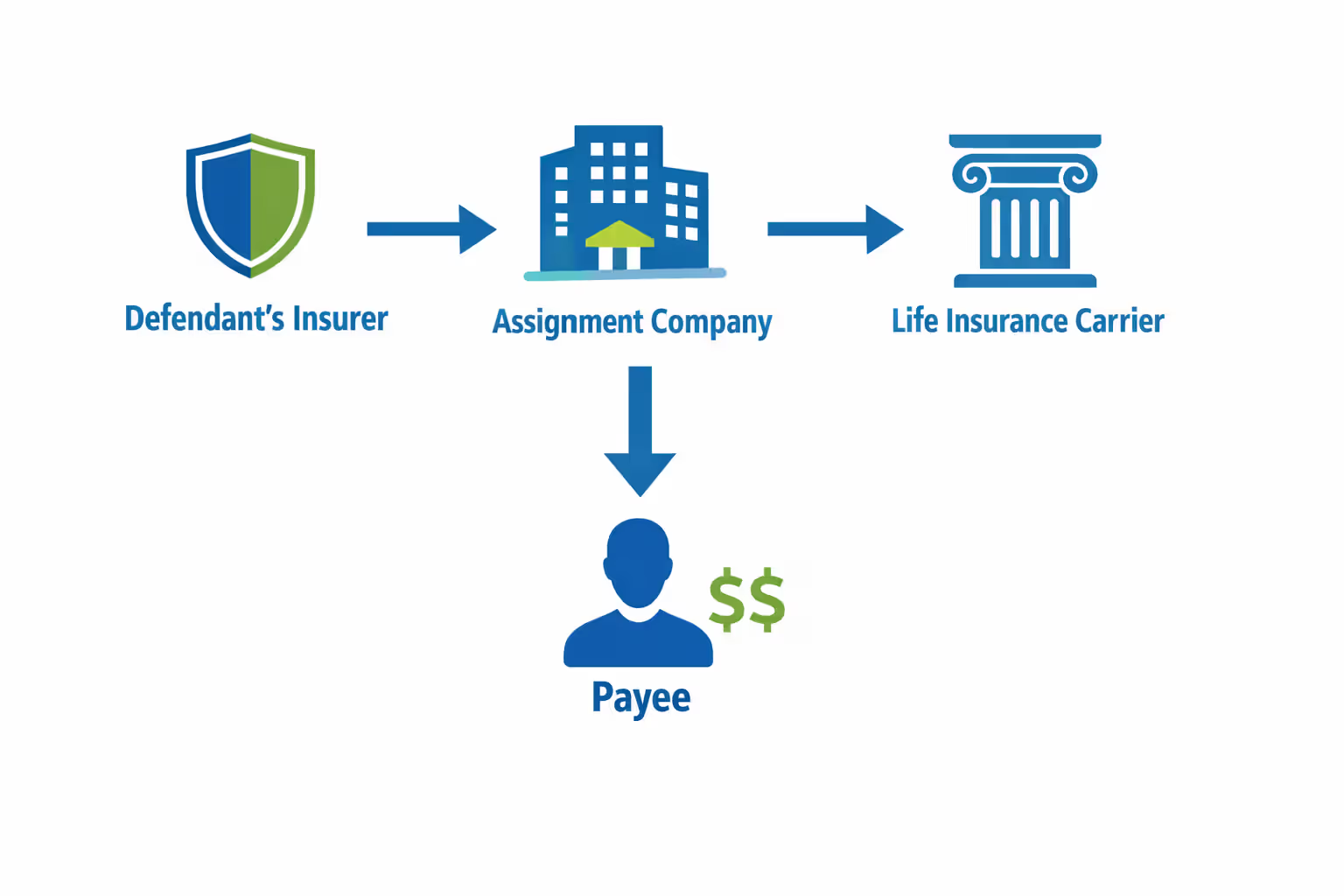

The defendant's insurer participates in structuring negotiations but rarely funds the payments directly. Instead, they transfer this obligation to a qualified assignment company, which then purchases the annuity. This separation protects you if the defendant's insurer faces financial trouble years later.

Structured settlements provide financial security and tax advantages that a lump sum simply cannot match, particularly for individuals who have never managed large amounts of money

— Frank Kilpatrick

The Role of Annuities in Funding Your Settlement

Once you agree to settlement terms, the defendant's insurance company pays a single premium to an assignment company, which immediately purchases a qualified annuity from a highly-rated life insurance carrier. This annuity becomes the engine that funds your future payments.

Annuities work through a simple principle: the life insurance company receives a lump sum today and contractually promises specific payments in the future. Because they invest conservatively and calculate payments using actuarial tables, they profit from the spread between investment returns and payment obligations. For a $400,000 annuity paying you $2,000 monthly for 25 years, the life insurer might earn 4-5% annually while your payments remain fixed.

The structured settlement annuity payment mechanics guide this entire arrangement. Unlike variable annuities sold for retirement, structured settlement annuities are "qualified" under IRC Section 130, meaning they're specifically designed for injury compensation. They cannot be surrendered for cash value, borrowed against, or altered after purchase. This inflexibility protects payments from creditors, bankruptcy, and impulsive decisions.

Who Actually Holds Your Settlement Money

The assignment company—not you—owns the annuity contract. This legal structure is fundamental to how structured settlements work. The defendant's insurer pays the assignment company, which assumes the periodic payment obligation. The assignment company then purchases an annuity naming itself as owner and you as payee.

This arrangement seems counterintuitive, but it serves important purposes. First, it releases the defendant and their insurer from future obligations. Once they pay the assignment company, their involvement ends. Second, assignment company ownership preserves the tax-free status of your payments under IRC Section 104(a)(2). If you owned the annuity directly, complex tax issues could arise.

Author: Andrew Halvorsen;

Source: avayabcm.com

You never control the principal, which frustrates some recipients who later want access. However, this separation also means the annuity cannot be seized in lawsuits against you, doesn't count as an asset for government benefit eligibility in many cases, and can't be drained by bad financial decisions.

Why Life Insurance Companies Issue the Payments

Life insurance carriers issue structured settlement annuities because their business model perfectly matches the obligation. They already manage long-term liabilities, maintain reserves required by state regulators, and invest in bonds and securities that provide steady returns over decades.

State guaranty associations provide another safety layer. If a life insurance company becomes insolvent, state guaranty funds cover annuity payments up to certain limits—typically $250,000 in present value, though limits vary by state. This protection mirrors FDIC insurance for bank deposits, though it's funded differently.

Only life insurers with high financial strength ratings (typically A- or better from A.M. Best) participate in the structured settlement market. Assignment companies and brokers maintain approved lists of carriers. Even so, diversifying large settlements across multiple insurers reduces concentration risk if one carrier weakens over time.

Step-by-Step: From Court Approval to First Payment

The structured settlement lifecycle guide follows a predictable sequence, though timing varies by jurisdiction and case complexity.

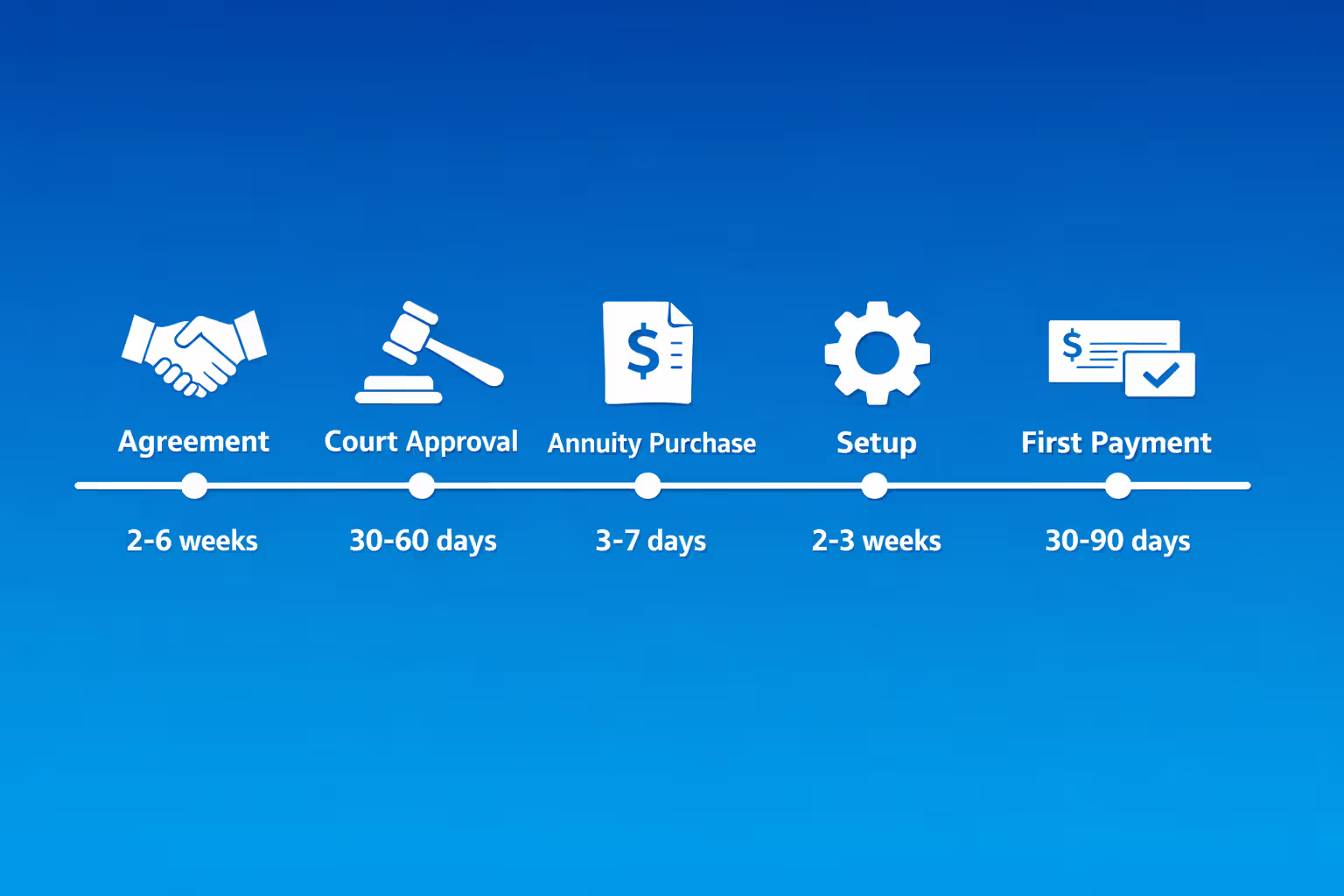

Agreement Signing: After negotiating terms, you sign a settlement agreement and release. This document specifies the payment schedule, identifies the assignment company and annuity issuer, and releases the defendant from further liability. Your attorney reviews every term because changes afterward are nearly impossible. Minors' settlements require guardian approval at this stage.

Court Approval Process: Most jurisdictions require court approval for structured settlements, particularly for minors or incapacitated persons. Your attorney files a petition with the settlement agreement attached. A judge reviews whether the structure serves your best interests, considering factors like age, injury severity, and financial needs. Approval hearings typically occur 30-60 days after filing, though uncontested matters may be approved on documents alone.

Annuity Purchase: Within days of court approval, the defendant's insurer wires funds to the assignment company. The assignment company immediately purchases the annuity from the chosen life insurance carrier. Speed matters here because annuity pricing fluctuates with interest rates. A rate drop between settlement signing and annuity purchase could reduce your total payments, though most agreements lock in rates at signing.

Assignment Documentation: The assignment company executes a qualified assignment agreement under IRC Section 130, formally assuming the periodic payment obligation. This legal document transfers responsibility from the defendant's insurer to the assignment company, which then looks to the annuity for funding.

Payment Schedule Setup: The life insurance company establishes your payment record in their annuity administration system. They verify your Social Security number, mailing address, and bank information if you elect direct deposit. Initial setup takes 2-3 weeks.

First Payment Delivery: Most structures specify first payment dates 30-90 days after settlement to allow time for all documentation and setup. Some claimants negotiate immediate first payments within 10-15 days if they have urgent needs. The life insurer mails checks or initiates ACH transfers according to your chosen delivery method.

| Phase | Key Activities | Typical Duration | Responsible Party |

| Settlement Agreement | Negotiate terms, sign release, finalize payment schedule | 2-6 weeks | Attorneys, parties |

| Court Approval | File petition, judicial review, approval order | 30-60 days | Court, your attorney |

| Annuity Purchase | Transfer funds, purchase annuity contract | 3-7 days | Assignment company, life insurer |

| Payment Setup | Establish payee record, verify information | 2-3 weeks | Life insurance company |

| First Payment | Initial payment delivery | Per agreement (often 30-90 days post-settlement) | Life insurance company |

The entire process from signed settlement to first payment typically spans 60-120 days. Expedited cases with immediate needs can compress this to 30-45 days, though court schedules often dictate timing.

Author: Andrew Halvorsen;

Source: avayabcm.com

How Payment Schedules Are Customized and Delivered

Payment structures range from simple to highly customized. The settlement payment operation guide offers flexibility to match your specific circumstances.

Monthly payments provide steady income replacement, mimicking a salary. A worker disabled at age 40 might receive $3,500 monthly for life, replacing lost wages. Monthly structures work well when you have ongoing living expenses and limited other income.

Annual payments suit those with other income sources who want yearly supplements. A $25,000 annual payment might cover property taxes, insurance premiums, and vacation costs. Annual payments also reduce administrative touches and potential for lost checks.

Lump sum intervals combine periodic income with occasional larger payments. You might receive $2,000 monthly plus $50,000 every five years for major expenses like vehicle replacement or home repairs. This hybrid approach provides both security and flexibility.

Increasing payments adjust for inflation or changing needs. Payments might start at $2,000 monthly and increase 3% annually, or jump to higher amounts at specific ages. A structure for a child might pay $1,000 monthly until age 18, then $3,000 monthly for college years, then $2,000 monthly for life thereafter.

Deferred structures delay all payments for years, allowing the settlement to grow. A 40-year-old might defer payments until age 65, receiving substantially more total dollars. The life insurer invests the premium for 25 years before payments begin, creating larger future payments than an immediate structure.

Cost-of-living adjustments (COLAs) are less common in structured settlements than in pensions because they significantly reduce initial payment amounts. A 3% annual COLA might reduce your starting payment by 30-40%, which many claimants find unacceptable despite long-term inflation protection.

Delivery methods have modernized significantly. While paper checks remain available, most recipients choose direct deposit for security and convenience. The life insurance company initiates ACH transfers to your bank account on scheduled dates. Some carriers offer online portals where you verify upcoming payments, update contact information, and access tax documents.

| Payment Type | Frequency | Best For | Pros | Cons |

| Monthly Income | 12x per year | Income replacement, ongoing expenses | Steady cash flow, budgeting ease | Smaller individual amounts |

| Annual Payments | 1x per year | Those with other income | Larger amounts, less administration | Requires yearly budgeting discipline |

| Lump Sum Intervals | Every 3-10 years | Major expenses, vehicle replacement | Addresses big-ticket needs | Long gaps between payments |

| Increasing Payments | Varies | Inflation protection, changing needs | Keeps pace with rising costs | Lower starting payments |

| Deferred Structure | Delayed start | Younger claimants, retirement planning | Maximizes long-term value | No immediate income |

Tax Treatment and Reporting Requirements for Recipients

Structured settlement payments from physical injury or sickness claims are completely tax-free under IRC Section 104(a)(2). You pay no federal income tax, no state income tax, and receive no Form 1099 for the payments. This tax exemption applies regardless of payment size or duration.

The tax-free treatment extends to all payments from the annuity, including any growth. Unlike taxable annuities where earnings are taxed as ordinary income, structured settlement annuities grow tax-free and distribute tax-free. A structure paying $500,000 over 20 years funded by a $300,000 premium generates $200,000 in tax-free growth.

Several conditions must be met to preserve tax-free status. The underlying claim must involve physical injury or physical sickness. Emotional distress claims without physical injury don't qualify. Employment discrimination, breach of contract, and other non-physical injury claims produce taxable settlements that cannot use tax-free structures.

The settlement agreement must specifically provide for periodic payments. Lump sum settlements, even from physical injury cases, can't be structured tax-free after settlement. The structure must be established as part of the original settlement, not created later by purchasing an annuity with settlement proceeds.

Punitive damages are taxable even in physical injury cases. If your settlement includes $400,000 for injuries and $100,000 in punitive damages, only the $400,000 can be structured tax-free. The punitive portion is taxable income whether received as lump sum or periodic payments.

You don't report structured settlement payments on your tax return. They don't appear on Form 1040, don't count as income for IRA contribution eligibility, and don't affect Social Security benefit taxation. The life insurance company doesn't issue Form 1099-MISC or any other tax form because the payments aren't taxable income.

One exception involves selling future payments. If you sell payment rights to a factoring company, the transaction may trigger tax consequences. The IRS could treat the lump sum you receive as taxable income, and you'll owe penalties for violating IRC Section 5891 if the sale wasn't court-approved. This creates a strong incentive to avoid selling payment rights.

Interest earned on payments after you receive them is taxable. If your $3,000 monthly payment sits in a savings account earning interest, that interest is taxable income. But the $3,000 payment itself remains tax-free.

Common Mistakes That Disrupt Structured Settlement Operations

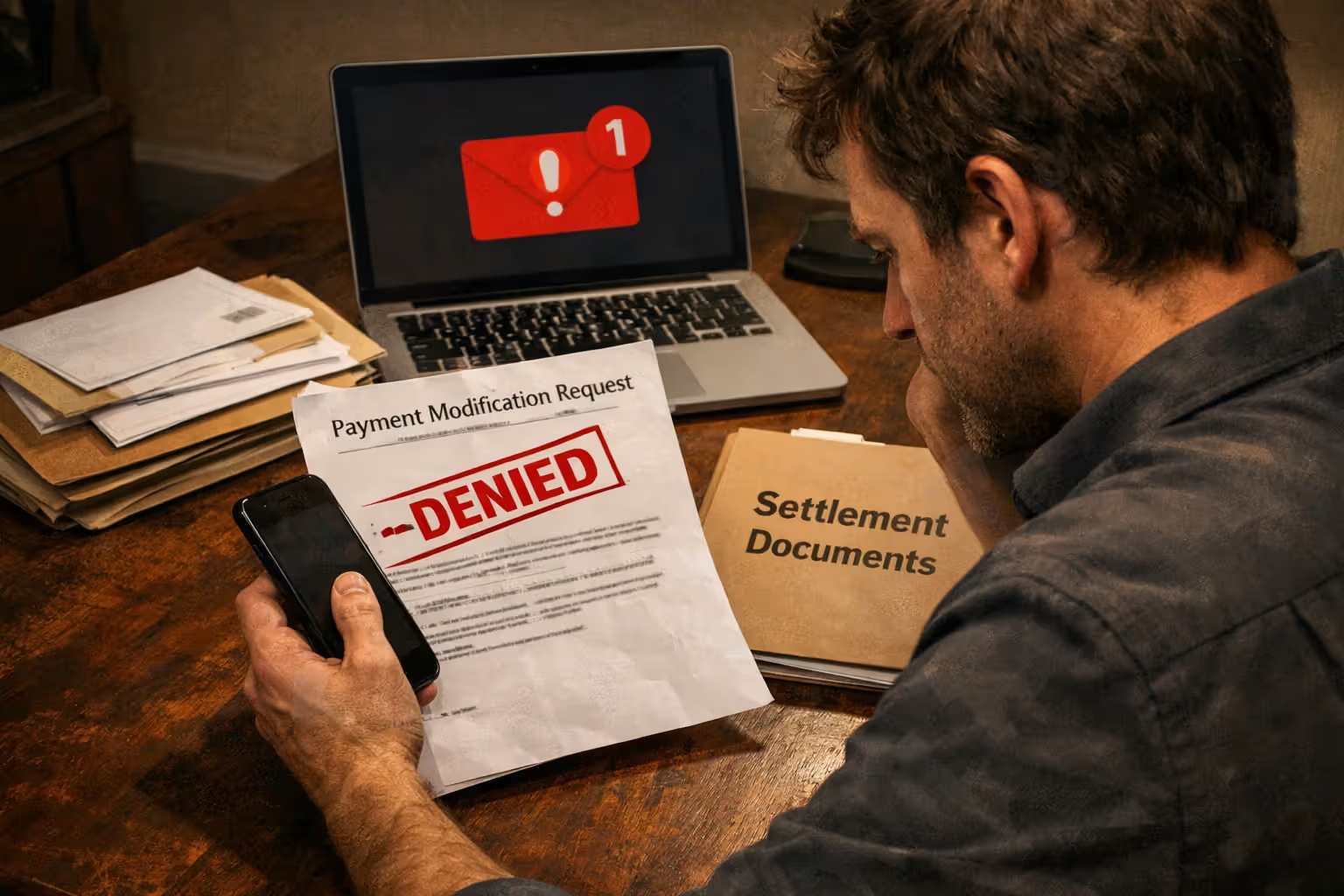

Attempting to modify payment terms after court approval ranks among the most frequent mistakes. Recipients experiencing financial hardship often contact the life insurance company requesting payment acceleration or schedule changes. These requests are always denied because the annuity contract is irrevocable. The structured settlement workflow guide established at settlement cannot be altered, even with compelling reasons.

Some recipients try to borrow against future payments or use them as loan collateral. Traditional lenders can't accept structured settlement payments as collateral because you don't own the annuity. Only factoring companies purchase payment rights, and their transactions require court approval under state structured settlement protection acts. Attempting to pledge payments to regular lenders wastes time and may expose you to predatory lending.

Author: Andrew Halvorsen;

Source: avayabcm.com

Misunderstanding payment terms causes unnecessary anxiety. Recipients sometimes panic when a monthly payment arrives on the 15th instead of the 1st, not realizing the settlement agreement specified mid-month payments. Others expect cost-of-living increases that were never included in their structure. Carefully reviewing your settlement agreement and annuity contract prevents these misunderstandings.

Tax mistakes occur when recipients confuse structured settlements with other financial products. Some incorrectly report payments as income, reducing tax refunds or triggering audits. Others assume they can deduct phantom "investment expenses" related to the annuity. The IRS doesn't recognize any deductions because the payments aren't income in the first place.

Beneficiary designation errors create probate complications. While structured settlement annuities typically include guaranteed payment periods (e.g., 20 years certain), recipients must designate beneficiaries to receive remaining payments if they die early. Failing to name beneficiaries or update them after marriage, divorce, or births forces payments through probate, delaying distribution and increasing costs.

Contact information lapses cause payment disruptions. Recipients who move without notifying the life insurance company may miss payments when checks go to old addresses. While companies attempt to locate payees, the process takes time. Maintaining current mailing addresses, phone numbers, and email addresses ensures uninterrupted payments.

Some recipients fall for scams promising to "unlock" structured settlement value without selling payments. These schemes claim special strategies to access principal while keeping payments, often involving life insurance policies or trusts. They're fraudulent. The only way to access future payment value is selling payment rights through court-approved factoring transactions.

Failing to understand state protection laws leads to problematic factoring deals. Most states require court approval before selling payment rights, but some recipients sign contracts with factoring companies without realizing court rejection will void the deal. These recipients waste months in legal proceedings, pay attorney fees, and end up with nothing.

FAQ: How Structured Settlements Work

Understanding how structured settlements work—from initial negotiations through decades of tax-free payments—helps you make informed decisions about injury compensation. The process involves multiple parties working together: attorneys negotiate terms, courts approve agreements, assignment companies assume obligations, and life insurers fund payments through annuities. While the structure becomes irrevocable after setup, careful planning during negotiations creates payment schedules matching your specific needs. The tax advantages, creditor protections, and guaranteed payments provide financial security that lump sums cannot match, particularly for those facing lifelong injury-related expenses.